Global| Dec 22 2016

Global| Dec 22 2016Italian Retail Sales Rebound

Summary

Italian retail sales are up sharply in October after falling for three consecutive months. The month's gain is large enough that the three-month annualized growth rate is now accelerating from 12-month to six-month to three-month. [...]

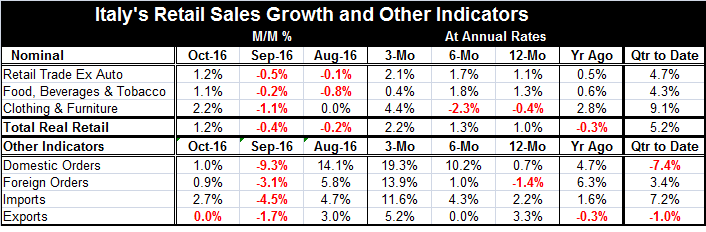

Italian retail sales are up sharply in October after falling for three consecutive months. The month's gain is large enough that the three-month annualized growth rate is now accelerating from 12-month to six-month to three-month. Real retail sales are accelerating as well on that same timeline. In the quarter-to-date, Italian retail sales are rising at a 4.7% annual rate and at 5.2% annual rate, the later growth rate is for sales expressed in real terms. Even as consumer attitudes erode, consumer spending in Italy is ramping up.

Italian retail sales are up sharply in October after falling for three consecutive months. The month's gain is large enough that the three-month annualized growth rate is now accelerating from 12-month to six-month to three-month. Real retail sales are accelerating as well on that same timeline. In the quarter-to-date, Italian retail sales are rising at a 4.7% annual rate and at 5.2% annual rate, the later growth rate is for sales expressed in real terms. Even as consumer attitudes erode, consumer spending in Italy is ramping up.

No Renaissance but Italian trends turn up

Several other Italian indicators also point to some Italian revival. Italian domestic orders, foreign orders and imports all show substantial and impressive growth rates over three months as part of an ongoing acceleration for each of these flows. Rising imports suggest rising domestic demand in Italy which also suggest better growth. Rising domestic orders suggest expanding domestic business, particularly on the output side. Rising foreign orders suggest that domestic output is getting stimulus from either improved Italian competitiveness (the euro has been weak) or from a pickup in demand elsewhere in the world (or both). Italian exports are up at a 5.5% annualized pace over three months and by 3.3% pace over 12 months but also register a slowing from those growth rates over six months, a timeframe when exports go flat. However, the rise in export orders suggests that Italian exports will be picking up.

Trends turn up but Q4 results are still touch-and-go

Still, these indicators have been quite volatile and in the quarter-to-date (Q4), despite the impressive recent trends, domestic orders are falling very sharply compared to their Q3 pace. Exports are falling early in Q4 as well, but foreign orders and imports have growth rates that range from solid to impressive in Q4.

Italian banking and political instability meet a stern test

Right now all eyes are on Italy for its banking issues and its recent political instability. Bank Monte dei Paschi is not having success raising private funds and it is expected that the Italian government will arrange a 'bailout' for it. Yet, bank bailouts are prohibited under new banking rules adopted in the EU at the time of the Cyprus banking crisis. It is not clear at all how Italy is going to be able to engineer a bank bailout and still be compliant with respect to the EUs rules. Everyone expects some sort of state-aided help and no one has explained how it can be done legally in the existing EU framework. Would a bailout by any other name stink as badly in Brussels? We may find out.

Growth spreads- and with it hope and even risk

Add Italy's name to the list of countries that are showing some upside. Germany is still doing well. France is weak but has shown some upward momentum (see yesterday's report). The U.K. has a good report out from the Confederation of British industry today for the fourth quarter as well as a new reading for December consumer confidence from GfK that shows a slight uptick in consumer attitudes. In addition, commercial vehicle sales for Europe grew 13.2% annually to 203,799 units in November. After a good long spell of very disappointing economic statistics in both Europe and the U.S., there are some upbeat signs, less than stellar signs in many cases, but still upbeat signs are starting to proliferate in Europe. The U.S. has its own revival that seems to be in progress aided by a solid Q3 GDP report - for now the Atlanta Fed 'nowcast' is hovering only at 2.6% for Q4. The U.S. economy seems more solid but is not running away with strength. A growing uptrend in durable goods orders in the U.S. also was reported today adding to the sense of ongoing upswing. These sorts of things can feed on each other, causing growth to become more solid and to accelerate. It is a fortuitous blend of events with the Trump elections serving to inspire economic confidence for change in the U.S. as growth in Europe seeming to have found a toe hold, too. Asia is still sort of lost in the woods. Still, some degree of optimism is warranted. How much is still hard to tell. And how dependent it is on accommodative monetary policy is even harder to tell. If firmer growth does take root, it will be important to watch the speed with which monetary authorities act to reduce their accommodation as well as how quickly markets react to the combination of growth and of less central bank backing. At that time it will be important to keep a finger on the pulse of the economy to see if it is maintaining a strong pulse.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief