Global| Jan 22 2015

Global| Jan 22 2015Italian Orders Drop in November

Summary

Italian industrial orders fell unexpectedly in November even as orders from abroad rose. Italian domestic orders fell sharply by 3.9% in November, overpowering a 2.9% rise in foreign orders to drive the overall orders total lower by [...]

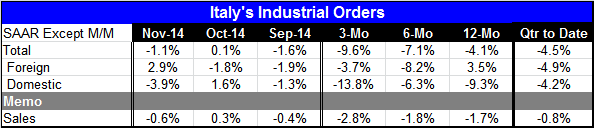

Italian industrial orders fell unexpectedly in November even as orders from abroad rose. Italian domestic orders fell sharply by 3.9% in November, overpowering a 2.9% rise in foreign orders to drive the overall orders total lower by 1.1%.

Italian industrial orders fell unexpectedly in November even as orders from abroad rose. Italian domestic orders fell sharply by 3.9% in November, overpowering a 2.9% rise in foreign orders to drive the overall orders total lower by 1.1%.

Domestic and foreign orders have been slipping since the first half of 2014. Year-over-year growth rates show that they both lost momentum and then turned negative in the second half of the year. Foreign orders fell more decisively while domestic orders shifted out of a growth mode to wallow around flat before taking a sharp turn lower in November.

The sequential growth rates tell the story on the shortened time line of one year and in. Their story is not much different, but perhaps a bit bleaker than the pattern in the chart traced by year-over-year rates of growth. Overall orders are accelerating their decline from 12 months to 6 months to 3 months, falling by 4.1% over long horizon, accelerating their drop to a -7.1% pace over six months and to a torrid -9.6% over three months.

Foreign orders show steady deterioration as they manage to rise 3.5% year-over-year but are falling at an 8.2% pace over six months and at a 3.7% pace over three months.

Domestic orders are weaker but do not give us a clear pattern of deceleration. They are down 9.3% over 12 months then ease back to a -6.3% pace over six months before falling much faster, at a 13.8% pace over three months.

Italian sales decline at a pace of just under 2% over 6 months and 12 months; that steps up to a pace of nearly -3% over three months.

Italian trends are poor with nothing reassuring in their pattern. While some European data seem to have paused their trend to deterioration, Italy is not in that cluster. Spain is holding its unemployment rate high as well with no sign of labor market progress. Meanwhile, the wait is nearly over for the specifics on what the European Central Bank will do. Based on comments from the ECB's Executive Board, it looks to be a less-than-ambitious program. The Germans seem to have been able to influence the program to be something less than the scale adopted in other countries that have employed QE. Given the low interest rates and low bond yields in the euro area, this is probably a healthy development for the ECB. It stands little chance of doing anything but lose money from this operation. The program will not be the solution to Europe's slow growth. Give it six months before Europe starts to look for Plan B.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief