Global| Aug 10 2016

Global| Aug 10 2016Japan's Data Are Mixed in June

Summary

Fresh observations (recently released data) on Japan's machinery orders and tertiary sector index (services) in June give off somewhat positive but still mixed signals, referring to an economy that is still under the pressure of the [...]

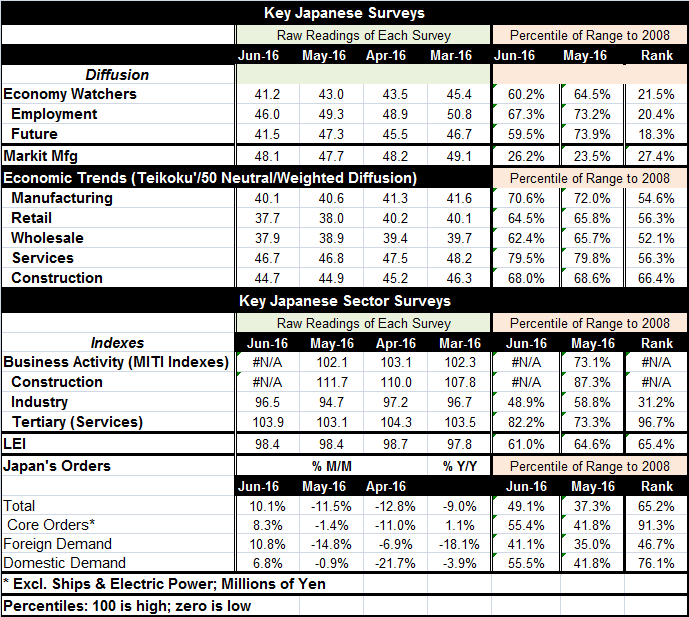

Fresh observations (recently released data) on Japan's machinery orders and tertiary sector index (services) in June give off somewhat positive but still mixed signals, referring to an economy that is still under the pressure of the broad forces of contraction. Japan's machinery orders rose by 10.1% in June as they fell by 9.0% year-on-year. Core orders rose by 8.3% in June as they advanced by 1.1% year-on-year. The tertiary index was up to 103.9 in June from 103.1 in May, still below April's 104.3.

Fresh observations (recently released data) on Japan's machinery orders and tertiary sector index (services) in June give off somewhat positive but still mixed signals, referring to an economy that is still under the pressure of the broad forces of contraction. Japan's machinery orders rose by 10.1% in June as they fell by 9.0% year-on-year. Core orders rose by 8.3% in June as they advanced by 1.1% year-on-year. The tertiary index was up to 103.9 in June from 103.1 in May, still below April's 104.3.

Divergent signals

The full set of business activity indexes is not yet ready for June but the industry and tertiary (services) indexes both are up in June. The industrial index standing is in the 31st percentile of its historic queue of data for the recession and post-recession period while the tertiary index stands at its 96.7 percentile, a substantially higher relative standing.

Smoothed orders strength shows some promise

Japan's machinery orders data show total orders at only their 65th queue or rank percentile with the core measure that excludes large projects showing the underlying less `lumpy' trend is much better off with a 91st percentile standing.

Teikoku readings show mediocrity and contraction

The earlier releases from Teikoku also for June largely show minor downshifting across sectors with standings that are mostly marginally above their respective median readings (a ranking of 50% is the median for each series). They do not see any of the strength in either service sector activity or that is indicated in machinery orders.

Service sector readings are helter-skelter

Japan's economy watchers index, a service-sector oriented index, downshifted more substantially in June, giving off a different signal from the tertiary index which is also a service sector gauge. Moreover, the standing of the economy-watchers gauge is below its 25th percentile for all its components, marking the sector as much weaker than the tertiary index which we rank based on the index level.

Recent releases are more hopeful but not a new trend

Broadly speaking, the two `freshest' (in the sense of most recently released not necessarily most -up-to-date) Japanese indicators are the relatively strongest indicators for June. But even these are equivocal. While the core orders ranking is relatively strong at its 91st percentile, the industrial sector business index component carries a weak 31st percentile ranking. In addition, the Markit manufacturing diffusion index carries a 27th percentile reading while the Teikoku Index carries a mid-50 percentile manufacturing sector ranking.

Summing up

Japan is going through a difficult time, trying to get some sort of stimulus/price boosting scheme in play and not having a lot of success. Of course, Japan is weighed down by structural factors like its shrinking population and also by its international linkages which find it plugged into its largest trade partner, China, a country where growth is also struggling to achieve growth targets. The topical gauges for June suggest that Japan is still not in any sort of growth acceleration mode. The reports among these that also have July observations (economy watchers, Markit and Teikoku) show slightly less weakness in July than in June. But the July diffusion data are still below the 50% mark for their raw readings (all three of these reports are diffusion indexes; a sub-50% reading points to ongoing contraction). In addition, the low rankings of the gauges broadly underscores that the readings are also well below established median values. Japan continues to struggle. There is no consistent evidence of any acceleration taking root.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief