Global| Nov 11 2015

Global| Nov 11 2015Japan's Money Growth Steadies

Summary

Money supply growth in Japan steadied in October as M2 was up 0.2% after being flat in September and up by 0.5% in August. M3 growth was up by 0.1% and M1 growth gained 0.4% in October, but both series slowed compared to August only [...]

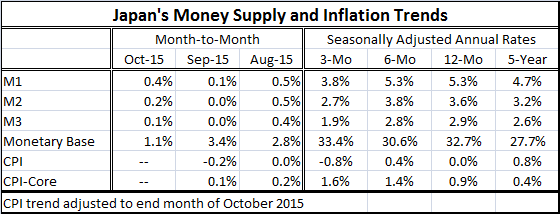

Money supply growth in Japan steadied in October as M2 was up 0.2% after being flat in September and up by 0.5% in August. M3 growth was up by 0.1% and M1 growth gained 0.4% in October, but both series slowed compared to August only gaining back some of weakness from September. All three monetary aggregates have slowed from 12-months to three-months and the slowdown has been gradual. Only M2 showed a slight pickup in growth over six-months compared to 12-months before heading lower over three-months.

Money supply growth in Japan steadied in October as M2 was up 0.2% after being flat in September and up by 0.5% in August. M3 growth was up by 0.1% and M1 growth gained 0.4% in October, but both series slowed compared to August only gaining back some of weakness from September. All three monetary aggregates have slowed from 12-months to three-months and the slowdown has been gradual. Only M2 showed a slight pickup in growth over six-months compared to 12-months before heading lower over three-months.

Japan continues to have its massive QE program in place but does not have much to show for it. Headline inflation has dropped from being flat over 12-months to dropping at a 0.8% pace over three-months. The core inflation rate is showing some signs of behaving as its growth rate has edged up from an annualized 0.9% pace over 12-months to 1.4% over six-months to 1.6% over three-months. These rates are all higher than its 5-year average gain of only 0.4%.

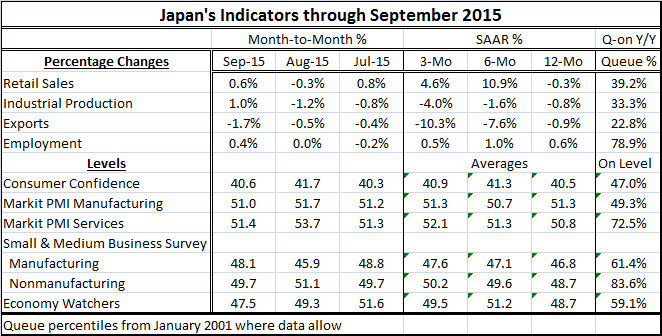

The table below presents some activity indicators and places them in their respective queues of values since 2001. These rankings show the relative strongest indicator is only in its 83rd percentile on this horizon. It is Japan's nonmanufacturing sector as assessed by small and medium sized businesses. This improvement is affirmed by the overall Markit services reading that has a lower standing in its 72nd percentile but still is showing some firmness. Employment sits in its 78th percentile, well above the median value which occurs at the 50th percentile for all rankings. Small businesses rate manufacturing better, in its 61st percentile, than does the overall Markit gauge that has the overall sector in its 49th percentile. However, consumer confidence ranks only in its 47th percentile with retail sales growth in its 39th percentile. Industrial production stands in its 33rd percentile with exports even weaker in their 22nd percentile.

The data scan of Japan's activity shows a great deal of weakness remains. The very low standing for exports shows that the international sector is still a drag on growth for an economy that is in some desperate need of stimulus. Despite a continued low standing of the yen exchange rate, Japan's exports are not advancing partly because they are hooked into slowing markets.

Money growth is struggling and not winning its battle for growth as we saw above. But the Bank of Japan is committed to at least holding the line on its QE policy and at least the core (excluding food and energy) CPI is showing some firmness. Japan is struggling to get growth in line. Its huge ratio of debt-to-GDP shadows the economy. The last policy effort to hike the sales tax to address the debt problem, caused the economic pickup that had been started by the QE program (Abenomics) to sputter. Japan's debt strategy continues to overhang and cloud economic performance. But the economic indicators show that growth is in gear just that there is not much of it and not any real sense of acceleration. To improve its economy Japan needs a viable debt strategy more than it need more QE.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief