Global| May 08 2014

Global| May 08 2014Is German IP Growth Topping?

Summary

German industrial production surprisingly fell by 0.5% in March. The drop follows a 0.6% gain in February and, while substantial, still allows strong growth in the first quarter. In the just-completed quarter to date, industrial [...]

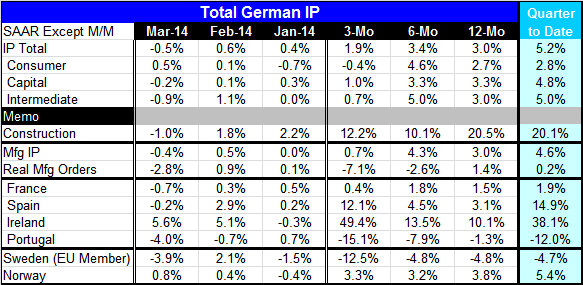

German industrial production surprisingly fell by 0.5% in March. The drop follows a 0.6% gain in February and, while substantial, still allows strong growth in the first quarter. In the just-completed quarter to date, industrial production is rising at a 5.2% annual rate. This is boosted substantially by a 20.1% annual rate gain in construction alone. The consumer sector is lagging with a 2.8% rise. Capital goods post a 4.8% annual rate gain. Intermediate goods post a clean 5% growth rate in the first quarter. However, all the sectors except for consumer goods show declines in production in March. Construction took a substantial 1% backtracking.

German industrial production surprisingly fell by 0.5% in March. The drop follows a 0.6% gain in February and, while substantial, still allows strong growth in the first quarter. In the just-completed quarter to date, industrial production is rising at a 5.2% annual rate. This is boosted substantially by a 20.1% annual rate gain in construction alone. The consumer sector is lagging with a 2.8% rise. Capital goods post a 4.8% annual rate gain. Intermediate goods post a clean 5% growth rate in the first quarter. However, all the sectors except for consumer goods show declines in production in March. Construction took a substantial 1% backtracking.

For manufacturing alone, output fell by 0.4% in March after rising 0.5% in February. Manufacturing output is up but only a 0.7% annual rate over three months. It still logs a 4.6% annual rate of growth in the first quarter. Real manufacturing orders are declining over three months and six months; they fell at a 2.8% annual rate in March. The orders trend seems to be signaling that a slowdown has been in store.

Still, we have strong industrial production across all the major categories in the first quarter and we have reasonable growth rates over three months, six months, and 12 months from the component categories, a hint, at least, of slowdown in each of them.

Other European early reporters of industrial production include France, Spain, Ireland, Portugal, Sweden and Norway. Of these, Sweden and Norway are not members of the single currency union. France, Spain and Portugal each saw declines in industrial production in March. Portugal had two consecutive monthly declines. Among these EMU members, only Portugal has a decline in industrial production over three months; and it's a substantial decline of 15.1% at an annual rate. Portugal also has declines over six months and 12 months. These growth rates indicate progressively deteriorating weakness. On the other hand, both Spain and Ireland show strong growth rates over three months and demonstrate a pattern a progressively stronger growth rates moving from 12 months, to three months, to six months. France's three-month growth rate is only 0.4%, but it's hard to tell what trend may be in the making for France. The recently completed quarter shows Portugal's output falling at a 12% annual rate, France shows an increase at a 2% annual rate, Spain's increase is at a 14.9% annual rate and Ireland's is at a stunning 38.1% annual rate. Three of the four largest countries in the European Monetary Union Germany, France and Spain are showing growth in industrial production in the first quarter.

Sweden and Norway have little in common other than being Scandinavian countries. Sweden is a member of the European Union while Norway is not. Sweden's industrial production fell by 3.9% in March while Norway's rose by 0.8%. Sweden's output is falling at a 12.5% annual rate over three months while Norway's is increasing at a 3.3% pace. Sweden's trend for industrial production is decaying while Norway's seems pretty stable. In the first quarter as a whole, Sweden's industrial production is falling at a 4.7% annual rate while Norway's rising at a 5.4% annual rate.

Europe largely has an upbeat picture with a couple of countries still having their own difficulties. In terms of our sample, the countries having difficulties are Portugal and Sweden. Germany's manufacturing orders have been posting weaker negative growth rates for some time; thus, making the decline in industrial production not exactly a bolt out of the blue. German businesses have been quite heavily and publicly lobbying Angela Merkel to stop ramping up restrictions on Russia. As we suggested in an earlier report, since having seen weakness in orders and now we're seeing weakness in industrial production and hearing complaints from German businesses, maybe where there's smoke there's fire? Maybe their complaints are not simply about the potential for business to be lost but a reflection that businesses is being lost. While Ukraine and Russia are not a huge part of German business, a sudden shutting off of business with these sources could have a noticeable impact on the German economy. And we're wondering if that's what we're seeing now. It's always dangerous to jump to conclusions when we don't have the data to completely support the hypothesis. On the other hand, the timing of the German weakness and the imposition of strictures against Russia are all too closely connected to ignore.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief