Global| Aug 17 2015

Global| Aug 17 2015Japan's GDP Sinks in Q2

Summary

Japan's GDP fell by 1.6% at an annual rate in Q2. The drop off, after sharply higher growth in Q1, comes despite a huge stimulus program that Japan has in place (Abenomics). Despite the setback to quarterly growth, year-over-year [...]

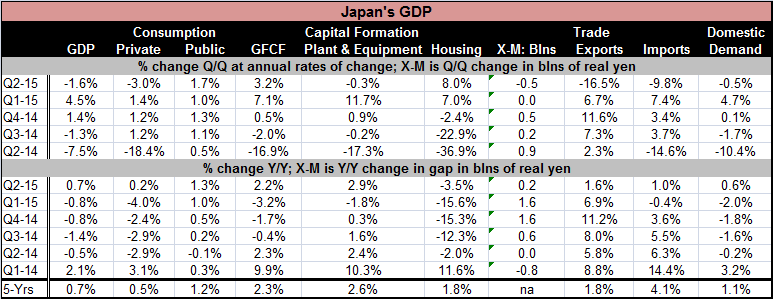

Japan's GDP fell by 1.6% at an annual rate in Q2. The drop off, after sharply higher growth in Q1, comes despite a huge stimulus program that Japan has in place (Abenomics). Despite the setback to quarterly growth, year-over-year growth in Japan's GDP is now at a positive 0.7%.

Japan's GDP fell by 1.6% at an annual rate in Q2. The drop off, after sharply higher growth in Q1, comes despite a huge stimulus program that Japan has in place (Abenomics). Despite the setback to quarterly growth, year-over-year growth in Japan's GDP is now at a positive 0.7%.

Private consumption collapsed in Q2, falling at a 3% annual rate. Public consumption rose by 1.7%, offsetting only part of that loss. Gross fixed capital spending rose at a 3.2% pace and housing investment advanced at a solid 8% pace. But spending on plant and equipment fell at a 0.3% rate and Japan's exports fell at a 16.5% annual rate, dealing the final blow to GDP. Imports fell in Q2, lessening the shock on GDP, but imports only fell at a 9.8% annual rate much less than the decline in exports. Overall, domestic demand shrank by 0.5% as exports imploded, dealing the economy a severe one-two punch.

However, in the wake of this devastating report, Japan's stock markets are higher. Investors are betting that Prime Minister Abe is willing to pony up even more stimulus. BoJ head Kuroda has been forced to set back the date when he expects Japan to attain its 2% inflation goal. Monetary stimulus could even increase.

Japan continues to struggle. And the recent devaluation by China is going to make Japan's task of achieving recovery even harder, as China's competitiveness has just stepped up a notch. The yen itself has deprecated to a significant extent after years -decades- of rising and may now back to a reasonable value on world markets. Of course, Japan, like most developed countries, will also benefit from the China devaluation because Japanese firms operate in China. But for the moment China's economy is very weak and its contribution has been to worsen the performance of companies operating there.

The world economy has become a complicated place. But it is clear that countries benefit most from the activities that go on within their borders, not from the activities of their corporation in markets abroad. One thing that remains dead simple is the weakness of global growth and the absence of inflation. Oil prices again are dropping on world markets accentuating this trend. China devaluation will reinforce that trend. Economists still think the Fed is headed for a September rate hike in this environment. It makes you scratch your head.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief