Global| Jun 02 2015

Global| Jun 02 2015Is Europe Really Gaining Momentum?

Summary

Through April, PPI prices in the EMU still are falling, but barely so. Monthly trends across member nations are mixed. The HICP, just reported, showed its first gain in six months, rising 0.3% year-over-year. In April, unemployment is [...]

Through April, PPI prices in the EMU still are falling, but barely so. Monthly trends across member nations are mixed. The HICP, just reported, showed its first gain in six months, rising 0.3% year-over-year. In April, unemployment is falling in Germany and Portugal. The signs of an economic spring are in the air. But not all breezes blow fresh.

Through April, PPI prices in the EMU still are falling, but barely so. Monthly trends across member nations are mixed. The HICP, just reported, showed its first gain in six months, rising 0.3% year-over-year. In April, unemployment is falling in Germany and Portugal. The signs of an economic spring are in the air. But not all breezes blow fresh.

European markets were set back today as they pondered whether Greece's comprehensive reform plan would pass muster. But yesterday's PMI data showed that in EMU growth was still mostly headed higher albeit at a slow pace. Some signals remain mixed.

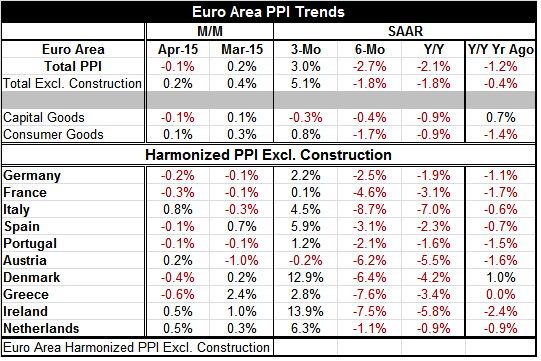

Today's news demonstrates that the pernicious downward pressures on inflation are abating. The trends can be seen in the CPI (HICP) as well as in the PPI. However, the good news is still nascent.

PPI trends across countries show inflation rising over three months for nine of 10 of these EMU nations that are early reporters of the PPI. That is an impressive switch. Over six months and over 12 months, all of these countries show falling rates of inflation. In fact, over six months, inflation is falling faster than it is over 12 months for each of these nations. That is one reason to be cautious about the inflation bounce over the recent three months. Still, there are corroborating trends of rising inflation from the EMU HICP in May.

The EMU manufacturing sector has been slower to recover than has its services sector. We have seen that in the sectoral PMI data. The new reports from Markit in May underline the difficulty that manufacturing is having. Since goods are more tradable than services, what we have is evidence of home grown recoveries taking hold that are not being supported well by the tradable goods sector (manufacturing). We see manufacturing still struggling in economics as diverse as the United States and China. The lack of demand and growth globally is the problem. It weighs on manufacturing sectors everywhere. Services sector expansion is not a cure-all elixir. Services sectors tend to be slower-growing, having lower productivity and generally lower wages. But right now services are the back bone of the European recovery and there is enough push there to help move consumer prices up to show year-over-year gains.

Inflation is neither necessary nor sufficient for an economy to develop growth. However, as a practical matter in the real world, weak inflation (especially falling prices) is taken as a sign of weak demand and therefore perceived to be undercutting growth. Perhaps if productivity were higher, central banks would not be so worried about weak prices. But in an environment where productivity growth is weak and falling commodity prices have helped to tank overall inflation, there is some concern that weak prices may have become a problem in and of themselves.

In this environment, seeing the HICP turn the corner to show a year-over-year price gain is good news. The trend to stronger PPI prices is reinforcing. The European activity data have not come on stream as strongly yet to underpin hopes of recovery. But activity still seems to have upward momentum; it's just weak momentum. For the moment, Europe seems to have everything moving in the right direction...just not quite fast enough. Could this be the start of a real lasting stronger European recovery? Has the ECB's QE program pulled Europe up over the edge?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief