Global| Sep 08 2020

Global| Sep 08 2020Japan's Economy Watchers Index Ticks Higher

Summary

Setting aside the numbers that are so much more precise, a look at the graphics tells the clear story of the economy watchers index and its gauge of the future. Japan was hit hard by the virus; after a plunge the economy watchers [...]

Setting aside the numbers that are so much more precise, a look at the graphics tells the clear story of the economy watchers index and its gauge of the future. Japan was hit hard by the virus; after a plunge the economy watchers index made a nearly equally strong and rapid recovery. But the recovery is not a full recovery. Moreover, Japan's economy already had been experiencing fading action in the economy watchers' profile before the coronavirus hit. These two factors leave the economy watchers index in this bent and fading profile that from 2013 onward has seen bumps up and down but was generally forming lower and lower peak values and giving way to a steady erosion that set in after 2017.

Setting aside the numbers that are so much more precise, a look at the graphics tells the clear story of the economy watchers index and its gauge of the future. Japan was hit hard by the virus; after a plunge the economy watchers index made a nearly equally strong and rapid recovery. But the recovery is not a full recovery. Moreover, Japan's economy already had been experiencing fading action in the economy watchers' profile before the coronavirus hit. These two factors leave the economy watchers index in this bent and fading profile that from 2013 onward has seen bumps up and down but was generally forming lower and lower peak values and giving way to a steady erosion that set in after 2017.

The rebound in the current index is still part of the covid-19 recovery process, but it is not very robust. While numbers attach numerical values to the various concepts, they must be applied over specific periods and that specificity can be somewhat arbitrary. That is why I begin this analysis with reference to the graphic for Japan because the process of erosion is complex and essentially very long lived there but it is nonetheless clear.

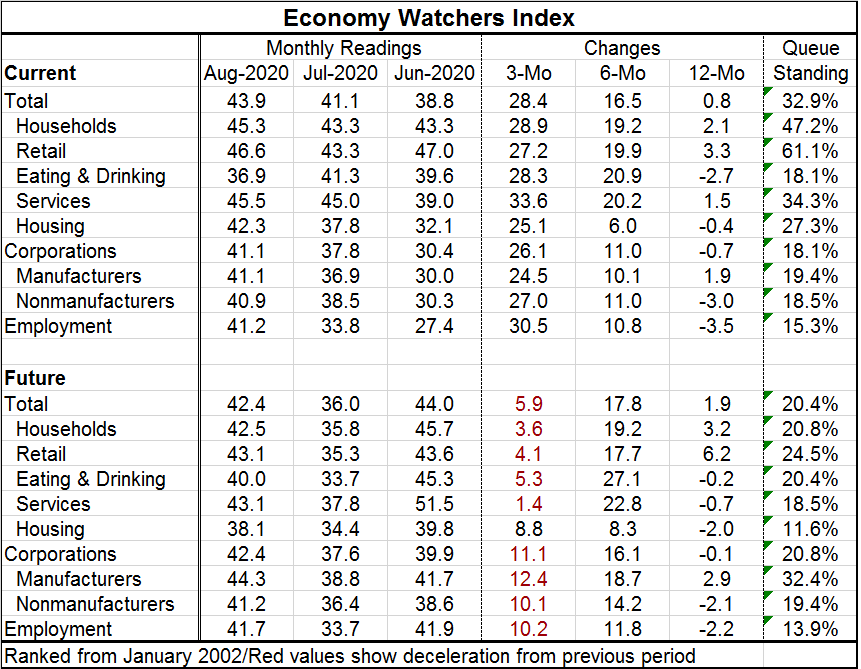

There is a marked difference between the various current readings and their future reading counterparts in this survey. The current overall economy watchers index shows a three-month value of 43.9 which compares ‘favorably' to the future outlook at 42.4. However, the ranking for those two values are very different as the current index ranks in its 32.9 percentile, well below its median value (which occurs at a rank of 50), while the future index is even weaker at its 20.4 percentile. The differences are more marked if we look at three-month changes; here the current index has risen by 28.4 points while the future index has improved by just 5.9 points. Both indexes show a more sizeable gain over six months and both show very small changes over 12 months. The six-month change gets back to data as of February when some of the early coronavirus impact was affecting the economy. The actual low came in April, but March, April and May are all severely affected months for the current index while February, March and April were the most affected months for the future index.

We are on a wild goose chase to look for good news in this survey. Some of the news is not as bad as other news; however, none of the news here is really good. In the current survey of the nine categories, all but eating and drinking places have readings with diffusion values in their 40-percentile range. For retailing though, that reading is enough to propel its queue standing above its median to a 61st percentile standing. Employment overall, nonmanufactures and eating & drinking places have the lowest queue standings.

For the future index no components have an above-median standing. Manufacturing has the strongest ranking with a 32.4 percentile standing. All the three-month changes in the future survey are very small; some barely get to double digits while five sectors fall short of that. Over 12 months, six components are still lower on balance and none among those with positive changes has advanced by very much.

On balance, the economy watchers survey is still a downbeat assessment on the economy. The last three months are showing improvement, but there is no great promise of the future and it is a series of diffusion readings all of which are below 50 and accompanied by weak queue standings for the current barometer, and weaker standing for the future components. Diffusion readings below 50 indicate ongoing contraction, but improving diffusion values suggest that the contraction is lessening in its intensity.

Japan's situation is further clouded by the decision of Prime Minister Abe to step down because of illness. It is unclear how policies will change in his absence and what path his successor will pursue. The coronavirus is still a factor in Japan. Global growth is still weak and Japan's long fight to restore growth and attain price stability is still in gear. At least Abe and the BOJ seem to have expunged deflation. But the path ahead remains challenging for Japan.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief