Global| May 09 2014

Global| May 09 2014Japan's LEI Shows Sharp Drop

Summary

Japan's leading economic indicator fell to 106.5 in March from 108.7 in February. The indicator is now declining at a 19.1% annual rate over three months and a 6.8% annual rate over six months. Over 12 months the index is crawling [...]

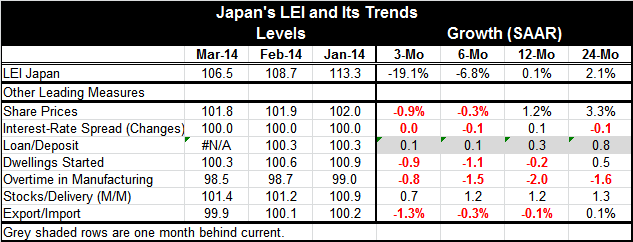

Japan's leading economic indicator fell to 106.5 in March from 108.7 in February. The indicator is now declining at a 19.1% annual rate over three months and a 6.8% annual rate over six months. Over 12 months the index is crawling ahead at an annual rate of 0.1%. Japan's LEI fell in March by 2% and it has fallen by more than that in one month less than 5% of the time back to 1994. The February drop was of more than 4%, the fourth largest drop in the LEI since January 1994. The LEI is sending a signal.

Japan's leading economic indicator fell to 106.5 in March from 108.7 in February. The indicator is now declining at a 19.1% annual rate over three months and a 6.8% annual rate over six months. Over 12 months the index is crawling ahead at an annual rate of 0.1%. Japan's LEI fell in March by 2% and it has fallen by more than that in one month less than 5% of the time back to 1994. The February drop was of more than 4%, the fourth largest drop in the LEI since January 1994. The LEI is sending a signal.

Contributing to the drop over three months are share prices which are falling at a 0.9% annual rate, dwellings-started which also is falling at a 0.9% annual rate, and overtime in manufacturing which is falling at a 0.8% annual rate. In addition, exports are growing faster than imports; the export/import metric is falling at a 1.3% annual rate.

Interest-rate spreads are stable over three months while the stock-to-delivery ratio is up by 0.7%. The lagging loan-to-deposit spread has been rising very modestly.

Abenomics is hoping to push the economy around the corner to sustainable stronger growth. But right now the economy is also trying to fight the headwinds imposed a consumption tax designed to address Japan's long standing fiscal excess.

The initial rounds of Abenomics appeared have an impact; working through the exchange rate channel as the yen fell, it helped Japan's export competitiveness. We now find the consumption tax hike may be about to have the dominant impact. The Bank of Japan has said it would do more if the consumption tax adversely impacted the economy. And it may step up its activities but will that be enough?

Japan's cross currents are many. The weak global growth environment continues to hold back its exports. Its important linkage to China while China is struggling is another headwind of sorts. Fortunately the lull in global growth has not ramped up oil prices as Japan has shuttered its nuclear capacity, but the increased oil import bill is still a huge hurdle for exports to overcome. Japan's industrial output is still expanding at a strong pace; manufacturing output is up by 7% over 12 months. And consumption is up strongly, rising by 11% over 12 months. However, these are the illusions of growth and the result of having announced that the consumption tax is coming. Consumption spurted ahead as consumers tried to buy items ahead of the sales tax imposition. As a result, industrial output and consumption were artificially stimulated. Now as Japan gets into the post-tax hike period, things will start to look different. The artificial fluff will be gone and we will see the impact of consumption having been shifted ahead as growth was borrowed from the future. The LEI is the first real hint of this. Japan seems to be about to struggle.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief