Global| Feb 28 2020

Global| Feb 28 2020Japan's Indicators Show a Lethargic Economy

Summary

Japan's growth is fading New reports on retail sales, industrial production and housing starts do not change the sense of weakness in Japan's economy. In January, retail sales rebounded to gain 1.2% month-to-month. However, housing [...]

Japan's growth is fading

Japan's growth is fading

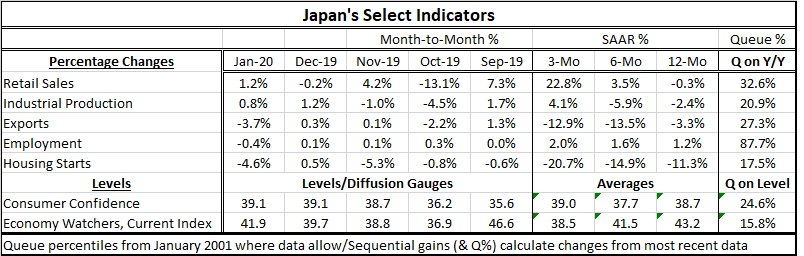

New reports on retail sales, industrial production and housing starts do not change the sense of weakness in Japan's economy. In January, retail sales rebounded to gain 1.2% month-to-month. However, housing starts fell by 4.6% as industrial production made its second straight monthly gain rising by 0.8%.

However, in January among the five indicators in the top panel of the table all indicators except employment show 12-month losses. The queue standings of the year-on-year percent changes are clustered in the lower 30th percentile or lower when ranked in their respective historic queues of data. Only employment is an exception with a strong 87.7 percentile standing.

Job growth keeps Japan's economy advancing. However, growth has been impacted by the late year hike in the sales tax which despite the government's best efforts still dealt the economy a body blow.

Retail sales and employment demonstrate gathering upside momentum as growth rates improve from 12-months to six-months to three-months. But on those same timelines, exports and housing show opposite, weakening trends.

The indicators we tend to assess more in level terms are in the bottom on the table. They include the manufacturing and service sector PMI data that are bounded by zero and 100 as well as the economy watchers index and consumer confidence. The levels data show some improvement in their monthly values. But this is a small-potatoes move as trends based on the 12-month to six-month to three-month averages show across the board index declines except for consumer confidence. The queue standings of the level data are generally slightly lower than for the percentage changes above.

Money growth and inflation

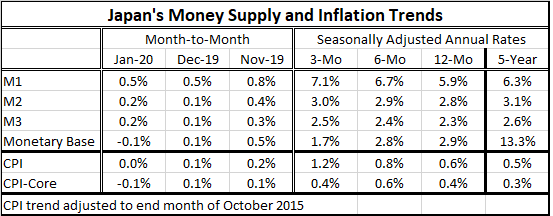

Money growth and inflation trends underline the hard time Japan has had in trying to boost inflation. While Japan barely shows the various money measures as accelerating from 12-months to six-months to three-months. The 12-month and even most of the three-month rates of growth are below the growth rates those variables have averaged over five years. The effort to stoke inflation using money growth has been fading.

As for inflation itself, the headline is slightly higher moving from 12-months to six-months to three-months, but the core seems to be stuck around the 0.4% to 0.5% mark. These trends put headline inflation which is volatile higher than its five-year average of 0.5%, but the core rate is only a tick higher than its five-year average of 0.3%. Japan has not been able to translate stronger money growth into more inflation.

2020 outlook

And the outlook for the year ahead is grim. The United States and China, Japan's two largest trading partners, settled 'Phase-One' of their trade war giving rise to some confidence in Japan that growth could move ahead again. But the U.S. still seeks further changes from China and despite that trade deal most U.S. tariffs on Chinese goods have been left in place. So Japan's optimism may have been misplaced to start. Then, to make matters worse, the coronavirus broke out. Japan already trades the most with China compared to any other country and Chinese tourists shop in Japan. Japan and China exchange a lot of goods in trade and swap a lot of tourist visits which is a bad thing if there is worry about spreading the coronavirus. Currently, Japan is taking steps to contain the virus. It has put school children on an extended holiday. While bottling up people on the cruise ship may not have been good for them, Japan has mostly controlled that contagion but there are other risks. And Tokyo has such a high population density and has mass transit that is extremely heavily utilized that the last thing Japan wants to have to deal with is an outbreak that reaches Tokyo.

WHO has warned that cases of infection outside China outnumber cases of infection in China and that the risk of the outbreak is growing. The coronavirus is the big risk of 2020 that no one saw coming. And it finds a heavily indebted global economy that is also beset with various geopolitical instabilities. The risks for 2020 are mounting and Japan already ended 2019 with a substantial decline in real GDP as a legacy effect of its consumption tax hike. It is impossible to handicap the risks, but a simple look at the reaction of financial markets lets you know in no uncertain terms that the situation is both serious and worrisome.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief