Global| Jun 30 2021

Global| Jun 30 2021Italian Inflation Is More Subdued Than Elsewhere

Summary

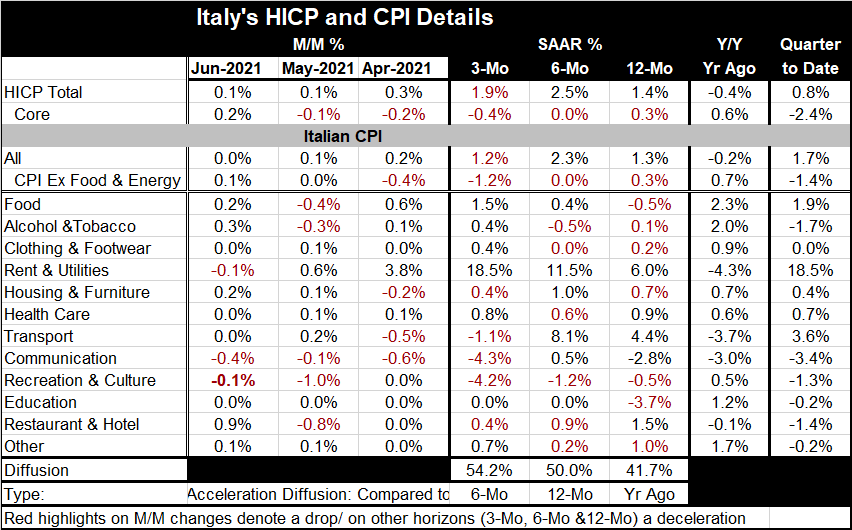

Italian inflation is only at 1.4% (HICP) or 1.3% (domestic index) on a year-on-year basis. Inflation in Germany already is over the top of the pace established as beyond the maximum by the ECB (2%). And while the two Italian headline [...]

Italian inflation is only at 1.4% (HICP) or 1.3% (domestic index) on a year-on-year basis. Inflation in Germany already is over the top of the pace established as beyond the maximum by the ECB (2%). And while the two Italian headline gauges are below the ECB marker, they also fail to show real acceleration. Both gauges accelerate over six months compared to 12 months then both settle to a lower pace over three months compared to six months. Over three months the HICP is closer to running hot at a 1.9% pace, but the domestic CPI has a 1.2% pace over three months.

Italian inflation is only at 1.4% (HICP) or 1.3% (domestic index) on a year-on-year basis. Inflation in Germany already is over the top of the pace established as beyond the maximum by the ECB (2%). And while the two Italian headline gauges are below the ECB marker, they also fail to show real acceleration. Both gauges accelerate over six months compared to 12 months then both settle to a lower pace over three months compared to six months. Over three months the HICP is closer to running hot at a 1.9% pace, but the domestic CPI has a 1.2% pace over three months.

Beyond the headlines, there is the core behavior that shows the trend apart from those elements in the headline that are not present in the core (various food and energy items) inflation in both measures remains tepid. Not only is it tepid but core inflation is decelerating in both core measures in Italy!

Inflation quarter-to-date

With Q3 data in hand, even if only preliminary data, inflation is running at a 0.8% pace (for HICP; or at a 1.7% pace for CPI). But both core measures show prices are declining in Q2 even as Germany is experiencing overheating on its headline over 12 months. Despite that, neither is Germany experiencing high inflation in the headline for Q2 where the headline data are complete as well but still preliminary. The German domestic CPI is also contained for the quarter but with a core closer to the edge at a 1.7% annualized rate. Inflation in Europe has popped but does not seem to be carrying momentum.

Italian inflation

With Italian inflation moderate over 12 months six months, and three months Italian diffusion metrics have also been moderate. Inflation diffusion is at 54.2% over three months, 50.0% over six months and 41.7% over 12 months. On diffusion a 50% reading means there is much inflation acceleration as deceleration across categories. Italy shows diffusion reasonably close to 50% on all horizons but a little more deviation on the low side over 12 months.

Inflation disparities

Inflation disparities

Inflation in the Euro area is not uniform. The German and Italian situations are still hard to pin down. Christine Lagarde has still been focusing on the need to provide the economy assistance and voices trumpeting inflation worry have been stifled. That is different from the U.S., of course, where economic growth is so much stronger with GDP already back to trend and inflation running well over the Fed’s long-term objective and running hot the way the Fed has said it wanted to ‘for a while.’ But for how long will this be acceptable? While the ECB is still focused on delivering stimulus, the Fed in the U.S. is being pushed to begin to withdraw some of its stimulus. These two central banks are singing from very different choir books.

Global differences

Another feature of Italian inflation is that it has not been particularly responsive to the price of oil. Brent prices are up by 109% over 12 months in May. The R-squared relationship between Brent oil and Italian headline inflation is 0.25; for the core it is an even punier 0.09. For Germany, the headline correlation with Brent produces an R-squared of 0.42, but the correlation to the core is much smaller at 0.01. The statistics are just another way of demonstrating how various shocks course though different countries differently- even within Europe and within the EMU area despite all of its homogenization. Right now there is a bit of a policy controversy that centers mostly on the U.S. as central banks are thinking about how much they have done as economies get back on track and as the virus is still being contained for the most part… Policy-makers are beginning to wonder how much is still needed and how much help is ‘too much.’ Europe is a month or two behind the U.S. in facing this quandary and, because it did not throw off so much fiscal stimulus, it will not face the same degree of tradeoff that the U.S. is facing.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief