Global| Apr 14 2017

Global| Apr 14 2017Japan's IP Shows Broad-Based Resurgence

Summary

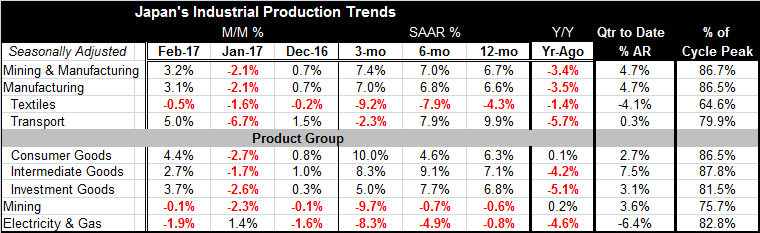

Japan's industrial output has bounced strongly in February, gaining 3.2% after a 2.1% January drop and making gains in two of the last three months. Combined mining and manufacturing output has growth rates skimming along at or above [...]

Japan's industrial output has bounced strongly in February, gaining 3.2% after a 2.1% January drop and making gains in two of the last three months. Combined mining and manufacturing output has growth rates skimming along at or above the 7% mark. Manufacturing alone sees growth up from about 6.6% to 7% from 12-month to three-month.

Japan's industrial output has bounced strongly in February, gaining 3.2% after a 2.1% January drop and making gains in two of the last three months. Combined mining and manufacturing output has growth rates skimming along at or above the 7% mark. Manufacturing alone sees growth up from about 6.6% to 7% from 12-month to three-month.

All three sectors consumer goods, intermediate goods and investment goods show solid-to-strong rates of growth over various spans of 12-month, six-month and three-month. There are no clear acceleration or deceleration trends in play. But sector output has growth at rates ranging from 5% to 10% annualized for the three sectors over these three time horizons. All of that is pretty solid stuff.

One place that improvement is very clear is in comparing Japan's current 12-month growth rates by sector to their corresponding 12-month rates of growth of one year ago. On that comparison, Japan seems to have a wholly new economy.

In the quarter-to-date, both manufacturing and the combined mining and manufacturing sectors show growth at a 4.7% annual rate. That is quite solid since these data already are adjusted for inflation. Growth in the 4.5% to 5% range is quite good. Japan is doing this with China, its major trading partner, still not firing on all cylinders

Viewed by sector, Japan's output is being led this quarter by intermediate goods with output up at a 7.5% pace in the current quarter followed by investment goods at a 3.1% pace and consumer goods output at a 2.7% pace.

Despite a grouping of very solid growth rates, Japan is still far from being in a position of generating any economic tightness. Manufacturing output is only at 86.5% of its past cycle peak. Intermediate goods have the highest sector ratio of current output to peak at 87.8% and investment goods have the lowest rate at 81.5%. Outside of manufacturing, mining has a ratio to peak output of 75.7%.

Japan is showing some solid-to-strong growth. It has no capacity issues. But it is still firmly fixed on its efforts to rid the economy of deflation. BOJ Governor Haruhiko Kuroda continues to endorse Japan's stimulus polices and there has been no hint of dismantling or unwinding any of them despite language or movement along those lines by the Federal Reserve in the U.S., by the ECB in Europe and at the Bank of England.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief