Global| Jun 28 2016

Global| Jun 28 2016Italian Consumer Confidence Makes Clear U-Turn from `New High' to Never Mind

Summary

Make no mistake about it. Italy's drop in consumer confidence is not about Brexit; it's about Italy. Italian confidence had surged, peaking in January of this year and has since been in a steady state of erosion. Confidence is 18 [...]

Make no mistake about it. Italy's drop in consumer confidence is not about Brexit; it's about Italy. Italian confidence had surged, peaking in January of this year and has since been in a steady state of erosion. Confidence is 18 points off its January peak. It is now at its lowest level since August of last year and it has downward momentum.

Make no mistake about it. Italy's drop in consumer confidence is not about Brexit; it's about Italy. Italian confidence had surged, peaking in January of this year and has since been in a steady state of erosion. Confidence is 18 points off its January peak. It is now at its lowest level since August of last year and it has downward momentum.

Many of the same forces at play in the U.K. also are percolating in the Italian economy and in Italian politics where a minority separatist party (Five Star) has got political control in two large Italian cities, Rome and Turin. Italy faces more elections in the month ahead.

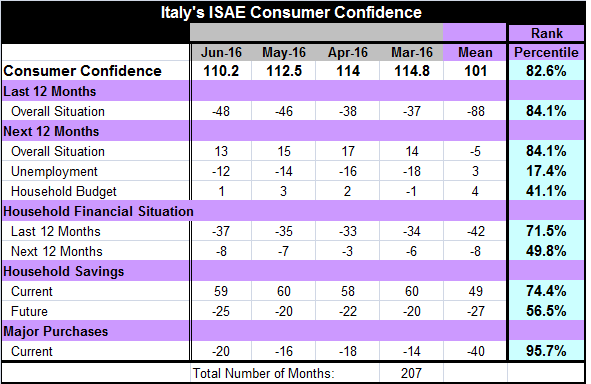

Confidence is still at a high level in Italy, standing in the 82.6 percentile rank of its historic queue of readings. But it has been slipping fast. The five-month drop in Italy's confidence index is the seventh worst seven-month stretch in the history of the series making it an event that has been worse only 2.8% of the time. This setback is severe. In all likelihood, there is more to come because of European financial conditions as well as Italy's own withering economy and percolating political discord. Italy's composite PMI index from Markit has seen a parallel drop to what we see in consumer confidence.

In the confidence report, the overall situation for the past 12-months is rated slightly worse this month but still at an 84th percentile queue standing. For the next 12-months, the overall situation is also downgraded by two points to the same 84th percentile standing. Unemployment fears are slightly higher, but still very much at bay with a rank standing that is lower only 17% of the time. The assessment of the household budget situation is worsened by two points, dropping to a weak 41st percentile standing.

The household financial situation over the last 12-months is rated as having slipped by two points to a 71st percentile standing. Over the next 12-months, expectations have slipped on the month and the outlook is much weaker but near a 50th percentile standing. Similarly, savings currently rate as in their 74th percentile but the future is assessed as much weaker at only the 56th percentile.

The environment for making a major purchase backtracked this month but still has an extremely high 95th percentile standing.

Beyond the confidence report

With the problems related to Brexit, there is a global stock market selloff in train and there is a sharp selloff of bank stocks especially Italian banks. They have not been recapitalized like U.S. and U.K. banks. In Italy, banks are still fundamentally depending on backstopping from the central bank for their support. As these factors play out in markets, confidence is likely to continue to come under continued downward pressure.

Related reports this morning saw France also report a lowering in its consumers' assessment of conditions but with a much smaller decrement compared to Italy. In the wake of the U.K. Brexit vote, the U.K. itself has been downgraded. There is a weaker U.K. retail indicator from the BCI survey for June. The U.K. Chancellor is talking about how tax hikes will be needed. Meanwhile, Spain's retail sales have slowed in May. We will be keeping an eye on the European data much more carefully in the coming months to see what fallout might be in train.

Summit up...

In a summit in Portugal today, ECB President Mario Draghi called for central banks to align their monetary policies to avoid destabilizing spillovers between economies growing at different speeds. It is unclear what Mr. Draghi wants. In some sense, no central bank wants policies from abroad to make its road harder. But does that mean that a country experiencing different conditions from its trade partners should not run the right policy for its position in the business cycle? It is quite unclear what Draghi means, but we can speculate that it simply is a way to urge the Fed to have forbearance after having come so close to pulling the interest rate trigger earlier in the year. But then, there is the issue for the Fed of what negative interest rates in Europe and elsewhere are doing by sending capital flows hurtling into the U.S. market to snap up `high' U.S. treasury yields at a time when the Fed was preparing to push rates higher. The Fed's plan is now undone. Who is right here? Who has the moral (economic?) high ground? At the end of the day, Draghi seems to be complaining about something that is simply part of economic reality.

On balance, there are a lot of reasons to look with a degree of skepticism on the road ahead. Central banks now face even more challenges. In the EMU, fiscal policy is still in a German lock-box. Good luck with that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief