Global| Apr 26 2017

Global| Apr 26 2017Japan's METI Indexes Show Ongoing Gains

Summary

Different strokes for different folks There are various Japanese indicators and some are available up through March. But here we are going to look at the updates through March to compared METI (indexes from Ministry of Economy, Trade [...]

Different strokes for different folks

Different strokes for different folks

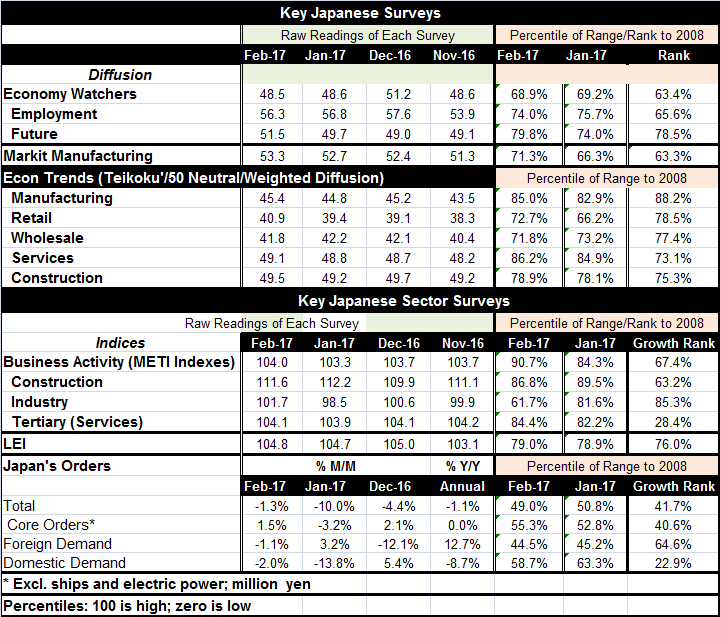

There are various Japanese indicators and some are available up through March. But here we are going to look at the updates through March to compared METI (indexes from Ministry of Economy, Trade and Industry) in tandem with other indicators also available through March.

Not surprisingly, different sorts of surveys produce different sorts of results and conclusions; yet, there are also a lot of consistencies.

Japan's services sector

The services sector is assessed by the METI indexes where it is named the 'tertiary sector.' That sector index rose to 104.1 in February from 103.9 in January, a small gain. Ranked by its 12-month growth rate, the tertiary index stands in its 28th percentile; that is quite weak. The tertiary index is up by a scant 0.2% over 12 months. The Economy Watchers index is also a service sector index. It has a diffusion format. The current reading at 48.5 shows a slight slip month-to-month. The level of the reading below 50 indicates that the services sector is not growing. This is not too different from the METI message where the tertiary index is up by just 0.2% over 12 months. The Economy Watchers index has a much higher 63rd percentile standing, compared with the tertiary index rank standing. And the Economy Watchers report also has an employment component and future index. Both of these are above 50, showing that employment gains continue and that the future index expects growth. The employment index has a 65th percentile standing while the future index - as low as it is - still has a 78th percentile standing. In other words, a future index at a weak diffusion reading of 51.5, barely signaling growth, has a top 22nd percentile standing. And it is at its strongest point since July 2015. Thus, the METI and Economy Watchers indexes seem to be more or less on the same page about the sector. They both embrace weak growth. But in ranking standing terms, METI is simply much weaker. We can add to all this to the message from the Teikoku indexes that have specific retailing and wholesaling as well as an overall services gauge. All the Teikoku diffusion indexes are below 50, showing sector shrinkage. The overall series gauge is the strongest at a reading of 49.1, close to the reading of the Economy Watchers current index. It also shows an improvement month-to-month. The Teikoku sector diffusion indexes at these generally lower diffusion readings show higher percentile rankings of the indexes, indicating a breadth of activity seen by Teikoku as weak even as the current readings are making a bigger step up relative to even weaker historic behavior. Thus, Teikoku shows a bit weaker momentum (lower sector diffusion readings) but a better improvement in momentum (higher ranked standings). In some ways, the weak Teikoku diffusion readings and their stronger rank standings bridge the gap between the economy index standing and the weak positioning of the METI index rank standing (since the METI sector diffusion indexes are weaker than the Economy Watchers current diffusion index, but their percentile rank standing is, nonetheless, stronger than either the Economy Watchers or METI).

Industry and manufacturing

The METI industry reading shows a gain in February to 101.7 from 98.5 in January. As we have seen in Europe and in the U.S., there is some sort of manufacturing revival that is being better signaled by indicators than by actual gauges of output. But that is not true of Japan where manufacturing IP itself rose by 3.1% in February and it is up by 6.6% over 12 months. Still, manufacturing IP in Japan is 20% short of its past cycle peak and yet evaluated since 2008 this growth rate is the seventh strongest giving it a 93rd percentile rank standing. The METI industry index is up by a 6.7% over 12 months and the 12-month growth rate has a strong 85th percentile standing. This is much stronger than the survey for overall or core orders (at the bottom of the table) where the order growth ranking is only in its 40th percentile or so, below its median. The Teikoku manufacturing sector diffusion index shows shrinkage with a diffusion reading of 45.4 in February although the level of index has a strong 88th percentile standing. By comparison, the Markit manufacturing gauge for Japan shows a diffusion index at 53.3, which does indicate that output is rising and it indicates a more moderate 63rd percentile standing (evaluated however only over the last five years).

Construction

There are construction sector readings for METI and Teikoku. The METI reading shows a construction sector step down in February to 111.6 from 112.2 in January. Construction activity is up by a modest 1.8% over 12 months. Teikoku is not much different with a diffusion reading of 49.5, showing shrinking sector activity on the month. Teikoku shows a 75th percentile ranking for construction compared to 63% in the METI framework.

Momentum overall

The overall METI index shows a gain in February to 104 from 103.3 in January. That marks a weak rise of 1.6% over 12 months. The LEI also notched a small gain in March, rising to 104.8 from 104.7 but gained a robust 5.8% over 12 months. The LEI envisions more growth ahead. The LEI has a 76th percentile standing, compared to a 67th percentile rank standing for the METI headline on current growth.

A final assessment

Of course, we always like to see a lot of gauges for an economy to help us place the economy in better perspective. But no two surveys are done the same and some simply use different methodologies. The rank standing calculations are meant to mitigate some of that because they place each indicator regardless of its absolute reading in an historic queue pitted against fellow readings complied under the same rules. Still, there are some differences. But what consistencies emerge here are that (1) the manufacturing sector is generally stronger than other sectors and not exaggerated by survey data, (2) the Teikoku survey shows more weakness yet a larger change in momentum than do other surveys, (3) the services sector is lethargic and near a stall speed although, (4) it is still better at creating jobs, (5) its future index suggests that somewhat better times lie ahead, (6) the overall METI index confirms that the overall Japanese economy does have growth in tow, and (7) the LEI suggests that the growth is set to improve, somewhat like what the economy watchers future gauge indicates.

The policy framework is still consistent with these facts

On balance, we find more consistency in these surveys than differences. But that sort of determination will always be somewhat subjective. Still, there is nothing in the speed of activity here to make us think that any price pressures are set to build up. The degree of economic slack and tightness is difficult to judge in an economy like Japan's with a shrinking population. In such a place, flat GDP will create rising per capital incomes. Japan is different and it will have to think different and operate differently. On balance, the stimulative BOJ policies still seem to be in order for this economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief