Global| Mar 16 2020

Global| Mar 16 2020Italian Inflation Gets Even Lower; From 0.4% over 12 Months in January to 0.2% in February

Summary

Italian inflation is low and falling. The HICP was up by 0.4% year-over-year in January to 0.2% over 12 months in February. The month-to-month change in February saw a drop of 0.2% after a flat performance in January. Italy, once one [...]

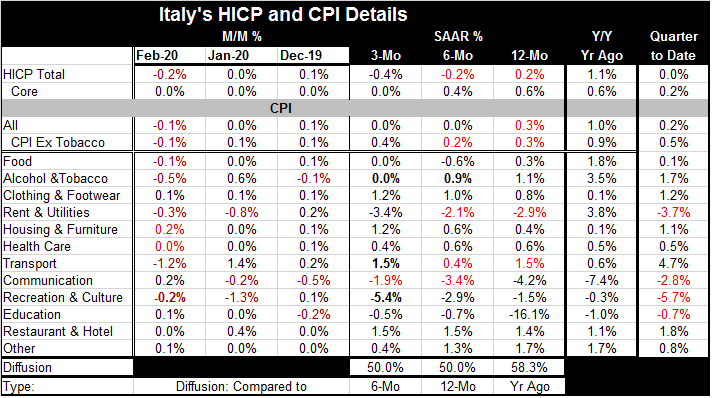

Italian inflation is low and falling. The HICP was up by 0.4% year-over-year in January to 0.2% over 12 months in February. The month-to-month change in February saw a drop of 0.2% after a flat performance in January. Italy, once one of the loose-cannon high-inflation Mediterranean EU/EMU economies has gotten religion even if it is with forced attendance. Quarter-to-date inflation is running at a 0% pace in Italy with the core up at a 0.2% annual rate. Inflation is super contained.

Italian inflation is low and falling. The HICP was up by 0.4% year-over-year in January to 0.2% over 12 months in February. The month-to-month change in February saw a drop of 0.2% after a flat performance in January. Italy, once one of the loose-cannon high-inflation Mediterranean EU/EMU economies has gotten religion even if it is with forced attendance. Quarter-to-date inflation is running at a 0% pace in Italy with the core up at a 0.2% annual rate. Inflation is super contained.

Inflation over 12 months is at a 0.2% pace; over six months it is at a -0.2% pace; and over three months it is at a -0.4% pace. Amazingly with inflation at 0.2% over 12 months, it is still decelerating sequentially!! Even core inflation is decelerating from 0.6% over 12 months to 0.4% over six months to 0% over three months.

The CPI for which we have details in the table (below) shows CPI inflation either falling and flat-lining or sequentially falling from 12-months to six-months to three-months. Core inflation on the CPI is also quite low and weak but not quite sequentially decelerating.

The CPI diffusion indexes show a 50% value over three months compared to six months and at 50% for six months compared to 12 months. 50% is the point where accelerating inflation is balanced by decelerating inflation. Italian 12-month inflation compared to year ago inflation shows a diffusion reading of 58%, indicating more categories with inflation rising than falling. But… on that comparison the CPI headline is actually lower from 1.0% a year ago to 0.3% over the past 12 months; and the CPI core is lower to 0.3% from 0.9% a year ago. Categories accelerating over 12 months compared to 12 months earlier are Clothing & footwear prices, Housing & furniture, Heath care, Recreation & culture (a smaller drop) and ‘Other.’ However, a simple perusal of the tables shows how weak prices are and how widespread the weakness is.

Of course, Italy’s coronavirus problems feed into this. Next month the impact will be greater. There will be plus and minus effects on prices as some goods in short supply might see price pressures, but the overall reduction in activity ought to dominate and make prices even weaker. In the quarter to date (QTD), four categories are seeing prices declining and that is with food prices barely rising at a 0.1% annualized rate (QTD).

Look at how consistently low three-month annualized inflation has been in Italy!

Italy has still not gotten the yearly generation of real GDP back to where it was over a decade ago. And over the last two years, the climb back in trend GDP growth has seen a set-back as GDP has been flat-lining at a significantly depressed level. And now there is the coronavirus impact.

Italy really is suffering. Its inflation rate is low, but its debt-to-GDP ratio remains extremely high. Still, it needs to take steps to support GDP at a time that the coronavirus is a real threat to not just growth but to status-quo income generation.

The EMU-wide Schengen system has come under pressure with Germany closing borders and placing some strict limits on exports of protective equipment outside EU. This underscores that other countries are running Me-first policies. It was popular to bash Donald Trump and his America-first policy and tariffs, but the rest of the world has run this way for quite some time. Now with Germany shutting its borders, I guess the Schengen has become shun-gen.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief