Global| Feb 10 2017

Global| Feb 10 2017Italian and French IP Trends Still Point Higher

Summary

In December, Italian and French industrial production went their separate ways, one up, the other down. But the sequential annualized growth rates from three-month to six-month to 12-month show output is expanding and accelerating in [...]

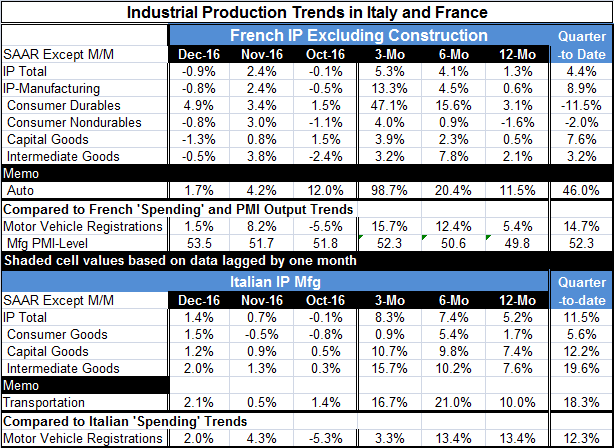

In December, Italian and French industrial production went their separate ways, one up, the other down. But the sequential annualized growth rates from three-month to six-month to 12-month show output is expanding and accelerating in both countries.

In December, Italian and French industrial production went their separate ways, one up, the other down. But the sequential annualized growth rates from three-month to six-month to 12-month show output is expanding and accelerating in both countries.

There is nothing in these production reports to change our view of what the economic realities are in Europe at the moment. Output is expanding and although there is some acceleration at work it is still hard to know how well-entrenched that trend is.

In France, motor vehicle production is strongly accelerating. In Italy, it is not accelerating, but it has ramped up and remains strong. Ongoing motor vehicle registrations are accelerating more strongly in France than in Italy, but registrations in Italy are stronger year-over-year.

France shows acceleration in consumer goods and capital goods. Italy shows acceleration in capital goods and intermediate goods. For France, intermediate goods output has slowed over three months. In Italy, consumer goods output has slowed over three months. Each country has a sector with significantly less strength than the other two.

The quarter-to-date shows strong output gains in both countries. But France shows declines in consumer goods output in Q4 while in Italy all sectors are expanding output in Q4.

For France, output has been more tepid and has only recently moved up to post stronger gains. In Italy, output has been relatively firm and has been showing improved year-on-year gains since about midyear.

Italy and France both fit into this same picture that finds euro area growth improving as the year has progressed. Both economies still have their issues and in France the nation is in the middle of some hotly disputed elections. European output generally appears to have firmed to some degree in recent months. Inflation is rising but much of that is oil. The ECB is holding off on declaring an easing hiatus or policy reversal on its refusal to recognize any true rise in inflation. For now inflation is being attributed to OPEC and its grip on oil prices. But that judgment and circumstance could change. For now there is nothing in these reports to upset the apple cart of the perceived status quo in Europe. But the firmer than growth looks in the euro area, the lower the hurdle becomes on inflation to trigger an ECB policy switch.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief