Global| Mar 10 2020

Global| Mar 10 2020Italian IP Has Strong January Rebound...but Don’t Extrapolate It

Summary

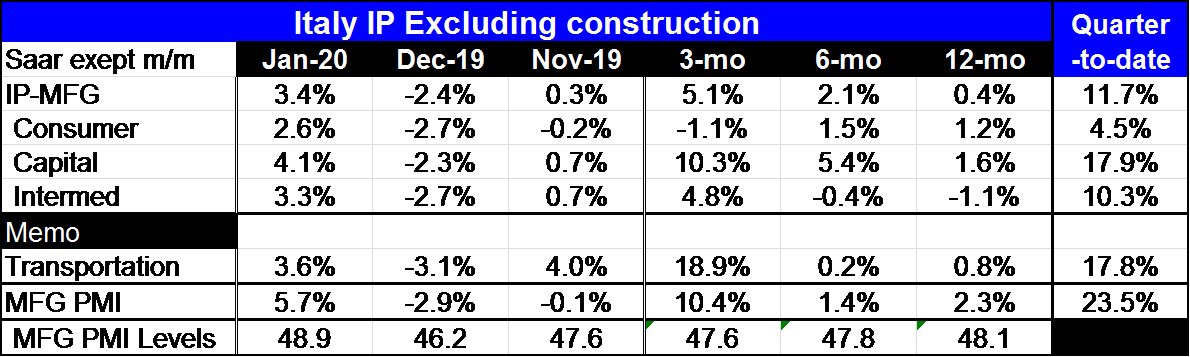

Italian IP rose by a strong 3.4% month-to-month in January after falling by 2.4% in December. December’s losses were across the board, and similarly, January’s gains are also across the board. Despite the late in-the-quarter drop in [...]

Italian IP rose by a strong 3.4% month-to-month in January after falling by 2.4% in December. December’s losses were across the board, and similarly, January’s gains are also across the board. Despite the late in-the-quarter drop in IP in 2019-Q4, production is advancing strongly early in 2020 Q1 with an 11.7% pace of increase for headline IP and similarly solid-to-stronger gains by sector.

Italian IP rose by a strong 3.4% month-to-month in January after falling by 2.4% in December. December’s losses were across the board, and similarly, January’s gains are also across the board. Despite the late in-the-quarter drop in IP in 2019-Q4, production is advancing strongly early in 2020 Q1 with an 11.7% pace of increase for headline IP and similarly solid-to-stronger gains by sector.

Looked at in terms of a sequence of growth rates over 12-months 6-months and 3-months headline IP is clearly accelerating- growing faster over shorter time spans. Acceleration is evident for capital goods output and intermediate goods output but not for consumer goods where output has tailed over the last three-months.

Italian manufacturing output is not stepwise accelerating but it is growing much faster over 3-months than over 12-months and has a very substantial double digit rate of growth for early in Q1. The Manufacturing PMI from Markit shows sequential weakening that is not echoed in the monthly data. The Italian PMI is up strongly more than two points month to month in January compared to December. But things are not looking up for Italy…

Meanwhile back in real-time...

Italy faces a nonetheless grim situation. This report is an example of the economic data lagging enough behind real-world events that they capture a picture through the rear window instead of through the front windscreen. The difference in the two views this month is very marked.

While it is all but impossible to handicap what Italian IP is doing Italian growth is going to be sharply reduced. All movements nationwide have just been restricted in March after a series of previous isolated steps was abandoned as insufficient. At the moment travel is not allowed except by persons with authenticated work-related needs. Italy is urging people to stay home to work or to take leave. The government has suspended mortgage payments during this period to softening the economic blow from the coronavirus.

Pictures taken of famous and well populated Italian tourist spots such as the Spanish steps in Rome and the Trevi fountain show them empty.

Clearly there is going to be a hammer blow to Italian GDP, output, consumer spending and a host of variables. Austria has taken the step of not allowing Italians into the country.

This is also a warning about interpreting economic data. We have already seen in the US a strong February jobs report even as the coronavirus was spreading. Today in the US the NFIB index for February, a sentiment gauge of independently owned businesses, showed a small increase as well. To understand the time of the collapse of confidence and the rise of fear I recommend looking at the disarray in the stock market. The start of the stock market collapse is likely a good estimator of when the public fears began to rise as well.

The coronavirus is a virus that creates flu-like symptoms for most people. As of yet no one under 30 has died from corona. It is most dangerous to people with preexisting illnesses, those taking medicines that compromise their immune systems or to people who are advanced in age. The mortality rate rises sharply for people of age 70 or more. Still, for much of a country’s population it is like a flu but one that is more highly contagious than most flu.

The coronavirus by now has spread widely globally. While governments are taking different approaches, people are getting the idea that this is a very contagious condition and economic activity, even without government restrictions is being reduced globally where the virus is present. Italy is an example of how we may not see the impact of the virus until it suddenly appears in one month with a crushing blow, as it did with the Chinese PMI data. It is somewhat surprising that Italy’s IP rebound in January was so strong. February might even post a decent number. At this point it is very hard to handicap economic numbers that are being scored by the virus. It’s a good idea to take economic data with a grain of or even a full shaker of salt for a while as we sail toward and into the period in which economic activity will be more clearly assaulted.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief