Global| Apr 21 2014

Global| Apr 21 2014Italy's Orders Weaken as Fiscal Policy Shifts

Summary

Industrial orders weakened in Italy in February. They fell by 3.1% but only after rising by 4.7% in January. Still, January represents a partial rebound from a 4.8% drop in December. Obviously, there has been a good deal of volatility [...]

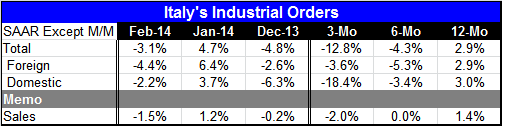

Industrial orders weakened in Italy in February. They fell by 3.1% but only after rising by 4.7% in January. Still, January represents a partial rebound from a 4.8% drop in December. Obviously, there has been a good deal of volatility in Italian orders. The graph shows that the year-over-year trends in domestic and foreign orders are working higher with irregularity and may have stopped their ongoing rise. But the table shows that the trends inside 12 months clearly are working lower. The annual rate decline over three months is deeper than for 6 months and both are weaker than the year-over-year gain of 2.9% Both foreign and domestic orders show the same dissipating trends, but for domestic orders the weakness in the last three months is pronounced (-18.4% at an annual rate).

Industrial orders weakened in Italy in February. They fell by 3.1% but only after rising by 4.7% in January. Still, January represents a partial rebound from a 4.8% drop in December. Obviously, there has been a good deal of volatility in Italian orders. The graph shows that the year-over-year trends in domestic and foreign orders are working higher with irregularity and may have stopped their ongoing rise. But the table shows that the trends inside 12 months clearly are working lower. The annual rate decline over three months is deeper than for 6 months and both are weaker than the year-over-year gain of 2.9% Both foreign and domestic orders show the same dissipating trends, but for domestic orders the weakness in the last three months is pronounced (-18.4% at an annual rate).

Italy has just announced a program of tax cuts to try to arrest the domestic weakness. Income taxes are to be cut by about 80 euros per month for individuals earning less than 26,000 euros per year. There is also to be a tax cut for businesses.

These fiscal developments come at a time that Italy is also being pressured to keep its budget deficit to 3% of GDP. The tax cutting will not help achieve this goal unless it has a pronounced impact on growth. The tax cuts are supposed to be offset by a selection of not fully articulated spending reductions.

Italy's economy is struggling and the trends for industrial orders make it clear that the downward pressures have not abated even deep into its ongoing recession. Italy's per capita income is still at the same position it was in 1997, a testament to the degree of weakness in one of the euro area's largest economies. The tax cuts are an attempt to restore some disposable income to consumers.

Spain, the fourth largest euro area economy, is improving; the proportion of bad loans at Spanish banks fell from a record high in January. France, the second largest euro area economy, is still struggling. Germany, the largest euro area economy, continues in the cat-bird's seat. But even overall confidence in Germany has taken a hit in the wake of the Ukraine crisis. With the top euro area economies seeing various degrees of headwinds, it's clear that ECB policy is still in play.

Italy is the most sluggish of the four large EMU economies. The tax situation is the result of new Italian Prime Minister Matteo Renzi fulfilling a campaign promise. But it also is a risky move given the continued pressure on euro area countries to hit their budget constraints. Italy is getting more desperate and the euro area recovery is not as clearly on track as we would like to see it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief