Global| May 10 2017

Global| May 10 2017Italian and French IP Both Expand in March But Fall in Q1

Summary

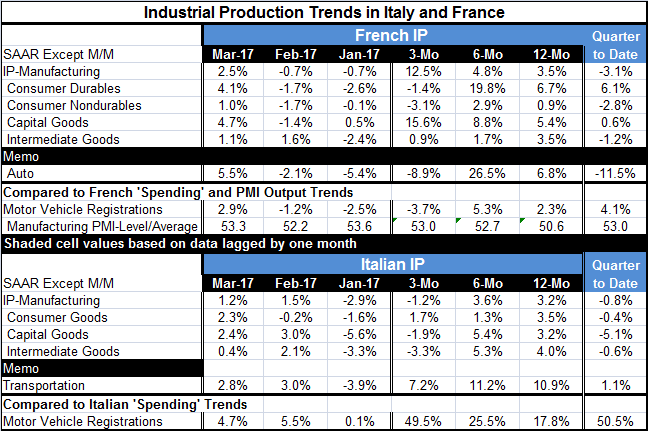

French and Italian IP both rose in March. In France manufacturing IP gained 2.5% and in Italy it rose by 1.2%, both solid to strong gains. In France the rise more than offsets a fall in February. In Italy the gain builds on a rise of [...]

French and Italian IP both rose in March. In France manufacturing IP gained 2.5% and in Italy it rose by 1.2%, both solid to strong gains. In France the rise more than offsets a fall in February. In Italy the gain builds on a rise of similar magnitude in February.

French and Italian IP both rose in March. In France manufacturing IP gained 2.5% and in Italy it rose by 1.2%, both solid to strong gains. In France the rise more than offsets a fall in February. In Italy the gain builds on a rise of similar magnitude in February.

Both France and Italy show IP gains in all sectors in March. For Italy these build on what are mostly sector gains in February while France is rebounding from near across the board drops in February.

French IP patterns

Sequentially French IP growth rates are accelerating. The ramp up from 3.5% over 12 months to a pace of 4.8% over six months to a soaring 12.5% over three months demonstrates that. Yet, the only component for France that shows acceleration is capital goods where the progression is strong. Oddly despite this acceleration, French IP is falling in Q1, dropping at a 3.1% annual rate. This seems a contradiction, but it can happen because the three-month growth rate, which shows accelerating growth for March over December, is quite different from the Q1 rate, which is the annualized Q1 average rise over the Q4 average.

Italian IP patterns

Sequentially Italian IP has no clear trend; growth is solid and accelerates from 12-month to six-month but then growth turns negative over three months. Capital goods and intermediate goods follow that same pattern. For Italy IP also declines in Q1 with a drop logged in all the major sectors as well.

Autos/vehicles

Auto registrations are expanding explosively in Italy over the timeline in the table while for France registration growth hit a snag over the last three months and declined. In France vehicle output has declined over three months as registrations declined. In Italy the output of transportation equipment is strong but has fallen out of double digit growth over three months despite a ramp up in registrations.

Manufacturing IP growth across EMU

On balance, ten EMU members have reported output for March and of these five show output drops and five show output gains. February had produced the same result but for a different batch of countries in each group. Over three months, these EMU members show output declining in five countries and output rising in four with output unchanged in one (Finland). Over six months, only Finland and Ireland show output declines. Over 12 months, output is rising across all thee reporters on gains that range between 1.4% in Germany as the weakest and at 7% in Greece as the strongest, an interesting irony.

Summing up

What this summary tells us is that conditions look very solid if we stick to year-over-year growth rates. But the last two months and three months in particular show a great deal more variation. We have seen that in U.S. data as well as a string of stronger looking data has given way to reports with more give and take in them. While central banks and supra-national agencies have been raising their forecasts, in reality all they have been doing is nudging them carefully higher. There has been no broad-based recalibration and in fact the Fed's more aggressive recent behavior and language may now seem out of step with the uneven data we have seen from the U.S. economy. And with rates rising in the U.S. and Trump's policy objects seeming more elusive, there is less reason that ever to become more upbeat on U.S. growth prospects. Even China has seen some growth softening. It's a good time to temper your enthusiasm.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief