Global| Apr 17 2020

Global| Apr 17 2020Japan's IP Falls in February...It's Only the Beginning

Summary

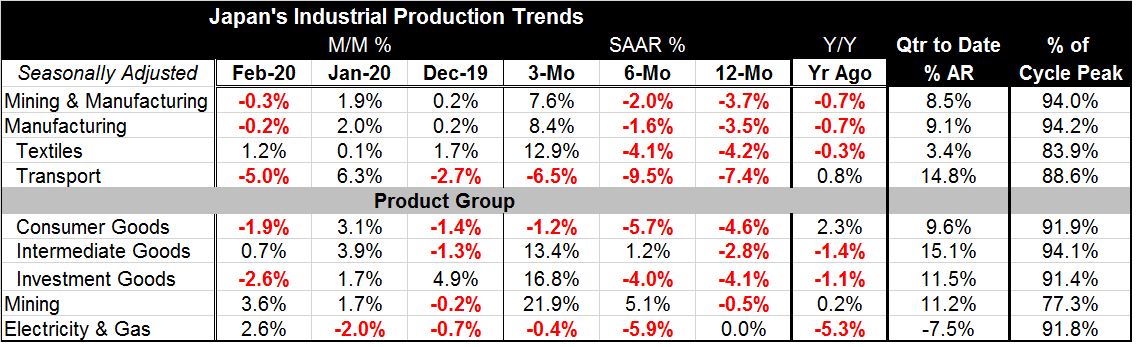

Japan's industrial production fell by 0.3% in February after two straight months of gains with January having been especially strong. Mixed trends Japan's industrial production trend has two distinct aspects. From 12-months to six- [...]

Japan's industrial production fell by 0.3% in February after two straight months of gains with January having been especially strong.

Japan's industrial production fell by 0.3% in February after two straight months of gains with January having been especially strong.

Mixed trends

Japan's industrial production trend has two distinct aspects. From 12-months to six-months to three-months, industrial production is generally accelerating. That is true for overall IP for manufacturing, for intermediate goods and for investment goods output. That same sequence of growth also holds for mining. However, the graph shows year-on-year trends and despite some trimming of losses in early-2020 all year-on-year sector trends continue to point lower. So Japan has this short-term-longer term trend divergence.

Surreal trends

Because January output was so strong, the quarter-to-date gains are positive and strong across all sectors with manufacturing up at a 9.1% annual rate two months into Q1. But these figures seem surreal compared to what is going on in the real world in real time.

Challenges

Japan is fighting off the coronavirus and undergoing some substantial stay-at-home edicts. Also just today, China, Japan's largest trading partner, reported a substantial decline in its GDP of -6.8%, the first it has ever reported (quarterly Chinese GDP data only date to 1992). And the U.S., Japan's second-largest trading partner, is currently in a coronavirus inspired 'economic-coma' as it tries to fend off spread of the virus and has accepted economic weakness as the cost. Of course, in such circumstances, it is hard to take the upbeat Japanese short-term trends seriously...or as sustainable.

Global and regional issues

The IMF is reporting a projection of a 3% decline in global growth for the year and the Asian Development Bank (ADB) has cut back its outlook for the region. The daily count of coronavirus infections and deaths continues to rise in Southeast Asia with Indonesia now leading the pack, having just surpassed the Philippines for the largest number of cases in the region. Clearly Japan is surrounded by weakness and other issues.

Domestic issues add to the woes

At home Japan's own tertiary index, an index of the services sector that is nearly a wholly domestic measure, fell by 0.5% in February. Between that sort of domestic weakness, newly implemented stay-at-home policies from Prime Minister Abe, and economic weakness all around the region and in the global economy, we can look for economic weakness in the coming month on the industrial front in Japan as well.

Assessment

What we do see is that Japan's economy had regained some footing before the tsunami of economic weakness hit it as it surely did in March. But with the U.S. economy just entering its down phase as suggested by the U.S. March index of leading indicators falling by 6.7%, Japan's fate to weakness is more or less sealed, regardless of what the trends show. U.S. weakness is oncoming and China's recovery will be slow acting. Japan will be caught in that very unpleasant environment. And it will have to deal with its own virus issues that are looking more serious.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief