Global| Jul 31 2020

Global| Jul 31 2020Japan's IP Rebounds

Summary

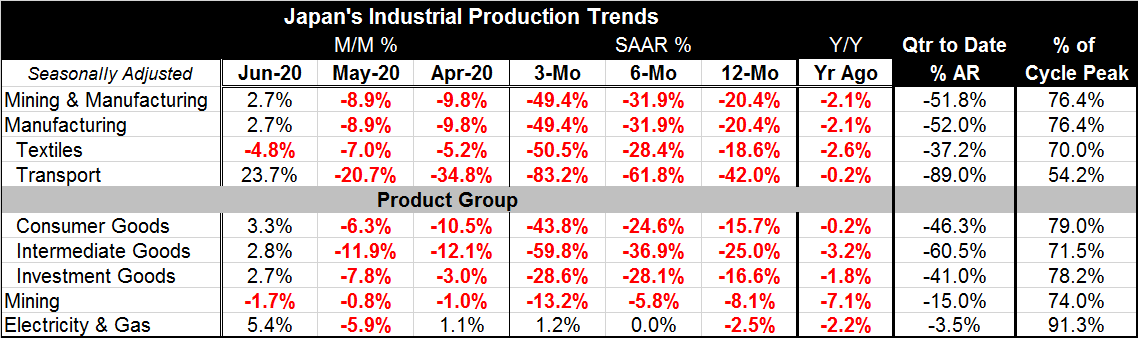

Japan's industrial production gained 2.7% in June after an 8.9% fall in May and a bigger drop in April. While the various growth rates over different tenors (see Chart) are slowing over more recent horizons, there is no reversal in [...]

Japan's industrial production gained 2.7% in June after an 8.9% fall in May and a bigger drop in April. While the various growth rates over different tenors (see Chart) are slowing over more recent horizons, there is no reversal in the sense that three-month growth rates are showing improved growth compared to six months. Sequential growth rates for Japan are still losing momentum despite this month's gain. The three-month IP growth rate is weaker than the six-month IP pace which is weaker than the 12-month pace. That is true for manufacturing, textiles, transportation goods, consumer goods, intermediate goods, and (barely) investment goods.

Japan's industrial production gained 2.7% in June after an 8.9% fall in May and a bigger drop in April. While the various growth rates over different tenors (see Chart) are slowing over more recent horizons, there is no reversal in the sense that three-month growth rates are showing improved growth compared to six months. Sequential growth rates for Japan are still losing momentum despite this month's gain. The three-month IP growth rate is weaker than the six-month IP pace which is weaker than the 12-month pace. That is true for manufacturing, textiles, transportation goods, consumer goods, intermediate goods, and (barely) investment goods.

In June, there are increases in all the sectors: consumer goods, intermediate goods, and investment goods. And while this is an increase across the board for the various manufacturing sectors, it is only a one-month gain. It may represent the toe-hold for sustained growth. But it is too soon to tell.

The industrial output story is told the same from the PMI data. Japan's manufacturing PMI has been stuck at the virtually the same diffusion value from April to May to June (41.9, 38.4 and 40.1, respectively). The diffusion data continue to see manufacturing output as very weak and contracting all through this period. The diffusion data do not flag an increase in output for June.

Japan continues to be an enigma with its major trade connections dug into China and the United States. China's early rebound is not helping Japan much and Japan so far is showing more industrial weakness than even the U.S. Japan is having some late issues with the virus after having run a low rate of infection overall. Japan's economy watchers index shows more of a profile like that of IP. It is very weak in April and May then recovers in June, but like the PMI report it also continues to point to ongoing declines in activity and no growth in June.

The virus continues to stalk the global economy. And there seems to be a lack of progress in understanding what the virus is and how it progresses. After all this time, there are no new approaches to it and for the most part only the most simple and old fashioned solutions are in vogue: wear a mask, wash your hands and social distance. In an age of technology after battling this virus globally for seven months, there is not much progress in understanding how to handle it. There is some progress in treatment. But the hope for a cure, for a vaccine, is still moving though it's inexorable timeline.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief