Global| Aug 05 2016

Global| Aug 05 2016Italy Shows Second Monthly IP Drop in a Row

Summary

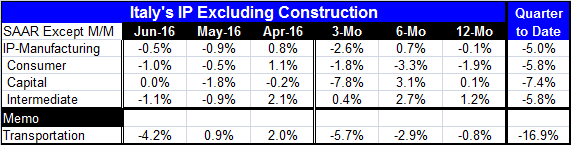

Italian industrial output fell hard for the second month in a row. However, output made a strong 0.8% gain in April. Even so, output is falling at a 5% annual rate in Q2 with declines across all sectors. Italian manufacturing is [...]

Italian industrial output fell hard for the second month in a row. However, output made a strong 0.8% gain in April. Even so, output is falling at a 5% annual rate in Q2 with declines across all sectors. Italian manufacturing is putting in a poor quarter.

Italian industrial output fell hard for the second month in a row. However, output made a strong 0.8% gain in April. Even so, output is falling at a 5% annual rate in Q2 with declines across all sectors. Italian manufacturing is putting in a poor quarter.

Beyond manufacturing, Italy remains weak. ISAE measure of consumer and business confidence show flat business confidence for a number of months with consumer confidence well off peak and falling. Real retail sales in Italy hit a `peak' growth rate below 2% around mid-2015 and retail sales have been weakening with negative year-on-year growth for the past several months. Industrial orders show total and foreign orders are falling year-over-year.

While the drop in Italian IP was not expected, it can't be considered very surprising against the backdrop of what is happening to the economy in Italy.

The Italian IP drop is also in step with Italy's manufacturing PMI gauge falling to 51.2 in July from 53.5 in June, a really sharp month-to-month pullback. Italy's manufacturing standing in PMI terms is nearly on top of its median value since early-2011. Italy's services PMI ticked-up ever so slightly in July, but both the manufacturing and services sectors show their moving averages slipping over the past year. Italy appears to be slowing and the IP drop should not be regarded as a fluke.

An added issue for Italy is the question of how the Italian banking sector's problems are going to be resolved. Italian banks are woefully undercapitalized. Italy did not take steps to recapitalize them earlier because it did not have fiscal room to do it. Then Cyprus' banking crisis hit and caused the EU to adopt the no-bail-out rule and to require `bail-ins' for troubled institutions. Bail-ins refer to making stock- and bond-holders take first losses meaning that in a really troubled institution they are wiped out before any public money could go in. Such an approach is a nonstarter politically in Italy. Italy is in a tough spot perhaps the toughest of any EMU economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief