Global| Jul 09 2019

Global| Jul 09 2019Italian Retail Sales Sink; Can Italy Sink Solo or Is It a Broader Symptom of Things to Come?

Summary

Italy continues to show wear and tear although the recent good news was that the EU Commission had decided not to impose sanctions on Italy for an excessive budget deficit. With that concern out of the way, Italy still may be facing a [...]

Italy continues to show wear and tear although the recent good news was that the EU Commission had decided not to impose sanctions on Italy for an excessive budget deficit. With that concern out of the way, Italy still may be facing a demand for some sort of tax hike down the road depending on how this year's budget works out. In the meantime, Italy continues to have quarrels with ships trying to enter Italian waters and off-load migrants rescued at sea. Italy has made it clear that it has absorbed all it will take of them 'basta!'

Italy continues to show wear and tear although the recent good news was that the EU Commission had decided not to impose sanctions on Italy for an excessive budget deficit. With that concern out of the way, Italy still may be facing a demand for some sort of tax hike down the road depending on how this year's budget works out. In the meantime, Italy continues to have quarrels with ships trying to enter Italian waters and off-load migrants rescued at sea. Italy has made it clear that it has absorbed all it will take of them 'basta!'

Retail sales and more show weakness

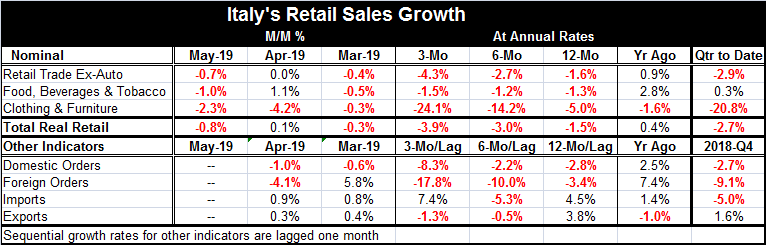

Italy's data table is populated with 'red ink.' I have used bold red figures to identify declines in sales and in other indicators. Retail sales show all retail metrics in the table including real retail sales are declining on all sequential growth calculations. The two orders series show nothing but declines while exports and imports show somewhat more forgiving figures albeit with exports seeming to lose their grip on growth in the more recent, shorter, periods. In short, the assessment of Italian growth and retail sales is poor.

Risks

If Italy does succumb to an economic decline that will constrict tax revenues and increase public outlays, it will blow its budget up into a much larger problem. As it is Italian GDP still has not recovered from the Great Recession and the imposed austerity of that period as Italy's GDP in real terms still lies below its pre-recession level. If Italy were to fall into a recession and bust the budget, it is still hard to imagine that after that with an economy seeking expansion the EU would cause Italy to adopt immediate tax hikes or any form of austerity.

Retailing trends

Regardless of the risk Italy's retail sales and other indicators do not paint a cheerful picture of the future. Italian retail sales in real terms are down in two of three of the most recent months with the one gain in April at 0.1%, hardly anything at all. In real terms, Italian retail sales fall by 1.5% over 12 months, at a 3% pace over six months and at a 3.9% annualized rate over three months. Retail sales are contracting at an accelerating pace. Contraction is also in gear for the other components of retailing as well with a slight exception for food and beverages. Clothing and furniture in nominal terms are falling by 5% over 12 months and dropping at a 24.1% annual rate over three months. That is very disturbing and extreme weakness.

Beyond retailing

Industrial orders also show declines across all horizons and for the most part also sequential weakness. Domestic orders do fall more slowly over six months than over 12 months. But over three months the domestic orders decline pace shoots up to -8.3%, far beyond a -2.8% pace over 12-months. Foreign orders are simply imploding, dropping by 3.4% over 12 months, at a -10% pace over six months and at a -17.8% pace over three months. Exports swing from growth of 3.8% over 12 months to a 0.5% drop over six months to an annualized drop of -1.3% over three months. Imports, that tend to be more closely tied to domestic demand, show some resilience as they slow and decline from 12-months to six-months then reverse out the weakness to post an annual rate gain at a 7.4% annualized pace over three months.

Quarter-to-date trends

The quarter-to-date period has two of three months of hard data for retail sales; that shows a 2.7% annual rate of decline for real sales, a 20.8% rate of decline for nominal clothing & furniture sales, and a very small annual rate increase at just a 0.3% pace for food and beverages in nominal terms. The industrial data show a quarter-to-date growth rate for only one month of the quarter and there are sizeable declines on that basis for orders, foreign orders and imports with exports defying the gravity of the situation with a 1.6% annual rate gain.

Other metrics for Italy

Italy is fighting to keep migrants out and fighting the ECB over the state of its indebtedness. At the same time, it is fighting to keep its head above water. In addition to all the weakness chronicled here, industrial output is down in four of the last five months. On the bright side, employment and the labor force is still growing and the Italian unemployment rate has been holding near its expansion period lows. However, business sentiment has been falling and motor vehicle registrations are declining (y/y) in seven of the last nine months. Inflation in Italy is among the lowest among the original EMU members. Italy does not have an inflation problem. But it does have a growth problem and that will bring with it a clash with the EU eventually since weak growth will cause the state of indebtedness in Italy to rise.

Global constraints

What we are going to start to see is evidence of how difficult policy making has become. Interest rates in Europe really have no place to go. Mario Draghi or Christine Lagarde can say 'whatever it takes… again' but when you drop the hammer on an empty cylinder nothing happens.

• Maastricht rules take fiscal stimulus off the table for most of Europe.

• China has already run its debt up trying to preserve growth in the face of export-slowing tariffs from the United States.

• Japan has its own mountain of debt and low rates –negative rates- to boot.

While I would not say that the U.S. is in the cat-bird's seat, it has the most flexibility for policy and an economy that has been outlandishly resilient even if it has not grown strongly.

A geopolitical sea of risk

Geopolitical threats of a significant nature abound. And old post war relationships are being strained by a new view everyone should carry their own weight in arrangements like NATO.

• Turkey is buying arms from the Russian...

• ...and Turkey drilling in a disputed sea to the ire of the EU and Cyprus.

• Thin-skinned Donald Trump is in a snit with the U.K. over a leaked memo that was critical of him.

• South Korea and Japan are eyeball to eyeball over an old wartime tiff that just won't go away.

• Europe and the U.S. are at odds on how to deal with Iran a country that is going rogue on its promise to restrain its nuclear ambitions. Iran's actions are getting blow back from the UN, the EU and the U.S. instead of gaining it bargaining power. It is hard to tell if something is about to blow up (literally) or not.

While the global economy has been 'in a good place' for a good long while, the TV show by that same name reminds us that the Good Place can turn on a dime and suddenly become a not-so-good-place or worse. There is not a whole lot more that can go right and help compared to the things that could go wrong and do harm. There are things that could go-right and keep things the same… Stay informed and nimble.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief