Global| Jul 21 2020

Global| Jul 21 2020Japan's CPI Snakes Sideways

Summary

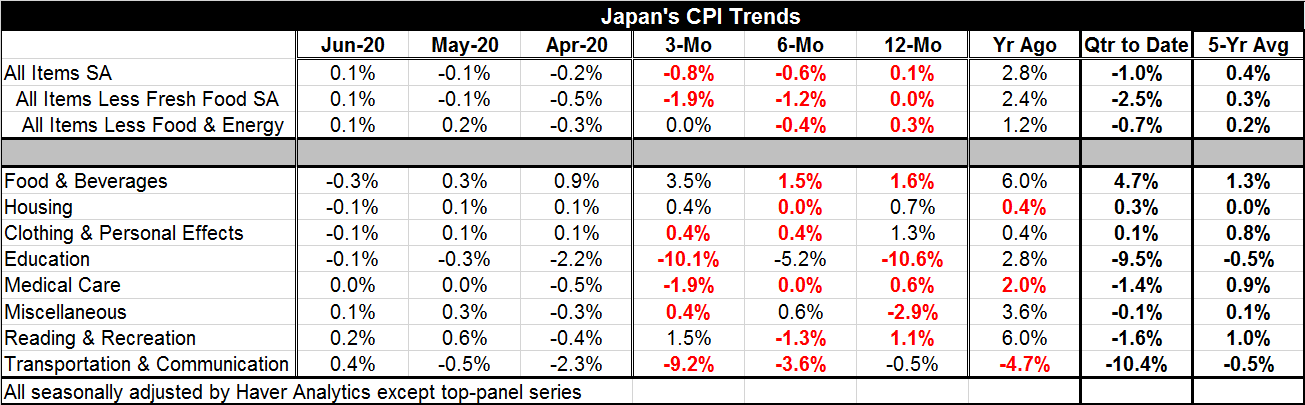

Japan's inflation continues to be moderate. The June result brought the first month-to-month gain in the headline since December. The first five months of the year produced inflation headlines that were either unchanged or lower [...]

Japan's inflation continues to be moderate. The June result brought the first month-to-month gain in the headline since December. The first five months of the year produced inflation headlines that were either unchanged or lower month-to-month. The headline series still is ‘trending lower' with weakening getting worse from 12-months to six-months and from six-months to three-months. The current month's pop up does arrest the long string of monthly deterioration even if it is not enough to undo the sequential trend weakening in prices. The trend for all items except food and energy, however, shows a more ambiguous sequential trend and two month-to-month increases in a row. These are the first pair of monthly increases that are back-to-back since November-December last year and that episode was an example of a triplet since the core also had risen in October. But on this occasion, there is an increase of 0.1% in June and 0.2% in May whereas the October-December run consisted of three gains of 0.1% each. However, all of this is hair-splitting and small potatoes since inflation in Japan is still flat or worse and the economy is still struggling.

Japan's inflation continues to be moderate. The June result brought the first month-to-month gain in the headline since December. The first five months of the year produced inflation headlines that were either unchanged or lower month-to-month. The headline series still is ‘trending lower' with weakening getting worse from 12-months to six-months and from six-months to three-months. The current month's pop up does arrest the long string of monthly deterioration even if it is not enough to undo the sequential trend weakening in prices. The trend for all items except food and energy, however, shows a more ambiguous sequential trend and two month-to-month increases in a row. These are the first pair of monthly increases that are back-to-back since November-December last year and that episode was an example of a triplet since the core also had risen in October. But on this occasion, there is an increase of 0.1% in June and 0.2% in May whereas the October-December run consisted of three gains of 0.1% each. However, all of this is hair-splitting and small potatoes since inflation in Japan is still flat or worse and the economy is still struggling.

Japan has no macroeconomic event that is driving it strongly or even firmly forward. Domestic indicators are uneven and still recovering from the effects of covid-19. Japan also finds itself in a poor global environment and one in which its main trade partners continue to have hostile relationships.

CPI components show an accelerating trend for food and beverage prices from 12-months to six-months to three-months. However, more categories have deceleration trends in progress such as for clothing & personal care, for medical care costs and for transportation & communication. However, a number of categories have mixed trends as well. Year-on-year only three categories show net price declines: education (-10.6%), miscellaneous (-2.9%) and transportations & communication (-0.5%). And those trends have been aided by the bottom falling out of global energy prices an event that now seems to have been arrested. Prices rise year-over-year for food & beverages (1.6%), clothing & personal items (1.3%), reading & recreation (1.1%), housing (0.7%), and medical care (0.6%). However, among those eight major CPI categories only three: housing, clothing & personal items and transportation & communication show acceleration from their 12-month ago annual pace of gain.

Closer up the quarter-to-date gains show prices falling in five of these categories and rising in only three. The five-year trends still show prices averaging declines in two of eight categories (education and transportation & communication). But housing prices average no change over the period and miscellaneous prices average an annual rise of just 0.1% per year over the last five years.

On balance, Japan still has a strong legacy of stable-to-weak prices. Growth has been weak as the population has continued to shrink. The Bank of Japan stimulus remains substantial, but there is little more to be done on that front. Japan continues to experience a very low inflation environment that was dragged lower earlier in the year as coronavirus disruptions dragged economic activity and prices lower. That episode seems to be coming to a close, but there is no clear change in Japan's price trends as a result.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief