Global| Nov 27 2020

Global| Nov 27 2020Italy's ISAE Sector Confidence Rebounds Then Retreats

Summary

The Italian business and consumer confidence readings are excellent examples of what much of Europe is going through right now. Italian confidence was hard-hit on the encroaching virus early in the year. It then snapped back sharply [...]

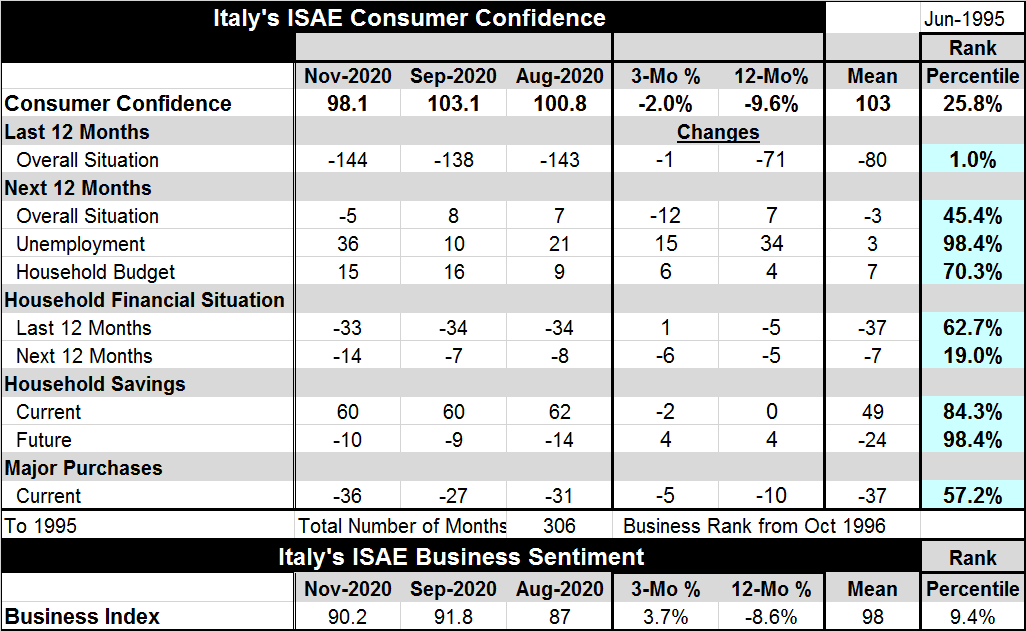

The Italian business and consumer confidence readings are excellent examples of what much of Europe is going through right now. Italian confidence was hard-hit on the encroaching virus early in the year. It then snapped back sharply if not fully. And now with virus spreading, confidence is again weakening with a sharp stepdown from the consumer and less sharp stepdown for businesses. But business confidence while stepping down less on the month is already at a lower ebb than consumer confidence. The business confidence index has only a 9.4 percentile standing while its consumer index counterpart has a 25.8 percentile standing. Although the consumer standing is much higher in percentile terms, both in fact are very weak in practical terms.

The Italian business and consumer confidence readings are excellent examples of what much of Europe is going through right now. Italian confidence was hard-hit on the encroaching virus early in the year. It then snapped back sharply if not fully. And now with virus spreading, confidence is again weakening with a sharp stepdown from the consumer and less sharp stepdown for businesses. But business confidence while stepping down less on the month is already at a lower ebb than consumer confidence. The business confidence index has only a 9.4 percentile standing while its consumer index counterpart has a 25.8 percentile standing. Although the consumer standing is much higher in percentile terms, both in fact are very weak in practical terms.

These indexes make some of the push back and furor in Italy against the new restrictions meant to contain spread of the virus a bit easier to understand. Maybe that push back still is not right, but these statistics should illuminate the mindset of Italian households.

The Italian assessment of the overall situation over the last 12 months dropped to a survey value of -144 in November from -138. It takes on a one-percentile standing – that means it has rarely ever been weaker. That means that Italians, coming into this survey period, were not happy campers.

Over the next 12 months, the survey value for the overall situation drops to -5 from +8 and registers a 45.4 percentile standing. That is not terrible, but it is below its historic median (rank medians occur at a percentile standing value of 50) and keeps the environment assessment ‘below normal' after a period that as rated as abysmal (-144!).

What worse (worst?) is that the unemployment response jumps to +36 from +10 to a 98.4 percentile standing. The fear of unemployment in Italy is palpable. This is the key response in the table and represents the overriding concern of the Italian people. They are more worried/certain of unemployment now than ever (That is almost literally true, not just an expression!). The problem is that they have lived through one shutdown and did not like it and now they fear another dose of the same ‘medicine.'

The household financial situation over the last 12 months actually has improved a tick on the month to -33 from -34 as it took on a 62.7 percentile (moderate) standing. But over the next 12 months, the expected situation reading dropped to -14 from -7 and plunged to a 19.0 percentile standing, a lower one-fifth historic reading.

The environment for making major purchases drops to a raw survey reading of -36 from -27 and to a standing at its 57.2 percentile- still above its historic median. It is a bit hard to square this standing on making a major purchase with the extremely high standing on unemployment fears, but these are the survey results I only report them- I cannot psycho-analyze them.

Summing up

Still, the survey is quite clear that the fear of unemployment in Italy is exceptionally high and the fear of how the future will unfold has ratcheted higher as well. The business confidence index slipped on the month and overall has a much more dire standing than for the confidence for households. However, together these are disturbing results. They explain a lot about why Italians are uncomfortable with the notion of further economic restrictions- right or wrong. And while this survey is not any more probing and specific, there is also anxiety among those who think ahead about what the post-covid-19 world will look like and how all this debt that has been accumulated to get through it is going to be handled. In these respects, Italy hardly stands alone.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief