Global| May 19 2014

Global| May 19 2014Japan's Machinery Orders Hit Slow Patch Despite Appearances

Summary

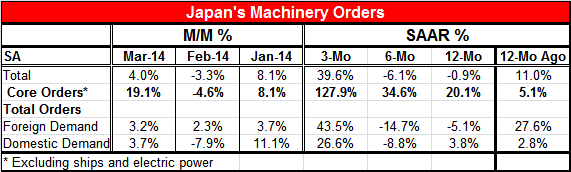

Overall Japanese machinery orders recovered in March, rising 4% from February's 3.3% drop after an 8.1% gain in January. Core orders (which exclude categories like ships and electric power) made a better recovery, rising 19.1% [...]

Overall Japanese machinery orders recovered in March, rising 4% from February's 3.3% drop after an 8.1% gain in January. Core orders (which exclude categories like ships and electric power) made a better recovery, rising 19.1% following a 4.6% decline in February and an 8.1% rise in January. Overall orders are strong over three months, rising by nearly 40% at an annual rate after posting declines over six months and 12 months. Core orders are showing a steady acceleration from 12 months to six months to three months on a three-month growth rate that's nearly 130% at an annual rate. These trends look eye-popping. But are they authentic?

Overall Japanese machinery orders recovered in March, rising 4% from February's 3.3% drop after an 8.1% gain in January. Core orders (which exclude categories like ships and electric power) made a better recovery, rising 19.1% following a 4.6% decline in February and an 8.1% rise in January. Overall orders are strong over three months, rising by nearly 40% at an annual rate after posting declines over six months and 12 months. Core orders are showing a steady acceleration from 12 months to six months to three months on a three-month growth rate that's nearly 130% at an annual rate. These trends look eye-popping. But are they authentic?

Machinery orders are a bright spot in an economy where other economic measures are losing momentum. However, we have to remember that this report is not completely topical as it only gives us orders through March, the period before Japan's sales tax kicked into gear after which a number of Japan's economic series began going into a tailspin.

However, as of March, both total foreign orders and total domestic demand are showing strength. Both rose in March; for foreign demand that came after increases in the previous two months whereas for domestic orders there was a decline in February but after a larger increase in January. As a result, both foreign and domestic demands are growing very strongly over three months. Foreign demand has moved into strong positive territory with a 43% annualized growth rate over three months following declines over 12 months and six months. Domestic demand is growing at a 26% annual rate following a decline of nearly 9% over six months and a 3.8% increase over 12 months.

The short-term growth rates tell a story of improving Japanese orders. However, because of the pending and widely anticipated sales tax increase, there has been a great deal of activity crammed into the first quarter, ahead of the second quarter when the tax was set to be imposed. When we step back from the shorter-term growth rates to look at trends in the year-over-year growth, we see a different, less ebullient, picture for Japan.

The growth rate for domestic orders over 12 months is the slowest since June 2013. June was preceded by a sharp year-over-year increase and that was preceded by declines in nine of the previous 11 months. Japan is showing domestic demand having ticked back up after its triple disasters but after flirting with growth rates of around 20% in five of the last eight months domestic growth in machinery orders already is wilting. It's down to 3.8% over 12 months. Foreign demand exhibited almost exactly the same profile in March. However, year-over-year foreign demand for machinery turned negative already in March, a sharper slowdown than for domestic orders. That's the first negative observation since February 2013. The decline in March represents a sharp reversal from February's strong gain of over 32%. Because of the abruptness of the March decline, it's too soon to get too pessimistic on foreign orders. However, if we look at the pattern of the time series for foreign demand (year-over-year trends), it seems clear that the bloom is off that rose, too.

The revival of orders in March, therefore, looks like it is part of the period of volatility and not a statement about the revival of long-term trends. Core orders seem to be holding up somewhat better and that is reassuring. However, looking at total orders for both foreign demand and domestic demand separately, we see very similar patterns of orders decaying as of March and with previous trends largely pointing to that is the authentic trend.

Machinery orders, despite their life in March and some strong three-month growth rates, do not seem to be suggesting that the Japan's industrial sector is going to sustain growth in the months ahead. We are certainly going to want to see what happens to these orders in the beginning of the second quarter, a period where we can already see that domestic demand is going to be at risk. Global demand (GDP) reports have also come in with disappointing results in recent weeks. Japan's prospects once again seem to be challenged. Has the imposition of the sales tax killed Abe's goose that laid the golden egg?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief