Global| Jan 22 2014

Global| Jan 22 2014Italian Trade Improves...the Hard Way

Summary

Italy's trade surplus grew in November to ?3.8 billion from ?3.7 billion in October. The growing surplus- on the face of it- seems to be evidence that Italy's economy is growing and its competitiveness is improving. However, there is [...]

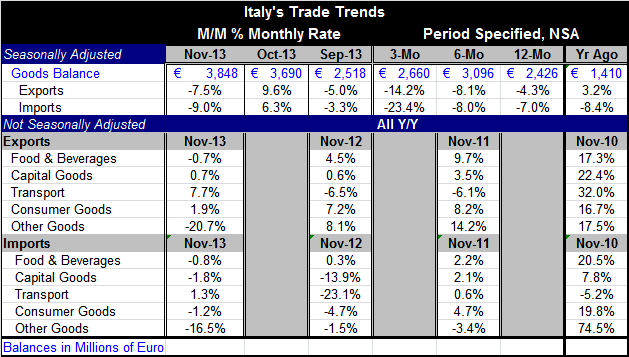

Italy's trade surplus grew in November to ?3.8 billion from ?3.7 billion in October. The growing surplus- on the face of it- seems to be evidence that Italy's economy is growing and its competitiveness is improving. However, there is a problem in making assessments about an economy's fortunes by looking at its trade or current account position.

Italy's trade surplus grew in November to ?3.8 billion from ?3.7 billion in October. The growing surplus- on the face of it- seems to be evidence that Italy's economy is growing and its competitiveness is improving. However, there is a problem in making assessments about an economy's fortunes by looking at its trade or current account position.

Over the past year Italy's exports in fact have fallen by 4.3%. The rate of drop is accelerating as the pace is 8.1% at an annual rate over six months and 14.2% at an annual rate over three months. There is a perception that world trade is improving and growth in Europe is improving. But Italy's exports are dropping at an ever faster pace. That is not a good sign and certainly is no barometer improved competitiveness.

The reason that the trade surplus grew in the face of such export trends is that Italy's imports were even weaker. Italy, basically, is starving itself to import improvement. Year-over-year Italy's imports are down by 7%; over six months they are down at an 8% annual rate. Over three months Italy's imports are dropping at a 23.4% annual rate, much faster than the rate of decline for exports; thus, explaining why Italy's trade surplus is improving.

What we would like to see as evidence of health is a country growing its imports in line with its GDP growth, and with its exports growing slightly faster in order to diminish the deficit or improve a surplus. We would construe such developments as part of a healthy economy. While Italy does have the trapping of an improving surplus, it is achieving that goal all the wrong way.

Exports are rising over the past year for consumer goods, transportation goods, and capital goods. Exports are falling for foods and beverages and falling rapidly for other goods.

Italy's imports are dropping across the board with one exception which is transportation equipment. There, the increase is only 1.3% year-over-year.

The detailed data on exports and imports do suggest the export problem is not as widespread as the import problem since three of the export categories are showing increases; that is somewhat encouraging, although only transportation equipment is showing a strong increase. On the other hand, the import side shows weakness across the board excepting only transportation, a clear signal that domestic demand is indeed weak.

In order for Europe to improve and get on the growth path, it needs for its large economies to begin to perform. While Germany is doing well and Spain, the fourth-largest economy, shows signs of recovering from its deep recession, France is floundering and Italy is still struggling.

What this means is that the prospects for the European Monetary Union to do better may still be there, but no one should be looking for a fast turnaround. Italy shows that its domestic demand is still extremely weak and its competitiveness is still questionable. While Germany remains the strong economy of Europe, it is also an economy geared to succeed with export led-growth, something that does not really help the other economies of Europe. When it comes to European recovery, be careful what you look for.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.