Global| May 13 2021

Global| May 13 2021Japan's Economy Watchers Index Goes Choppy

Summary

Last year in April the virus plunged Japan's current and future Economy Watchers Indexes to their lows. Both sprang back very strongly and by June they had attained levels that actually both are higher than the April 2021 readings [...]

Last year in April the virus plunged Japan's current and future Economy Watchers Indexes to their lows. Both sprang back very strongly and by June they had attained levels that actually both are higher than the April 2021 readings recorded today. From June forward, both the future and the current household indexes have seen higher readings, but then they have been lower too. After the initial recovery in June, the current index moved higher for four more months before seeing a set-back while the future index moved lower in July, then rose modestly for three months in a row before seeing a setback. Since Japan's recovery, in June 2020, the current and future indexes have undergone a good deal of volatility as Japan has struggled to contain the virus using a variety of restrictions in and around the Tokyo area in particular. Even now Japan is under restrictions as it tries to pave the way for hosting a safe Olympics at long last.

Last year in April the virus plunged Japan's current and future Economy Watchers Indexes to their lows. Both sprang back very strongly and by June they had attained levels that actually both are higher than the April 2021 readings recorded today. From June forward, both the future and the current household indexes have seen higher readings, but then they have been lower too. After the initial recovery in June, the current index moved higher for four more months before seeing a set-back while the future index moved lower in July, then rose modestly for three months in a row before seeing a setback. Since Japan's recovery, in June 2020, the current and future indexes have undergone a good deal of volatility as Japan has struggled to contain the virus using a variety of restrictions in and around the Tokyo area in particular. Even now Japan is under restrictions as it tries to pave the way for hosting a safe Olympics at long last.

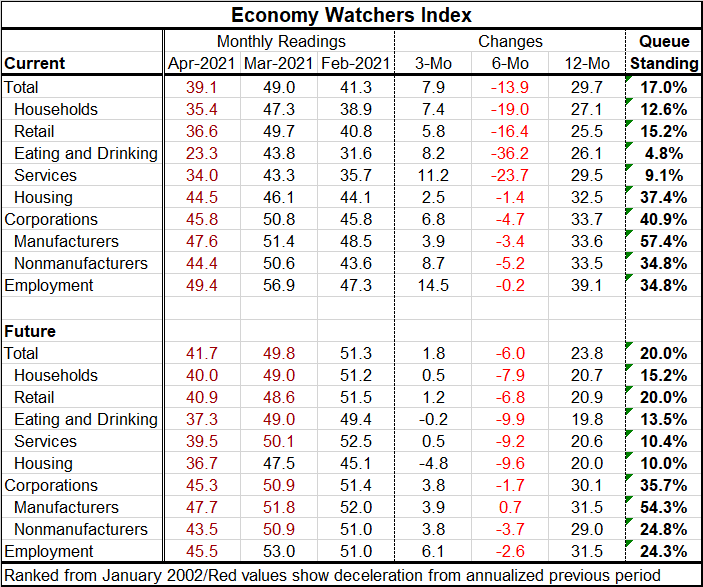

In table below, the color red highlights deceleration either month-to-month or from one period to the next (3-month vs. 6-month, 6-month vs. 12-month, 12-month vs. year ago, pro-rated of course). The current indicators' color coding shows a sort of loopy cycle that the current index has fluctuated widely. Its gain over 12-months is greater than the change it had between 12 months and 24 months ago. The gain over six months is weaker than prorated change over 12 months. And over three months changes are stronger than the pro-rated six-month change. Overall, there is a speed up over three months. That speed up is on the back of improvements across the board in February and March, but those are partly offset by deterioration in April.

The future index shows monthly deteriorations in expected conditions in both April and March on a widespread basis after widespread improvements in February. But on the strength of February, the three-month change in expectations is positive across the board. The six-month expectation falls more than the 12-month expectations when prorated. And the 12-month expectation rises across all industries compared to its change of 12 to 24 months ago. These changes signal a great deal of choppiness in Japan's indicators and their signals. That is most easily seen from the graphic at the top.

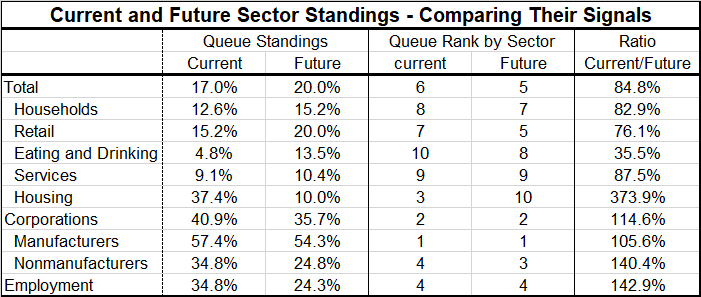

The table below focuses on the levels of the queue standings in the current and future readings instead of on index point changes. There is a strong correlation across the queue standings for the future and the current indexes. A correlation of about 0.79. If we pool the headline with all the components and look at the 10 table entries as ‘equals' there are five cases of the current readings being higher than the future readings and five cases of the future readings higher than the current readings using queue standings for the comparison. The top-ranking current queue standings and the top ranking future queue standings both rank manufacturing as number one, and corporations as number two both have high ranking for nonmanufacturer corporations and for employment. The current reading, however, also has a strong reading for housing whereas the future reading for housing is at the bottom on the heap in the future queue. Households retailing eating and drinking places and services generally rank low in both surveys based on their queue standings.

The virus imbroglio

Japan is still dealing with virus issues and planning to hold the one-year delayed Olympics. The very slow rate of vaccinations in Japan coupled with the government's devotion to holding the Olympic games has created a powerful pushback in Japan against the games. Japan's situation is unique because the government is holding back vaccinations it has. At the same time, Japan is not very different since we see that whatever a government chooses to do it can face a broad backlash from its citizens to whatever policy a government adopts. Virus policy is made worse because governments feel as though they must justify what they are doing as ‘science.' Yet, reasonable people can draw different conclusions from the data on covid-19 and yet each country adopts its own notion of how to fight the virus and wants all of its citizens on board for that action even if the action can't be fully supported by ‘science.' That explains why there is so much controversy about governments and their respective virus policies. Some people are protesting to get vaccinated; others assert their right to opt out of vaccination requirements. What a mess.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief