Global| Jan 10 2017

Global| Jan 10 2017Japan's Confidence: Bounce to Nowhere

Summary

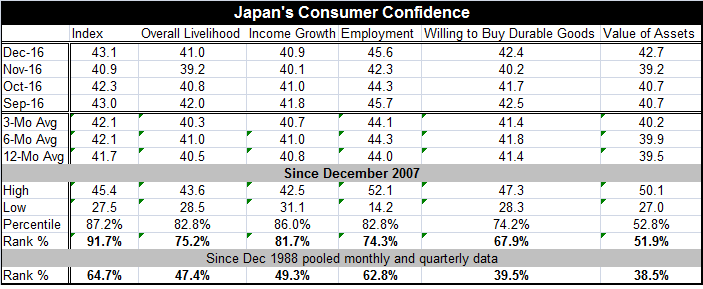

Japan's consumer confidence, a diffusion measure, rose sharply month-to-month, regaining the ground it lost on the previous month's sharp drop. Despite the jump, there is little lift in the series that lingers below the neutral mark [...]

Japan's consumer confidence, a diffusion measure, rose sharply month-to-month, regaining the ground it lost on the previous month's sharp drop. Despite the jump, there is little lift in the series that lingers below the neutral mark of 50 as it has since 2006. Still, since early 2014, there is a clear but very mild uptrend that has been in place for this index of consumer attitudes.

Japan's consumer confidence, a diffusion measure, rose sharply month-to-month, regaining the ground it lost on the previous month's sharp drop. Despite the jump, there is little lift in the series that lingers below the neutral mark of 50 as it has since 2006. Still, since early 2014, there is a clear but very mild uptrend that has been in place for this index of consumer attitudes.

Since 2007, going back to when the global financial crisis struck, the consumer confidence index has a queue (or rank) standing of 91.7% marking it in the top 10% of its queue of values over that period. Its components generally have more moderate standings. Evaluated over a much longer period, the headline index has only a 64th percentile standing reflecting the fact that since the financial crisis struck the overall confidence index has been weak and as the high-low data show have a high reading of only 45.4 still short of the neutral reading of 50. On data back to December 2007, only two components have registered a reading at or above 50 at any time on that timeline.

The rank percentile since 2007 show the relative strongest readings are for income growth (81.7%), overall livelihood (75.2%) and employment (72.8%). Of those, only income growth breaks into the stronger 80th percentile range. At even lower levels are consumer willingness to purchase goods (67.9%) and value of asset perceptions (51.9%); the later barely makes it above is median standing which occurs at the 50th percentile mark. And remember that we are looking at queue rankings of data that themselves are diffusion indices and all components are below neutral themselves (let alone below their medians) as consumers find conditions still below neutral for all the consumer confidence components.

The lower row of rankings reevaluates the consumer gauges on a broader timeline since 1988. On that basis, all of the evaluations drop precipitously with only two, the headline and employment, above their longer term median values as of December. There are two messages here. One is that the consumer attitudes have been slowly improving in the post financial crisis and post-recession period. The second is that nonetheless in this period consumer attitudes are still substantially reduced compared to what they used to be before that set of calamities struck.

On balance, there is still a very slow up-creep of improvement to Japan's consumer confidence. Despite this improvement, the overall tone remains negative as it has since 2006. While consumers are reasonably copacetic about their livelihood and income and are as a result reasonably disposed to buy durable goods, they lack confidence in employment conditions and are not pleased with the value of their assets. These latter two issues restrain them in their willingness to buy durable goods.

The BOJ continues to press ahead with its aggressive program to pump in bank reserves and to control the yield curve; meanwhile, Japan's manufacturing PMI gauge has been slowly improving. Japan's manufacturing PMI is above 50 for four months running. The economic diffusion gauges on sectors from Teikoku show slow but ongoing progress across sectors through November, their freshest data points. The services sector focused economy-watchers index bottomed out in June and has been on a steady improving trend ever since. The news from Japan is steadily improving, but it is also very slowly improving. The sharp jump in the headline for consumer confidence this month belies the slowness of the speed by which progress is being made.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief