Global| Nov 02 2017

Global| Nov 02 2017Japan's Consumer Confidence Claws Its Way Higher; Can It Continue?

Summary

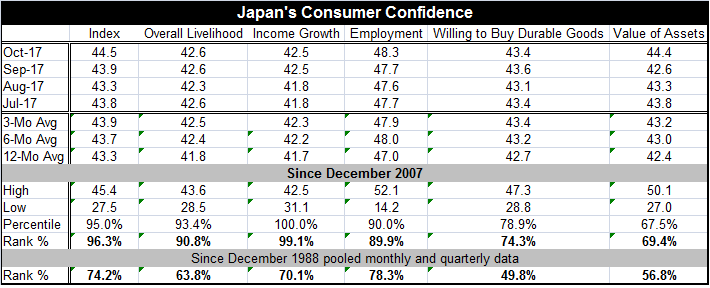

Dots represent quarterly confidence points; the line connects dots since the report has become monthly. Japan's consumer confidence moved up to 44.5 in October form 43.9 in September. It was last stronger in September 2013. And then [...]

Dots represent quarterly confidence points; the line connects dots since the report has become monthly.

Dots represent quarterly confidence points; the line connects dots since the report has become monthly.

Japan's consumer confidence moved up to 44.5 in October form 43.9 in September. It was last stronger in September 2013. And then it was only stronger sporadically as fluctuated in a higher plane then registered lower readings. Confidence was higher than 44.5 in three months over the span from September 2013 to March 2013 but on that period it only average 44.2, below October's 44.5 reading. Confidence in Japan has not been 'consistently better' than this level since May 2007 and before, about one decade ago.

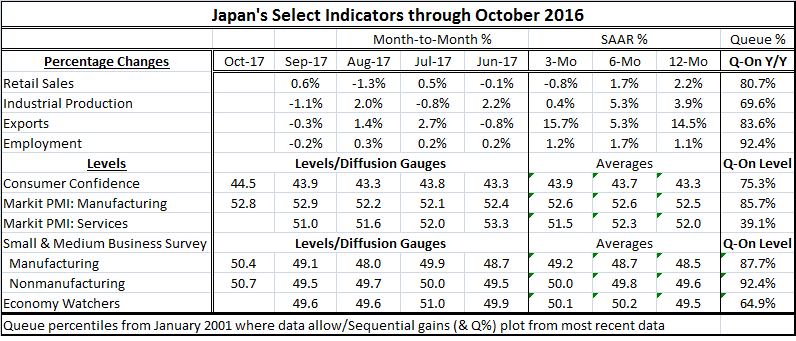

I present consumer confidence along with a batch of other macroeconomic data. Consumer confidence in terms of its percentile standing seems to be 'fairly positioned' among other economic indicators. That is to say that the queue percentile standing for consumer confidence is 'in the mix' at its 75th percentile. Retail sales have an 80th percentile standing, employment has a 92nd percentile standing. Manufacturing has an 85th percentile standing for its PMI, compared to a much lower 39th percentile standing for services. Industrial production has a 69th percentile standing. While small business gauges for manufacturing and nonmanufacturing are stronger at a manufacturing standing of 87% and nonmanufacturing at 92%. The economy watchers index has a 64th percentile standing. Placed among these myriad reports from October and September, the consumer confidence index is stacked in the lower middle of this grouping. Its positioning seems 'about right' partly because consumers are very jobs centric. And while the employment standing is very high, the readings for the services sector overall and for the economy watchers survey (which is a service sector barometer) are weaker and the services sector is the main job creation sector. Also consumer spending is not ranked too differently from consumer confidence.

Overall consumer confidence shows that its 12- to 6- to 3-month standings are on the rise. However, on that same progression, retail sales are losing steam and employment growth has an undefinable trend. Manufacturing is clawing higher in the guise of its PMI, but it has weakened over three months in its industrial production format. Small businesses show growth progress on the timeline for both manufacturing and nonmanufacturing. But the Markit services gauge backs off as does the economy watcher index in the recent three-month period.

Japan's trends are lackluster. However, its year-on-year gauges for retail sales, industrial production, exports and employment are gaining and its overall PMI gauges for manufacturing and services signal expansion. But the consumer confidence gauge is also a diffusion index. And while it is posting some of its strongest gains since it was consistently higher a decade ago, the current reading still shows that there is more pessimism on balance than optimism (the gauge is below 50). Also the small business gauges, while clearly rising, are at an absolute standing below 50 over 12 months along with the economy watchers index. But as of October, the economy watchers index and the nonmanufacturing small business index have improved and neither is showing declines any more. However, the small business manufacturing index is still showing contraction.

The details of the consumer confidence survey show us that since 2007 the overall livelihood reading, which was steady in October, has a 90th percentile standing and has been higher only 10% of the time. However, in a broader historic context, if we pool the monthly and quarterly data, the current observation standing sinks to the 63.8 percentile for overall livelihood. This tells us that historically Japanese conditions are only moderate, but they are some of the best conditions Japan has seen since 2007.

As we read across the table, we find the same sorts of standings for the since December 2007 period compared to the full period across the confidence components. Income growth in October has an unchanged reading with September and together these two months are among the highest readings since December 2007 (99.1 percentile!), yet only with a 70.1 percentile standing more broadly. Employment performance has another gap between ranking in the two periods and the employment gauge at about a 10 percentage point standing gap between the two periods. Willingness to buy goods, however, shows a setback over the longer period (reading below 50) with conditions actually below their median. In the discussion above, we pointed to the relative weakness in retail sales. Here we see that the willingness to buy slipped month-to-month to 43.4 in October from 43.6 in September. Its since-December-2007 standing is in its 74th percentile while its full period standing is just below its median at its 49th percentile. The value of assets also has a low reading. While this metric improved month-to-month rising to 44.4 in October from 42.6 in September, it has only a 69th percentile standing since December 2007 and a 56th percentile standing more broadly.

All the focus in Japan is on Abenomics and the monetary policy at the Bank of Japan. These policies have helped to get and keep Japan growing and have kicked it up out of its deflation funk. But policies have fallen short of achieving the 2% inflation rate sought by the BOJ. Of course, the BOJ is not alone in this failure as the U.S. has failed on this score and so has the ECB. Against that background, it seems appropriate to applaud Japan for its success at stabilization and at eliminating deflation - a harder job for it to accomplish with a shrinking population - than to berate it for its failure to hit a 2% inflation target when nobody else can hit it either.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief