Global| Nov 11 2009

Global| Nov 11 2009Japan Machinery Orders Dig Out

Summary

Japan’s machinery orders rose by 6% in September. Core machinery orders spurted by 10.5%. Foreign demand is the whole of the pickup as domestic orders fell by 5.4% while foreign orders rose by 25.9% both in September. The three month [...]

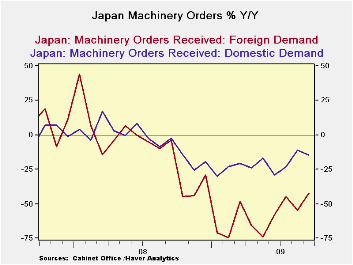

Japan’s machinery orders rose by 6% in September. Core machinery orders spurted by 10.5%. Foreign demand is the whole of the pickup as domestic orders fell by 5.4% while foreign orders rose by 25.9% both in September.

The three month metrics show that core orders are still not out of the woods; their three month growth rate is just 2.9% annualized the same as their six month growth rate. Still these two horizon growth rates are better than the -21.8% Year-over-year performance. Core machinery orders are no longer falling but they are not rising very rapidly.

The same sort of shortfalls exist across countries

Moreover Japan like Germany is benefiting from external growth. Over three months, foreign demand is up at a 180% annual rate that is an acceleration from a 60.4% annual rate over six months and those numbers reverse the 42% drop in foreign demand Yr/Yr. Still, domestic demand is wanting. Over three months it is up at a 19.9% pace, better than the -1% rate over six months, and that is an improvement from the drop of 14.9% Yr/Yr.

On balance Japan’s orders are on the mend. Even domestic

orders are showing a push into positive territory. But these series are

very volatile and given the volatility the recent domestic growth

figures are not very impressive. Much more impressive is the growth in

foreign orders that seems to be jumpstarting Japan as a whole.

As the global economy turns to recovery one key challenge is going to be to see if surplus and deficit countries begin to make adjustments. Note that Japan and Germany, traditional exporting powers, continue to get a lot of their stimulus from overseas. China’s trade surplus was up this month. How is the US going to keep the lid on its deficit if everyone else is running surpluses? Large structural trade imbalances and the persisting investment flows they imply was one of the main sources of instability in this past cycle. Is anything going to change?

| Japan Machinery Orders | |||||||

|---|---|---|---|---|---|---|---|

| m/m % | Saar % | ||||||

| SA | Sep-09 | Aug-09 | Jul-09 | 3-Mos | 6-Mos | 12-Mos | 12-Mo Ago |

| Total | 6.0% | -1.9% | 7.5% | 56.1% | 2.6% | -26.5% | -2.5% |

| Core Orders* | 10.5% | 0.5% | -9.3% | 2.9% | 2.8% | -21.8% | -3.7% |

| Total Orders | |||||||

| Foreign Demand | 25.9% | -15.7% | 21.8% | 180.0% | 60.4% | -42.2% | -3.5% |

| Domestic demand | -5.4% | 7.1% | 3.4% | 19.9% | -1.0% | -14.9% | -2.8% |

| * Excl ships and electric power | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief