Global| Jul 25 2007

Global| Jul 25 2007Italy's Business Confidence Indicator Falls

Summary

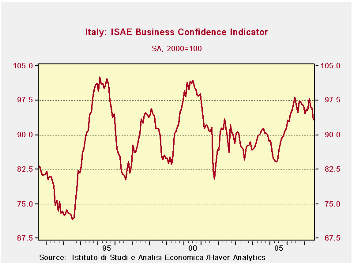

Business confidence in Italy is still at a reasonably strong reading. The index fell this month to 93.3 from 95.9. The months drop is relatively sharp. The chart pattern for the index is much more ominous than for most EMU members. [...]

Business confidence in Italy is still at a reasonably strong reading. The index fell this month to 93.3 from 95.9. The month’s drop is relatively sharp. The chart pattern for the index is much more ominous than for most EMU members. Italy has been the weakest of the large EMU countries for some time. We maintain that the place to look for vulnerability to the strong euro value is not in the EMU’s strongest economy, Germany, but in some of its weaker members. Italy is a case in point.

Percentile readings of the ISAE survey components are mostly in the 60 to 70 percentile range. But residing in the 61.4 percentile of their range, foreign orders are one of the weaker categories. This is a reading that would be expected to get weak if Italy developed competitiveness problems. Consumer goods reading are among the weakest by industry group with percentile readings that fall out of the 60th percentile in the 50s. But the loss in momentum is greater for investment goods than for consumer goods even though the consumer goods raw readings are weaker in absolute terms.

On balance, Italy appears to have lost a lot of momentum. Its readings are reassuring and are nonetheless still solid. We would start to get more worried about Italy and the hint of the loss in competitiveness if the drop in the index we see this month extends itself in the coming months. For now, it is just a warning and possibly a bit of mid-summer volatility...but also possibly something more.

| Since January 1999 | 4COLSPAN | |||||||||

| Jul-07 | Jun-07 | May-07 | Apr-07 | Percentile | Rank | Max | Min | Range | Mean | |

| Biz Confidence | 93.3 | 95.9 | 96 | 97.9 | 60.3 | 35 | 102 | 80 | 21 | 92 |

| TOTAL INDUSTRY | ||||||||||

| Order books & Demand | ||||||||||

| Total | -3 | 2 | 2 | 3 | 60.0 | 29 | 13 | -27 | 40 | -10 |

| Domestic | -2 | 0 | 0 | 2 | 68.3 | 17 | 11 | -30 | 41 | -12 |

| Foreign | -6 | -1 | 1 | -3 | 61.4 | 32 | 11 | -33 | 44 | -14 |

| Inventories | 8 | 5 | 5 | 5 | 79.2 | 20 | 13 | -11 | 24 | 4 |

| Production | 7 | 9 | 6 | 5 | 69.4 | 11 | 22 | -27 | 49 | -6 |

| INTERMEDIATE | ||||||||||

| Order books & Demand | ||||||||||

| Total | 0 | 2 | 3 | 5 | 65.5 | 23 | 19 | -36 | 55 | -11 |

| Domestic | -3 | -1 | 1 | 4 | 60.4 | 20 | 16 | -32 | 48 | -13 |

| Foreign | -1 | 1 | 3 | -2 | 67.2 | 22 | 18 | -40 | 58 | -12 |

| Inventories | 7 | 5 | 2 | 4 | 75.9 | 12 | 14 | -15 | 29 | 0 |

| Production | 4 | 6 | 8 | 9 | 60.3 | 19 | 27 | -31 | 58 | -7 |

| INVESTMENT GOODS | ||||||||||

| Order books & Demand | ||||||||||

| Total | 12 | 19 | 17 | 20 | 70.1 | 16 | 32 | -35 | 67 | -6 |

| Domestic | 5 | 9 | 10 | 13 | 66.1 | 16 | 25 | -34 | 59 | -11 |

| Foreign | 3 | 8 | 13 | 9 | 64.3 | 26 | 23 | -33 | 56 | -8 |

| Inventories | 9 | 9 | 7 | 6 | 70.3 | 15 | 20 | -17 | 37 | 1 |

| Production | 20 | 23 | 18 | 12 | 77.3 | 11 | 35 | -31 | 66 | -2 |

| CONSUMER GOODS | ||||||||||

| Order books & Demand | ||||||||||

| Total | -4 | -2 | -5 | -8 | 56.8 | 24 | 15 | -29 | 44 | -10 |

| Domestic | -7 | -6 | -10 | -10 | 58.3 | 35 | 8 | -28 | 36 | -12 |

| Foreign | -7 | -7 | -6 | -12 | 59.6 | 20 | 12 | -35 | 47 | -15 |

| Inventories | 9 | 7 | 11 | 7 | 76.9 | 17 | 15 | -11 | 26 | 4 |

| Production | 3 | 2 | -5 | -5 | 77.8 | 10 | 11 | -25 | 36 | -7 |

| Total number of months: | 100 | 6COLSPAN | ||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief