Global| Mar 09 2015

Global| Mar 09 2015Japan's Economy Watchers Index Fights Back

Summary

Economic growth in Japan was revised lower in Q4, unsettling markets. But the more topical economy watchers index rose in February, poking its head up above the 50 level to stand at 50.1, signaling expansion. The employment gauge [...]

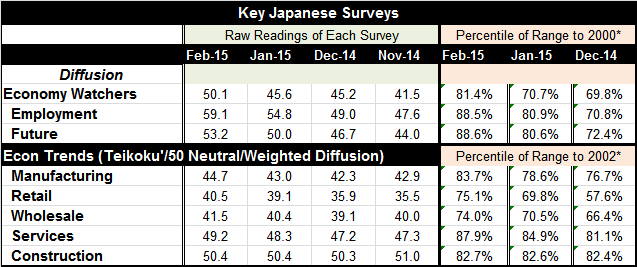

Economic growth in Japan was revised lower in Q4, unsettling markets. But the more topical economy watchers index rose in February, poking its head up above the 50 level to stand at 50.1, signaling expansion. The employment gauge moved sharply higher to 59.1 from 54.8 in January. The future index moved smartly higher to 53.2 in February from 50.0 in January. The future and current readings are telling a reinforcing pro-growth story.

Economic growth in Japan was revised lower in Q4, unsettling markets. But the more topical economy watchers index rose in February, poking its head up above the 50 level to stand at 50.1, signaling expansion. The employment gauge moved sharply higher to 59.1 from 54.8 in January. The future index moved smartly higher to 53.2 in February from 50.0 in January. The future and current readings are telling a reinforcing pro-growth story.

We juxtapose the economy watchers data with the Teikoku sector readings whose indexes show a widespread improvement across sectors of various types in February. Still, manufacturing, retailing, wholesaling and services all are struggling to show gains on that gauge (levels above 50). Only the construction sector that was unchanged in February shows a diffusion gauge above 50 and signals an outright rise in the sector.

Still, these various gauges from Teikoku and the economy watchers all show relatively high percentile standings of the surveyed gauges. All three economy watchers gauges are in their 80th percentile with employment and the future gauge each in the 88th percentile. For Teikoku, the rankings range from the 74th percentile (wholesaling) to the 87th percentile (services).

Japan continues to struggle concerning keeping inflation up to 2% as oil prices decline and it struggles to keep growth in gear. China, an important trade partner for Japan, is gearing down now preparing to meet only 7% growth as it has continued to pare its expectations and targets for growth.

Just today Germany, one of the most productive and efficient economies in the world with a huge current account surplus and cheap and falling currency, nonetheless, produced weak export growth as German dependence on the China market is starting to show some wear and tear from the special events washing over China's economy and slowing it down.

Asia is still an import locus of growth but attention has shifted to the U.S. as it has begun to grow better or at least to show improved job growth as we saw with last Friday's job report. Economies around the world are looking for ways to tap into the U.S. economy as they expect U.S. domestic demand to grow and want to go along for the ride. But the U.S. has been better at creating jobs than at creating GDP growth of late. The U.S. may not have quite the bright star to affix a wagon to. Many U.S. jobs are low end jobs and low skill jobs and therefore low productivity jobs. It explains why U.S. productivity growth has fallen off and why GDP growth is now lagging job growth in the U.S.

The world economy continues to look for some solution to its morass. Quantitative easing is now in force from the U.S. to the U.K. to EMU to Japan. And while it has been helpful, it has been no panacea. Japan and Europe's QE seem to work mostly through the exchange rate. But for that to be effective there will have to be enough global effective demand to be exploited. Since austerity is still the name of the game everywhere except maybe China, it's not clear how/where that `domestic' demand will develop. If the U.S. is not the solution, then what is? If the U.S. growth surge falls short, what will replace it?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief