Global| Oct 20 2014

Global| Oct 20 2014Italian Orders Rebound but Go Nowhere

Summary

Italian industrial orders in August rose by 1.5% after a 1.5% decline in July. Foreign orders rebounded by 2.5% after a 2.1% decrease in July. Domestic orders rose by 0.7% after a 0.9% decline in July. The message here is that there [...]

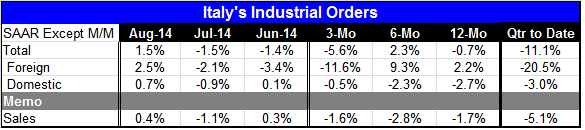

Italian industrial orders in August rose by 1.5% after a 1.5% decline in July. Foreign orders rebounded by 2.5% after a 2.1% decrease in July. Domestic orders rose by 0.7% after a 0.9% decline in July. The message here is that there wasn't much change in activity during this period. And we can see from the sequential growth rates that the path of Italian industrial orders remains weak.

Italian industrial orders in August rose by 1.5% after a 1.5% decline in July. Foreign orders rebounded by 2.5% after a 2.1% decrease in July. Domestic orders rose by 0.7% after a 0.9% decline in July. The message here is that there wasn't much change in activity during this period. And we can see from the sequential growth rates that the path of Italian industrial orders remains weak.

Overall Italian industrial orders fell 5.6% at an annual rate over three months after rising at a 2.3% pace over six months but are still falling at a 0.7% annual rate over 12 months. In the quarter to date, a quarter that lacks one month's worth of data to complete the third quarter, orders are falling at an 11.1% annual rate.

Italy's foreign orders are falling at an 11.6% annual rate over three months. This comes after accelerating to a 9.3% annual rate over six months and with a 2.2% gain over 12 months. Despite the climb back, for orders in August, foreign orders are falling at a 20.5% annual rate in the quarter to date.

Italian domestic orders are showing a tendency to mitigate their decline as the negative growth rates for three months, six months and 12 months get progressively smaller. Over three months domestic orders are falling at a 0.5% annual rate, slower than the 2.3% annual rate drop over six months, which is less than the 12-month drop of 2.7%. Still, in the current quarter, domestic orders are falling by 3% at an annual rate.

Italian sales show negative numbers across all the horizons without any clear trend. Sales are falling at a 1.6% annual rate over three months. That's not quite as bad as to 2.8% drop over six months which marked acceleration compared to the 1.7% drop over 12 months. In the quarter to date, Italian sales are falling at an elevated 5.1% annual rate.

Italy continues to struggle. There are still some nascent forces in Italy trying to build momentum for a return to the lira. These are the kinds of things that we saw in the pit of the financial crisis in the euro area. While Italy's situation doesn't have that same degree of difficulty as in the crisis, Italy's economy continues to struggle and to do so after period in which there was substantial dislocation.

Italy, like many countries in the euro area, needs a period of real recovery after the substantial economic dislocation that it lived through. The financial crisis was painful, but in some ways, the recovery is becoming just as painful. It's not that the jobless rate is rising again; it's that those thrown out of work still aren't back. Germany continues to resist any pressure to reflate and instead is pursuing a balanced budget target and urging everyone to follow the pied piper of austerity on the promise that less will be more.

The falling euro exchange rate is some of the medicine that will help Europe. It makes European industry more competitive without any domestic, fiscal or EMU-level action. But it is also a beggar-thy-neighbor program that leans heavily on domestic demand elsewhere to provide fuel for growth. And domestic demand is still in short supply around the world. The U.S., which looked to have the most progressive recovery, saw a collapse in its retail sales in September and that has prompted a stock market selloff in the U.S. as concerns about growth or its speed have been raised.

Italy sits in the middle of Europe's morass. Its domestic orders have been skimming at a pace around zero while foreign orders are in a clear downtrend for year-over-year growth. No county in Europe can use fiscal policy for stimulus. Europe itself is weakening. Monetary policy is probably played out and further monetary maneuvering is opposed by Germany. Meanwhile, the effect of sanctions on Russia spreads. Europe is in an uncontrolled slide and Italy is feeling the pain.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief