Global| Nov 10 2016

Global| Nov 10 2016Japan's Machinery Orders Falter As a New World Paradigm Emerges; The End of 'Business As Usual'

Summary

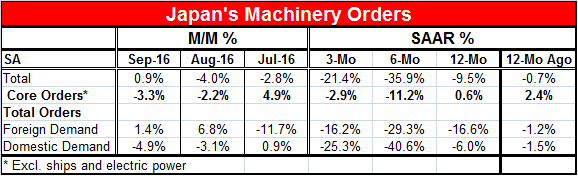

Japanese machinery orders rose in September after falling for two months in a row. Core orders excluding large projects, like ships and electric power projects, showed a drop of 3.3% month-to-month, their second straight monthly drop. [...]

Japanese machinery orders rose in September after falling for two months in a row. Core orders excluding large projects, like ships and electric power projects, showed a drop of 3.3% month-to-month, their second straight monthly drop.

Japanese machinery orders rose in September after falling for two months in a row. Core orders excluding large projects, like ships and electric power projects, showed a drop of 3.3% month-to-month, their second straight monthly drop.

All demand is weak

Despite an overall order bounce back in September, foreign demand, judging from overall orders, has been shrinking on any of the timelines in the table from three-month to six-month to 12-month. Domestic demand on that same metric has been worse. It is shrinking on all those same timelines and the shrinkage has become quite large, but at least it falls short of getting progressively worse.

No sign of progress for Japan

Still, there is nothing in these patterns that looks like a turnaround or stabilization in Japan's orders or growth (see chart).

Markets lead the way and ponder the new paradigm

The best news of the day is that financial markets are on the rebound. After selling off sharply particularly in Asia in the wake of the unexpected Trump victory in the U.S., markets in Asia are today following the lead of U.S. markets which did swoon in the early going yesterday but posted unexpected gains on the day of the Trump presidential election victory. While we can talk about economic data until we are blue in the face, there is right now far more interest in what this new U.S. leader will mean for geopolitical relations, U.S. economic relations, and the thrust of U.S. policy in general.

The end of wimp-o-nomics

If you have been longing for more normal interest rates, here they come. The belief that Trump will explode the fiscal deficits as he spends and cuts taxes at the same time has the U.S. yield curve steepening at a rapid pace. Rather than stopping the Fed from going ahead with its planned rate hike, the Trump effect seems to be providing a tailwind for those on the FOMC that want to hike rates and have been looking for a good reason to do it. The days of fiscal austerity and monetary excess are coming to a rapid close, at least in the U.S. And that is an interesting tale in and of itself.

The economic chasm will deepen and widen

This raises deeper questions about how economic forces will play out between Europe and the U.S. as well as between Asia and the U.S. In Japan, monetary policy is still fully accommodative as it is in Europe. Stronger U.S. growth- if Trump is successful- and less monetary accommodation will impact exchange rates and should act to raise the value of the dollar and intensify downward pressures on U.S. prices as well as on U.S. exports at a time when the President-elect is focused on repairing U.S. competiveness and on recasting what he views as trade deals gone wrong. These effects will move the U.S. trade accounts in the 'wrong' direction from his perspective.

The coming of cognitive dissonance

There is likely to be a lot of cognitive dissonance in the months ahead, so prepare yourself. I don't think the U.S. economy can repair the state of global demand by itself and certainly that is not an objective of Donald Trump - far from it. But the U.S. could provide an example of what a different fiscal tact can accomplish and that could bring more tension to bear in Europe where the Germans are unbelievers in fiscal policy the way most people are unbelievers in the tooth fairy.

Maybe only Japan is on auto-pilot

In Japan, fiscal policy is constrained by different forces since Japanese debt levels are so high. In Europe, the constraints are self-imposed and German-enforced.

Change!

We have to see how U.S.-China relations will play out, but China is already back on its heels admonishing Trump to preserve the status quo. Don't the Chinese know that Trump was running against the status quo? Something is going to give and it just may be China's sense of privilege that it should always get its way (on trade, on admission to the WTO, on getting the yuan in the SDR basket, on 'claiming' the South China Sea, etc.). And since China is such an important market for Japan, that will matter to Japan too.

Trump and Brexit define a new reality

The election of Donald Trump is the U.S. comes on the heels of the British Brexit vote and at a time when Europe is having its own identity crisis since the great EMU experiment is not working out the way many saw it or hoped. Germany has managed to capture, tame and turn the EMU into a device of its own prosperity while the rest of Europe is suffering and still being forced to pay the game by German rules which allow for little or no flexibility. Interestingly, this game was launched as Barack Obama took over as president in the U.S. nearly eight years ago. And while Europe and the world lauded his election, they put him and his Treasury secretary in the back row, stifled their voice and Germany stepped up as the architect of recession/post-recession and post-financial crisis growth. How is that working out? Can you hear me now?

Business as usual: no more

Now with the Obama Administration in its final days, there is a new U.S. leader with a new plan and his plan is not to sit in the back row and keep his mouth shut. No one will be giving him a Nobel Prize for his work in his first 30-days on the job, but arguably there will be few U.S. presidents whose impact on markets and on expectations will prove to have been more profound in the run up to taking office than what we will experience (and are experiencing) as Donald Trump prepares to succeed Barack Obama. One key question is whether Brexit and Trump give Europe an altered sense of the economic and political risks afoot and lead it to adopt more flexibility or whether these political changes in the U.S. and the U.K. will embolden dissent in the community and help the internal pressures there to escalate. To be sure, there are many unanswered questions that hang in the balance. One thing is clear, however. The days of 'business as usual' are over.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief