Global| Aug 27 2008

Global| Aug 27 2008Italy: Consumer Confidence Rebounds but Remains Very Weak

Summary

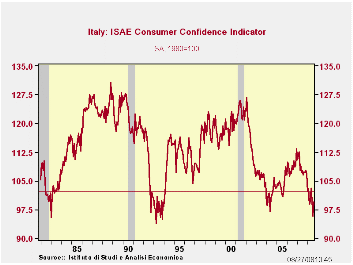

Consumer confidence rebounded in Italy to 99.5 In August from 95.8 in July. This is a nice bounce but it still leaves the index at a very low level. The best guess is that the pop in confidence stems from the drop in global oil prices [...]

Consumer confidence rebounded in Italy to 99.5 In August from

95.8 in July. This is a nice bounce but it still leaves the index at a

very low level. The best guess is that the pop in confidence stems from

the drop in global oil prices and the positive impact that has on short

term consumer budgets. Price trends over the next 12 months improved

slightly this month (to 23 from 23.5) and past price trends were

assessed as a lot lower this month as oil prices broke. The drop in

expected price trends is the first break in the uptrend in two months.

The overall situation is assessed as better at a reading of

-30 up from -35 last month. But that reading is still in the 14th

percentile of its historic range, a weak position. The household budget

improved sharply month-to-month, most likely the result of lower energy

costs. Its improvement to +2 from -7 elevates it to the 22nd percentile

of its range, still weak but less severe. It’s the biggest one-month

shift in this category since at least December of 1998, although shifts

of 8 points m/m have been recorded. As you might expect if the sharp

drop in world oil prices is behind the improvement in sentiment

spending plans would not be changing much even though the budgets show

more breathing room, since oil will not help all that much with big

ticket purchases compared to monthly needs. Here we find major purchase

plans fell over the next 12 months to -70 from -67 in July and stand in

the bottom 10 percentile of their range since Dec 1998. This helps to

point the finger for improvement at lower oil and at the same time

raises a cautionary note about getting too hopeful on the notion that

Italy has reached a turning point.

On balance the shifts in the ISAE survey of consumer

confidence are consistent with the notion that dropping energy prices

may be the catalyst for improved sentiment. The house hold budget feels

some relief and that improves the overall situation somewhat, but the

unemployment expectations and purchase plans are hardly affected.

Europe is still caught in the grip of a slowdown. And, lower

energy prices could help to temporarily mollify consumers. Still, Italy

has been weak for some time. It has no special remedy in place to boost

its economy. Meanwhile, as surrounding nations are getting weaker,

Italy is increasingly challenged. This situation promises to make

Italian consumers worse off before they become better off. This month’s

improvement does not seem to be part of a trend as much as it reflects

a one-off reaction to cheaper oil.

Still Italy’s result suggests we may see more widespread

improvement throughout the Euro Area this month.

Oil prices have a more limited impact to improve sentiment in

Europe given high energy taxes. Compared to the US where at-the-pump

fuel prices will move more when world spot oil prices change, energy

shifts can be expected to boost sentiment less in Europe. So whatever

improvement in sentiment we might see this month in Europe, we should

not expect the improvement to be too dramatic and perhaps not even

lasting as deteriorating economic circumstances eventually catch up

with euro-consumers.

| Italy ISAE Consumer Confidence | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Since December 1998 | ||||||||||

| Aug 08 |

Jul 08 |

Jun 08 |

May 08 |

%tile | Rank | Max | Min | Range | Mean | |

| Consumer Confidence | 99.5 | 95.8 | 99.9 | 103.1 | 11.9 | 112 | 127 | 96 | 31 | 111 |

| Last 12 months | ||||||||||

| OVERALL SITUATION | -79 | -84 | -82 | -81 | 9.5 | 109 | -22 | -85 | 63 | -56 |

| PRICE TRENDS | -11.5 | -16 | -11 | -15 | 57.7 | 55 | 4 | -32 | 36 | -14 |

| Next 12months | ||||||||||

| OVERALL SITUATION | -30 | -35 | -16 | -9 | 14.3 | 107 | 24 | -39 | 63 | -13 |

| PRICE TRENDS | 23 | 23.5 | 19.5 | 19 | 46.9 | 52 | 49 | 0 | 49 | 22 |

| UNEMPLOYMENT | 7 | 8 | -5 | -3 | 94.9 | 4 | 9 | -30 | 39 | -5 |

| HOUSEHOLD BUDGET | 2 | -7 | -1 | -3 | 22.5 | 107 | 33 | -7 | 40 | 14 |

| HOUSEHOLD FIN SITUATION | ||||||||||

| Last 12 months | -50 | -56 | -55 | -53 | 12.2 | 111 | -7 | -56 | 49 | -30 |

| Next12 months | -19 | -20 | -15 | -10 | 2.9 | 116 | 14 | -20 | 34 | -2 |

| HOUSEHOLD SAVINGS | ||||||||||

| Current | 73 | 75 | 73 | 68 | 96.4 | 2 | 75 | 20 | 55 | 40 |

| Future | -41 | -44 | -38 | -38 | 17.9 | 112 | -9 | -48 | 39 | -24 |

| MAJOR Purchases | ||||||||||

| Current | -55 | -56 | -64 | -51 | 18.4 | 112 | -15 | -64 | 49 | -40 |

| Future | -70 | -67 | -69 | -56 | 9.7 | 104 | -42 | -73 | 31 | -62 |

| Total number of months: | 117 | |||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief