Global| Mar 24 2008

Global| Mar 24 2008Italy Retail Sales and Consumer Confidence Sag

Summary

Italy’s retail sales edged up in January, rising by 0.2% in nominal terms, likely a decline in volume terms given the recent pace of inflation. Over the past three months, sales values fell at a 0.4% annual rate. And, overall value [...]

Italy’s retail sales edged up in January, rising by 0.2% in

nominal terms, likely a decline in volume terms given the recent pace

of inflation. Over the past three months, sales values fell at a 0.4%

annual rate. And, overall value growth has been eroding ever so

slightly over this period. In the first quarter of 2008 value growth is

up at a 0.5% annual pace and at a stronger 0.7% pace for food,

beverages and tobacco – both likely representing volume declines.

Italy’s retail sales edged up in January, rising by 0.2% in

nominal terms, likely a decline in volume terms given the recent pace

of inflation. Over the past three months, sales values fell at a 0.4%

annual rate. And, overall value growth has been eroding ever so

slightly over this period. In the first quarter of 2008 value growth is

up at a 0.5% annual pace and at a stronger 0.7% pace for food,

beverages and tobacco – both likely representing volume declines.

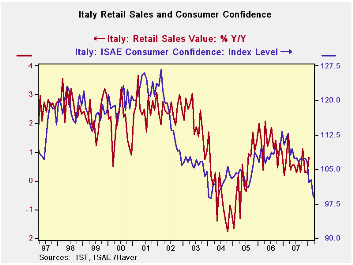

The chart at the top shows the ISAE consumer sentiment index plotted against retail sales Yr/Yr. Notice that the ISAE index plotted in its raw levels format tends to lead the Yr/Yr decline in retail sales: Sentiment peaks first and rebounds first. It gives reasonably good signals about what retail sales are about to do. In the recent period the weak consumer sentiment readings are pointed to further weakness in Italy’s already weak retail sales.

Italy’s HICP is rising at a 2.9% pace in Q1 (also through January) and its core is up at a 1.5% pace. But in terms of Italy’s own domestic inflation indicator (NIC) inflation is at a 5% pace in the first quarter or 4.6% excluding tobacco (NIC ex-tobacco). Food prices alone in Italy are up at a 5.8% pace in Q1.

As in the table above these inflation statistics for the first quarter growth rates take the January level over the Q4 average (centered in November) and compound that pace. Italy’s Q1 inflation calculated on that same basis produces some dismal implicit estimates of ‘retail sales growth (-2.5% to -4.5% depending on the deflator used). Inflation is clearly outstripping the nominal growth rates for sales in these comparisons by a wide margin. Italy is the most severely impacted economy of the EMU Big Three or EU Big Four (i.e. Germany, France & Italy for EMU, adding the UK for EU).

All of the EMU nations are having a hard time getting retail sales to grow. (The EU’s UK retail sales are an exception to most of the rest of Europe). Germany continues to look for the consumer to fill in some gaps. But flagging confidence is an issue and the EMU industrial sector is slowing. Fear seems to have gripped the EMU nations as the euro has climbed in value despite policymakers extolling European strength and flexibility, and growth has continued to be registered. Someone is either worried about nothing or someone else is whistling past the graveyard. Who is out of touch? Is it the consumer whose pull back is reminiscent of the consumer in the fetal position, or is it the policymaker who is trying to put a brave face on an ugly situation? I report, you decide… For the moment we are in opinion-land on this or deeply into shrink-o-nomics as we try and assess the state of mind of the government official vs the consumer.

| Italy Retail Sales Growth | ||||||||

|---|---|---|---|---|---|---|---|---|

| mo/mo % | At annual rates | |||||||

| Nominal | Jan-08 | Dec-07 | Nov-07 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | Qtr-to-Date |

| Retail Trade | 0.2% | 0.0% | -0.3% | -0.4% | 0.9% | 0.8% | 0.2% | 0.5% |

| Food Bev & Tobacco | 0.1% | 0.1% | -0.1% | 0.3% | 1.9% | 1.7% | -0.3% | 0.7% |

| Clothing&Furniture | 0.7% | 0.2% | -1.5% | -2.6% | 0.4% | 0.7% | 0.5% | 1.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief