Global| Oct 02 2020

Global| Oct 02 2020Japan and Europe's Jobless Rates Rise in August

Summary

Japan's unemployment rate has risen for the second month in a row. The EMU unemployment rate has risen for five months in a row. The spread of infection has played a role in this. Japan had its peak for infections early in August and [...]

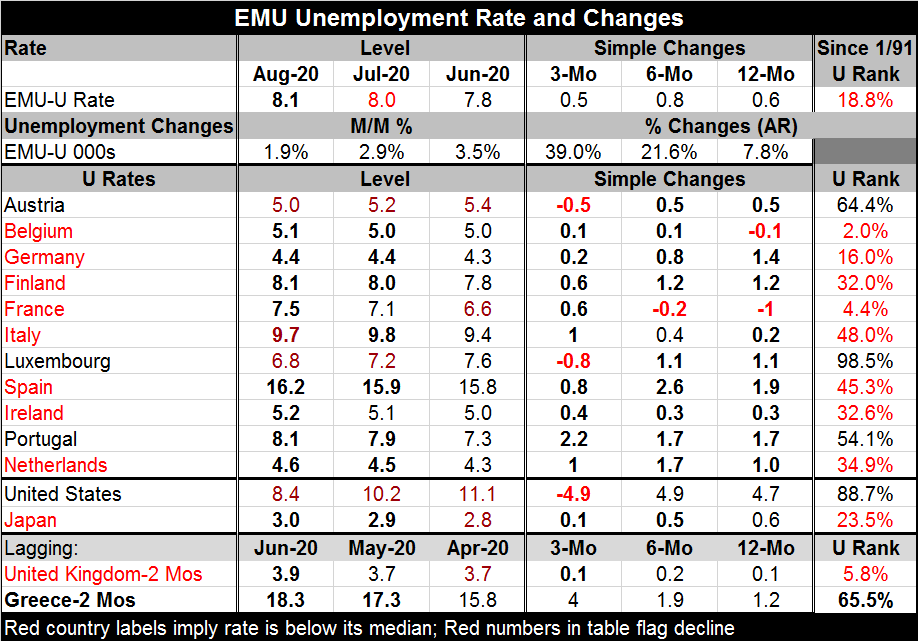

Japan's unemployment rate has risen for the second month in a row. The EMU unemployment rate has risen for five months in a row. The spread of infection has played a role in this. Japan had its peak for infections early in August and since then levels have continued to ease lower. But in Europe, infection rates are rising in general. Infection rates are on an upswing for the large economies Germany, France and Italy. Spain has also seen an upswing to a high level, but it is showing signs of peaking in Spain even as the city of Madrid has taken some stern actions.

Japan's unemployment rate has risen for the second month in a row. The EMU unemployment rate has risen for five months in a row. The spread of infection has played a role in this. Japan had its peak for infections early in August and since then levels have continued to ease lower. But in Europe, infection rates are rising in general. Infection rates are on an upswing for the large economies Germany, France and Italy. Spain has also seen an upswing to a high level, but it is showing signs of peaking in Spain even as the city of Madrid has taken some stern actions.

These infection patterns will have a lot to do with what happens to unemployment going forward.

In August among 11 of the early EMU members, eight are experiencing increases in their unemployment rates in August compared to three with unemployment rates falling. Unemployment rates fall in Italy, Luxembourg and Austria. They rise elsewhere including Greece (on a lagged basis) and in the United Kingdom (no longer an EU member but an important European economy).

Only three countries have unemployment rates above their medians since 1991. Those are Austria Portugal and Luxembourg.

Looking more broadly, unemployment rates are higher year-on-year by 0.6 percentage points in the EMU, by 4.7 percentage points in the United States, by 0.1 percentage point in the U.K. and by 0.6 percentage points in Japan. Only Belgium and France have unemployment rates that are lower over 12 months.

The queue percentile standing data show that several important economic regions have unemployment rates at about the 20th percentile of their historic queue. That is true for the EMU area as a whole and for Japan. The U.S. has one of the highest queue standings for unemployment at an 88.7 percentile standing; only Luxembourg has a higher standing than the US. The U.K. has a standing at its 5.8 percentile, at the other end of the spectrum. Only Belgium and France have lower standings than the U.K.

Of course, we began this discussion speaking about the virus and its developments and trends. Its developments may be about to let Japan open up a bit more and accelerate growth to reduce its unemployment. In Europe, not only do the incentives from the virus go the other way, but there are no new stimulus plans afoot. In the U.S., stimulus programs have run out and there is a half-hearted effort to renew them. But with nothing new in the way of support done in the U.S. and globally, as recoveries slow, and with these unemployment rates rising, there are more corporate layoffs being announced that will in all likelihood extend this trend of rising rates of unemployment. Businesses are looking at the still present virus and the lack of commitment by governments then deciding to play it safe and slim down operations. If too many businesses take that tact, we could see growth itself backsliding - so much for a V-shaped recovery.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief