Global| Jan 24 2014

Global| Jan 24 2014Italian Retail Sales Offer Very Slow Progress

Summary

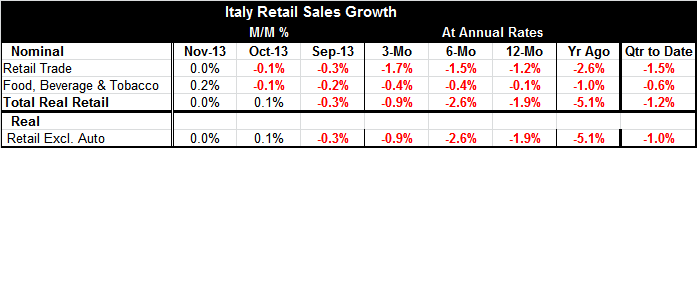

Retail sales for Italy in November were flat, marking their best performance since August when sales also were flat. The last increase in Italian retail sales came in May 2013 with a 0.1% rise. Despite the fact that there was a better [...]

Retail sales for Italy in November were flat, marking their best performance since August when sales also were flat. The last increase in Italian retail sales came in May 2013 with a 0.1% rise. Despite the fact that there was a better number November, the best performance for retail sales in number of months, there will clearly be no cheering in the streets about this result. Retail sales dropped by 1.2% over 12 months, they fell at a 1.5% annual rate over six months and they fell at an even faster, 1.7% rate, over three months. The intra-yearly sequential growth rates paint a picture of weakening nominal sales.

Fortunately, if we look at a time series of year-over-year growth rates, we see a more progressive trend. On that basis, Italian nominal retail sales are still declining, but they are cutting the rate of decline year-over-year. We see that in the chart on the left. We also see that there has been some improvement in Italian consumer confidence and that retail sales in a very general sense tend to follow the shifts in consumer sentiment. As we saw in 2008 and 2009, when consumer sentiment picked up, it may take a little while for consumer spending to pick up, but eventually it does. In that sense the rebounding consumer sentiment is good news even though a large gap has developed between sentiment and consumer spending. That gap under the circumstances is not unusual and, in fact, is quite normal. However, we also must note that consumer confidence, having broadly increased, has also started to lose some of its momentum over the past few months. That may raise some new questions.

Turning to the figures in the table on real retail sales, we also see a slightly more encouraging picture there than from the trends in nominal retail sales. Real retail sales excluding autos are flat in November, but they had risen by 0.1% in October. Retail sales are down by 1.9% over 12 months and they are falling at a faster, 2.6% annual rate, over six months. However, over three months, real retail sales are declining at only a 0.9% annual rate. While that is still a contraction, it is better than the 12-month and six-month growth rates. On balance, retail sales are on a net basis higher over the last two months once inflation-adjusted. Even so that is pretty thin gruel for good news.

If we compare Italian inflation-adjusted retail sales to the same measure for the euro area, we find that there is a reasonably close tracking, with Italian sales consistently lagging behind the performance of sales in the euro zone since 2010. Early in 2013, euro zone sales picked up and then flattened out and, as that happened; Italian sales basically mimicked that pattern from a lower level.

This gives us two optimistic trends to look at for Italian sales. The first is that consumer confidence has risen and sales historically have tended to close the gap on consumer confidence when confidence has moved up sharply as it has. The second is that Italy tends to follow the patterns in the euro zone. It is currently following the euro zone's pattern fairly closely and the euro zone pattern is showing ongoing improvement. Clearly, what happens in Italy is going to depend more about the circumstances within Italy than for the euro zone at large. But Italy is one of the largest euro zone economies; thus, improvement in the euro zone is apt to provide Italy with a better economic environment which will help to aid the performance of retail sales.

Current conditions and performance in Italy are poor; however, there is evidence that confidence and retail sales may be on the mend. The euro zone shows various signs of being on the mend as well, although we have to be careful about that since Germany bears such a large weight in the euro zone and has an economy that does not necessarily spinoff a proliferation of positive effects the boost growth for fellow EMU nations. Still, there is reason for optimism. Despite the sluggishness in Italian retail sales, on balance, they show signs of improving and there are reasons to believe those signs.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.