Global| Aug 29 2013

Global| Aug 29 2013Italian Businesses and Consumers Feel Somewhat Better

Summary

Italian business and consumer confidence both improved in August. However, the relative state of the confidence of businesses and consumers is still quite poor. When we take the current month's standing for confidence and place it in [...]

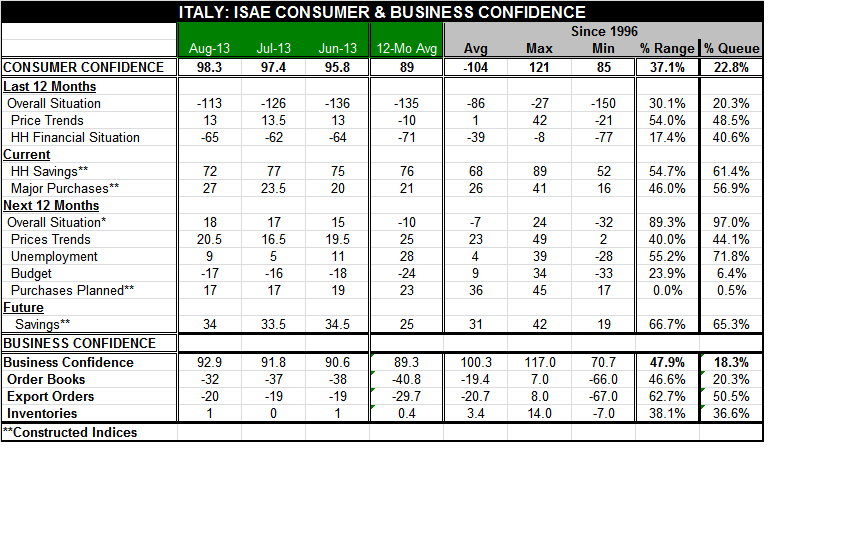

Italian business and consumer confidence both improved in August. However, the relative state of the confidence of businesses and consumers is still quite poor. When we take the current month's standing for confidence and place it in an ordered queue of historic values back to late 1996, we find that consumer confidence is just above the lower 1/5 of this queue while business confidence is just in the top of the lower 1/5 of its queue. That means that each index is LOWER than its current level only about 1/5 of the time; each is better 4/5 of the time. That is impressive weakness.

Italian business and consumer confidence both improved in August. However, the relative state of the confidence of businesses and consumers is still quite poor. When we take the current month's standing for confidence and place it in an ordered queue of historic values back to late 1996, we find that consumer confidence is just above the lower 1/5 of this queue while business confidence is just in the top of the lower 1/5 of its queue. That means that each index is LOWER than its current level only about 1/5 of the time; each is better 4/5 of the time. That is impressive weakness.

In general terms, consumer and business confidence in Italy continues to be very adversely impacted. However when you look at the chart you see that, in fact, consumer confidence has moved up very sharply from an extraordinary low point, thus consumers are feeling substantially better than they did a short (and extended) while ago. Still, measured against the standards of historic averages their level of comfort is still pretty poor. On the other hand, business comfort has only improved slightly and therefore continues to be stuck at roughly the same low point in this range that it has been for some time. , Business confidence had previously made of sharp recovery from its extreme business cycle low in early 2009. Its recovery overshot and fell and now it on the second low point that is still far higher than its first in-financial-crisis low.

The charts basically give you a very good picture of exactly how things have moved around for the tow groups. And while consumer confidence has moved up sharply we would caution that you look at the level of confidence relative to where it's been historically rather than to look at how much it has jumped from its extreme lows where it was stuck for nearly a year.

Having said that it's also true that with the sharp improvement in conditions, consumers are very upbeat about the future. Their +18 diffusion score for the forward-looking overall situation puts it in the top 3% of its historic range - an extremely optimistic view of the overall situation for the next 12 months. That response unfortunately does not fit very well with the outlook for unemployment where the response moved up the +9 in August from +5 and resides in about the 72nd percentile of its historic range- or the top 28%.

Consumer's assessment of the current situation give current metrics a slightly better than middling rating for the ability for households to save and to make major purchases. The queue standing for both of those is above the 50th percentile, for household savings it's just barely above the 60th percentile; for major purchases it's above the 56th percentile. To underscore the point of improvement, looking back at the last 12 months the assessments put the overall situation there in the bottom 1/5 of its historic range. That households are looking for a big improvement in the next 12 months compared to the last 12 months, leaves a lot of room for improvement to occur and still leave the readings low. Significant improvement could happen without conditions getting to be very good.

Business confidence is still very weak in the lower 1/5 of its range. Order books are given a raw diffusion responsive of -32, an improvement from -37 in July but that still sits in the bottom 1/5 of its range. Export orders are somewhat better; still they did slip month-to-month to a raw diffusion reading of -20 from -19 in July. However, that reading is still a 50th percentile reading with respect to its ordered queue standing.

The good news for Italy is that there has been improvement in consumer confidence and in business confidence. However we want to be careful about overstating the degree of improvement. Because Italy is coming off of such extremely poor conditions from the standpoint of consumers they could be looking at a very big improvement in confidence and yet remain in a rather beleaguered state. On the business side of things we see continuing a minor improvement that is still at a very weak level. If business conditions are not going to improve appreciably, it's going to be hard for consumers to feel much improvement in their lot in life, let alone for any real improvement to occur.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.