Global| Mar 16 2015

Global| Mar 16 2015Japan's Consumer Confidence Hovers at Low Reading

Summary

Consumer confidence in Japan has averaged a reading of 39.4 over the last 12 months. This month's pick-up to 40.7 in February from 39.1 in January barely improves on its one-year average. Moreover, the three-month and six-month [...]

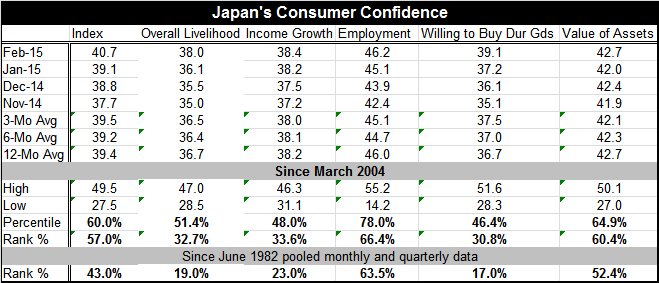

Consumer confidence in Japan has averaged a reading of 39.4 over the last 12 months. This month's pick-up to 40.7 in February from 39.1 in January barely improves on its one-year average. Moreover, the three-month and six-month averages are low and stagnant. This month's rise is not much evidence that Japan is breaking out of its consumer slump. There is a one-month improvement but no real change in momentum.

Consumer confidence in Japan has averaged a reading of 39.4 over the last 12 months. This month's pick-up to 40.7 in February from 39.1 in January barely improves on its one-year average. Moreover, the three-month and six-month averages are low and stagnant. This month's rise is not much evidence that Japan is breaking out of its consumer slump. There is a one-month improvement but no real change in momentum.

The rise in Japan's consumption tax meant to put the country on a more sustainable fiscal path has instead continued to harm consumer sentiment and to hold back economic expansion. This month's reading of 40.7 for consumer confidence still sits in the 43rd percentile of its historic queue of readings marking it as a reading that is lower only 43% of the time and higher 57% of the time- not an enviable positioning.

Monthly survey responses to the assessment of overall livelihood rose nearly two points on the month but sit is an even weaker and low 19th percentile of its historic range. There is little sign of building momentum here.

Income growth received only a slightly improved response in February with the index nudging up to 38.4 from 38.2 in January. The position of the reading is in its lower 23rd percentile, still an extremely weak reading and again without any evidence of improved momentum.

The employment response in February rose to a reading of 46.2 from 45.1 in January. While there is a better queue standing for this variable, in its 63rd percentile, the reading is still only moderately firm and the series shows no broad improvement. However, there is a hint of improved momentum over the last three months.

Consumers' willingness to buy durable goods rose nearly two points in February from its January level but still sits weakly at the 17th percentile of its historic queue of data. Here too there is some evidence of improvement over the last three months.

Japanese consumers see the value of their assets as relatively more secure standing at it does at the 53rd queue percentile, up slightly on the month and above the midpoint (50%) of its historic queue of data. Still, this is not a strong reading. Moreover, there is little evidence of any improvement in this assessment over the past year or over shorter periods.

On balance, Japanese consumers still seem to be shell-shocked by the consumption tax hike with overall growth held back by slow population growth and a weak global economy. While the yen is falling, there is less manufacturing activity in Japan than there used to be, so the weak yen does not help the economy as much as it would have in the past. Of course, Japan has been importing a lot of oil, but there is no sign from consumers that lower prices have helped their mood much.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief