Global| Dec 29 2009

Global| Dec 29 2009Italian Business Confidence Advances...But Still Lags

Summary

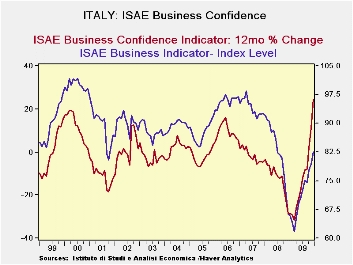

Italian business confidence is shooting up strongly but still clings to relatively weak absolute readings. The level of the current reading stands in the 52nd percentile of the range of values occupied since October of 1996. But by [...]

Italian business confidence is shooting up strongly but still clings to relatively weak absolute readings. The level of the current reading stands in the 52nd percentile of the range of values occupied since October of 1996. But by rank the current index stands 136th out of 159 readings or in the bottom 12 percentile of all readings over that same span. That is not a very reassuring statistic despite the rise in the index this month. This percentile rank-in-queue measure is uniformly weak across the various components this month. Unfortunately inventories have the highest reading within each commodity category. Of all commodity types consumer goods are doing the best while investment goods and intermediates goods are lagging nearly equally.

The graphic below shows the strength of the current surge depicting both the absolute level of the index and its percentage rise on the same graph. We can hope that the rise continues and that it will bolster the level reading further. But for the rest of the e-Zone a good deal of pessimism remains.

France’s final GDP figure confirms the weak rise in GDP in Q3 although it does show two quarterly gains in a row. In the UK private forecasters have reaffirmed their view of slow growth in the UK for the year to come. Italy’s business survey results seem to fit snugly into this grouping of reports that shows some improvement but still no gusto.

Italy ISAE Business Sentiment| Since Oct 1996 | |||||||

| Dec-09 | Nov-09 | Oct-09 | Sep-09 | Percentile | Rank | Rank% | |

| Biz Confidence | 82.6 | 79.4 | 77.8 | 74.6 | 52.0 | 139 | 12.7% |

| TOTAL INDUSTRY | |||||||

| Order books & Demand | |||||||

| Total | -40 | -47 | -50 | -52 | 33.8 | 146 | 8.2% |

| Domestic | -41 | -47 | -49 | -49 | 35.8 | 146 | 8.2% |

| Foreign | -41 | -49 | -54 | -55 | 35.8 | 146 | 8.2% |

| Inventories | -2 | -2 | -3 | 1 | 37.5 | 125 | 21.5% |

| Production | -38 | -45 | -49 | -47 | 28.6 | 147 | 7.6% |

| INTERMEDIATE | |||||||

| Order books & Demand | |||||||

| Total | -52 | -55 | -57 | -55 | 26.8 | 146 | 8.2% |

| Domestic | -53 | -55 | -57 | -54 | 27.4 | 146 | 8.2% |

| Foreign | -49 | -56 | -56 | -59 | 31.6 | 146 | 8.2% |

| Inventories | -4 | -6 | -7 | -1 | 37.9 | 113 | 29.1% |

| Production | -48 | -51 | -52 | -51 | 25.0 | 147 | 7.6% |

| INVESTMENT GOODS | |||||||

| Order books & Demand | |||||||

| Total | -45 | -56 | -62 | -61 | 26.7 | 146 | 8.2% |

| Domestic | -45 | -54 | -54 | -55 | 30.0 | 146 | 8.2% |

| Foreign | -48 | -54 | -66 | -61 | 25.3 | 147 | 7.6% |

| Inventories | -3 | 0 | -1 | -1 | 36.8 | 111 | 30.4% |

| Production | -45 | -52 | -61 | -58 | 21.6 | 147 | 7.6% |

| CONSUMER GOODS | |||||||

| Order books & Demand | |||||||

| Total | -23 | -32 | -36 | -38 | 44.9 | 133 | 16.5% |

| Domestic | -23 | -32 | -36 | -39 | 50.0 | 125 | 21.5% |

| Foreign | -31 | -36 | -41 | -42 | 37.1 | 141 | 11.4% |

| Inventories | -2 | 1 | -1 | 1 | 34.6 | 111 | 30.4% |

| Production | -21 | -33 | -37 | -33 | 43.9 | 137 | 13.9% |

| Total number of months: 159 | |||||||

by Louise Curley December 29, 2009

Reports of

retail trade in Spain, Sweden and Hong Kong were among today's

statistical releases. Retail sales are sometimes good

indicators of trends in total GDP. In order to test this

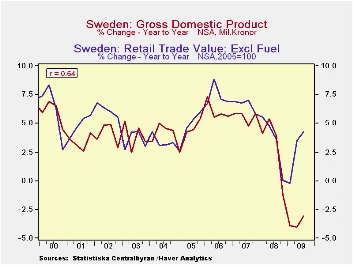

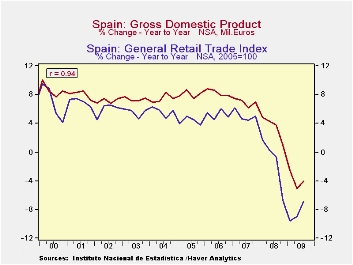

hypothesis, we computed the correlation coefficients between the year

over year percent change in the quarterly values of the value index of

retail sales and the year over year percent change in the value of

total GDP over the past ten years*. The first three charts

show these correlations.

Reports of

retail trade in Spain, Sweden and Hong Kong were among today's

statistical releases. Retail sales are sometimes good

indicators of trends in total GDP. In order to test this

hypothesis, we computed the correlation coefficients between the year

over year percent change in the quarterly values of the value index of

retail sales and the year over year percent change in the value of

total GDP over the past ten years*. The first three charts

show these correlations.

The highest correlation was in Spain where

the correlation coefficient was .94. Hong Kong was next at

.87 and Sweden was the lowest at .64. The correlation

coefficient squared, R2, is a measure of the

explanatory power of one variable on the other when all other factors

are held constant.  Thus, in the case of Spain, based on the

experience of the last ten years, the year to year change in retail

sales explains about 88.4% of the variation in total GDP when all other

factors are held constant. In the case of Hong Kong, the year

to year change retail sales explains 75.7% of the change in total GDP

and in the case of Sweden, only 41%. The precise values are less

important than the order of magnitude. Thus, we should expect

the trend in retail sales in Spain to have a greater impact on the

trend in total GDP than that in Hong Kong or Sweden.

Thus, in the case of Spain, based on the

experience of the last ten years, the year to year change in retail

sales explains about 88.4% of the variation in total GDP when all other

factors are held constant. In the case of Hong Kong, the year

to year change retail sales explains 75.7% of the change in total GDP

and in the case of Sweden, only 41%. The precise values are less

important than the order of magnitude. Thus, we should expect

the trend in retail sales in Spain to have a greater impact on the

trend in total GDP than that in Hong Kong or Sweden.

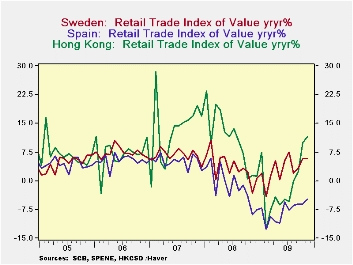

The fourth chart

shows the year over year changes in monthly retail sales in the three

countries. On the basis of the past relationship between

retail sales and total GDP the year to year changes in the value of

retail sales in October and November of 9.9% and 11.7% for Hong Kong

suggest there is a good chance that the year to year change in the

fourth quarter total GDP will increase from -1.99% in the third quarter

to perhaps a positive value. The continued negative, though

diminishing, yearly comparisons of retail sales in Spain suggest that

any improvements in year to year comparison for total GDP in the fourth

quarter is likely to be small.

On the basis of the past relationship between

retail sales and total GDP the year to year changes in the value of

retail sales in October and November of 9.9% and 11.7% for Hong Kong

suggest there is a good chance that the year to year change in the

fourth quarter total GDP will increase from -1.99% in the third quarter

to perhaps a positive value. The continued negative, though

diminishing, yearly comparisons of retail sales in Spain suggest that

any improvements in year to year comparison for total GDP in the fourth

quarter is likely to be small. For Sweden, the year to year

increases in retail sales of 5.8% and 5.7% in October and November may

be large enough to have a positive effect on the increase in total GDP

in spite of the fact that the yearly change in retail sales has less

than a major effect on the change in total GDP. *(Computation of the

correlation coefficient can be done in DLXVG3 by clicking on

"Correlation" in the TOOLS menu.)

For Sweden, the year to year

increases in retail sales of 5.8% and 5.7% in October and November may

be large enough to have a positive effect on the increase in total GDP

in spite of the fact that the yearly change in retail sales has less

than a major effect on the change in total GDP. *(Computation of the

correlation coefficient can be done in DLXVG3 by clicking on

"Correlation" in the TOOLS menu.)

| Retail Sales, Value Indexes Y/Y % Change | Nov 09 | Oct 09 | Sep 09 | Aug 09 | Jul 09 | Jun 09 | May 09 | Apr 09 | Mar 09 |

|---|---|---|---|---|---|---|---|---|---|

| Sweden | 5.74 | 5.80 | 3.38 | 1.80 | 7.51 | 5.16 | 0.32 | 5.21 | 1.26 |

| Spain | -4.99 | -6.03 | -6.08 | -6.51 | -7.75 | -5.54 | -10.91 | -10.57 | -9.30 |

| Hong Kong | 11.66 | 9.87 | 2.57 | -0.07 | -5.29 | -4.71 | -6.20 | -4.30 | -7.76 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief