Global| Apr 17 2008

Global| Apr 17 2008Japan's IP is Revised Sharply Higher: Still Growth Trends are Mixed

Summary

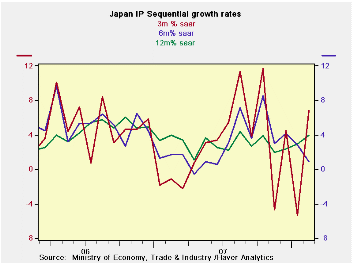

Japan's February industrial production was revised up sharply using a new data formula. Production is now in line with Japan’s strong exports, solving one of the puzzles about the economy for the Bank of Japan. Industrial production [...]

Japan's February industrial production was revised up sharply using a new data formula. Production is now in line with Japan’s strong exports, solving one of the puzzles about the economy for the Bank of Japan. Industrial production rose 1.6% in February from January, revised up significantly in a turnaround from the initial estimate of a 1.2% fall that was reported last month. The revision was due mainly to a change in data calculation methods rather than to revised data themselves. From a year earlier, February production rose 5.1% after gaining 2.2% in January. Still, for manufacturing sequential growth rates do not paint a clear picture. The revision has elevated the three-month growth rates to strong levels. But, even with the new readings, over six months there is a lull in growth compared to the 12-month pace. This finding is across the board in manufacturing; utilities output has a stronger more consistent trend. It is thus too soon to say that the revival discovered though data revision is what it seems. Several more months of data should help to clarify the nature of the trend.

| Japan Industrial Production Trends | |||||||

|---|---|---|---|---|---|---|---|

| m/m % | Saar % | Yr/Yr | |||||

| seasonally adjusted | Feb-08 | Jan-08 | Dec-07 | 3-mo | 6-mo | 12-mo | Yr-Ago |

| Mining & Manufacturing | 1.6% | -0.5% | 0.6% | 6.8% | 0.9% | 4.0% | 4.0% |

| Total Industry | 2.0% | -0.5% | 0.5% | 8.4% | 1.6% | 4.4% | 3.9% |

| Manufacturing | 1.6% | -0.6% | 0.7% | 6.8% | 0.9% | 4.0% | 4.0% |

| Textiles | -0.2% | -2.3% | 1.6% | -4.0% | -6.3% | -6.0% | -3.6% |

| Transport Eqpt | 1.3% | 1.8% | 1.3% | 18.9% | 5.4% | 11.4% | 6.7% |

| Product Group | |||||||

| Consumer Goods | 2.7% | 0.2% | 0.9% | 16.4% | 1.8% | 6.9% | 3.2% |

| Intermediate Goods | 1.0% | -1.9% | 1.1% | 0.7% | 2.0% | 4.0% | 4.6% |

| Investment Goods | 1.1% | 0.5% | 0.0% | 6.4% | -2.6% | -0.5% | 4.6% |

| Mining | 2.3% | -6.7% | -1.6% | -22.0% | -5.7% | -4.5% | 4.8% |

| Electricity & Gas | 9.7% | 0.1% | -1.2% | 38.7% | 17.4% | 17.5% | -1.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief