Global| Sep 14 2015

Global| Sep 14 2015Italian HICP Ticks Higher in August

Summary

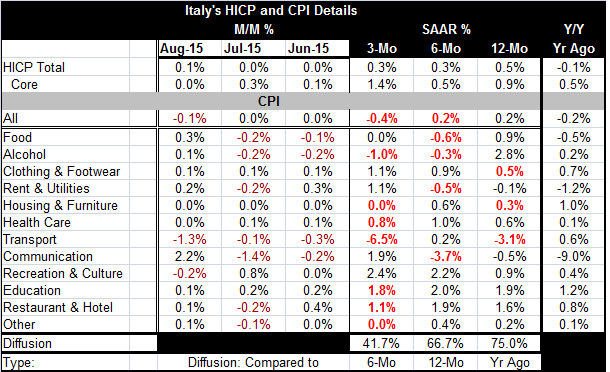

Consumer prices in Italy are very well-behaved. The HICP headline rose by 0.1% in August as the core was flat. The domestic CPI fell by 0.1% in August. Italy's 12-month inflation is 0.5%; the core measure is up by 0.9%; the domestic [...]

Consumer prices in Italy are very well-behaved. The HICP headline rose by 0.1% in August as the core was flat. The domestic CPI fell by 0.1% in August. Italy's 12-month inflation is 0.5%; the core measure is up by 0.9%; the domestic CPI is up by 0.2%. The chart shows that the HICP is accelerating broadly faster than the domestic headline measure. But both measures show higher inflation than over the past two years when all the CPI inflation gauges hugged zero.

Consumer prices in Italy are very well-behaved. The HICP headline rose by 0.1% in August as the core was flat. The domestic CPI fell by 0.1% in August. Italy's 12-month inflation is 0.5%; the core measure is up by 0.9%; the domestic CPI is up by 0.2%. The chart shows that the HICP is accelerating broadly faster than the domestic headline measure. But both measures show higher inflation than over the past two years when all the CPI inflation gauges hugged zero.

Still, the ECB has warned that EMU-wide inflation could see negative numbers again this year.

In August, despite weak headline and core inflation readings, inflation decelerated compared to July in only three of 12 categories. In July inflation had decelerated in seven of 12 categories. Over three months, inflation is decelerating compared to over six months in seven categories; that creates a diffusion reading of 41.7. Diffusion readings below 50 denote more decelerating prices than accelerating prices. The six-month diffusion reading is at 66.7, showing that over six-month compared to 12 months inflation in Italy has been accelerating. And comparing inflation of 12 months to 12 months ago shows another high diffusion reading at 75.0, revealing widespread inflation acceleration. We see that in the chart as inflation is higher than it was 12 months ago, but only by a modest amount.

But diffusion and actual inflation acceleration/deceleration do not always line up. Diffusion is an unweighted process applied across CPI categories while the CPI inflation measure itself is from weighted component data. Diffusion is a double check on whether inflation's change is a widespread phenomenon or not. For example, if a few components with high weights show price pressure that could push the price index headline to acceleration even if acceleration were not the case for most components. When diffusion does not go the same way as the price indices, we have divergent component price movements.

The higher diffusion readings over six months and 12 months confirm that the rise in inflation flagged by the price indices over that period is relatively widespread. However, over three months, we have a new trend and an opposite trend in place. And its metrics are strong with a diffusion value of 41.7. But not all prices indices agree with the diffusion signal.

While diffusion finds price acceleration over six months compare to 12 months, both HICP measures decelerate on that horizon while the domestic index is flat at 0.2% on both horizons. Apparently high weight pries components were weaker than low weight components. Then the diffusion index shows sharp deceleration for inflation over three months compared to six months, but actual headline inflation is flat for the HICP and accelerating sharply for its core. Inflation is negative for the domestic measure, confirming the falling price story. But not all price tends agree. We have mixed readings.

The chart shows us that Italian inflation is world part from its old tendencies. Yet, inflation did spring back as the global financial crisis abated then it moved lower again and continued to move lower or stay low since 2012 as the economic recovery remained weak and as Italy adopted austerity.

Of course, Italy is subject to all the same depressing international inflation forces as any other country. Weak commodity prices, weak oil prices and weak growth abroad all help to temper Italian inflation. Also Italy is minding its budgetary responsibilities within the EMU framework and inflation has been kept low.

Over 12 months, among the major CPI categories, only alcohol has a 12-month rise in prices in excess of 2%. Italy is not building much in the way of inflation pressures. Its sequential inflation rates are moderate although the HICP core rate is up strongly over three months, a period for which the Italian domestic headline shows the opposite, widespread price weakness.

Europe does not have much strength. The global economy is weak. The weak euro may be one avenue for inflation to gain some traction. But oil and other commodity prices will be running counter to that. So far we can say Italy's inflation trends are weak and mixed. As a traditional European high inflation country, Italy's recent prices performance is encouraging.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.