Global| May 08 2008

Global| May 08 2008IP Trends in Germany Begin to Decay

Summary

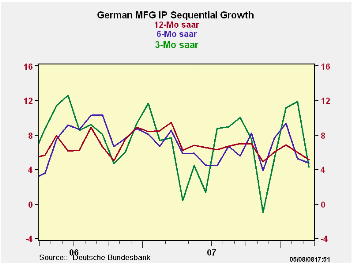

The chart on top shows that German growth trends are decaying across the array of 3-Mo 6-Mo and 12-Mo rates. They are stratified so that the they do point to some further decelerations but only barely. Each growth rate series has a [...]

The chart on top shows that German growth trends are decaying across the array of 3-Mo 6-Mo and 12-Mo rates. They are stratified so that the they do point to some further decelerations but only barely. Each growth rate series has a declining profile coming into the current month. Even so on each horizon the rate of growth is still close to 4.0%, which for real output is still a fairly strong result.

Underneath the headlines we find that the trends and underpinnings are notas bullet-proof. The trend for the output of consumer goods is withering steadily with a three-month rate of growth that is -1.1%. Capital goods output trends are accelerated with a 3-month growth rate 0f 7.5%. But intermediate goods growth has been decelerating steadily. The capital goods result, while quite solid-looking on its own should be looked upon with some suspicion since the rate of the E-zone is slowing and capital goods investment generally gets cut back in economic slowdowns. Clearly German IP trends tell us that the consumer that Germany sells to are being less than resilient.

Short term, however, trends are still quite bright. In 2008-Q1 all main (annualized) sector growth rates are at 3% or higher. Moreover the quarter shows growth accelerations from the previous quarter for output in consumer goods, capital goods and intermediate goods. Growth rates per se are strong in the quarter: For capital goods the q/q annualized rate of growth is 11.7% and for intermediate goods it is 9.2%. These figures exceed their current trend values and imply that Q1 GDP might overstate the developing trend.

Construction is up at a 49% pace in the quarter MFG IP is up at a 9% pace but MFG orders are falling by 5.3%, one of the ominous signals for growth ahead – but ahead of 2008Q1.

| Total German IP | |||||||

|---|---|---|---|---|---|---|---|

| Saar exept m/m | Mar-08 | Feb-08 | Jan-08 | 3-mo | 6-mo | 12-mo | Quarter-to-Date |

| IP total | -0.5% | 0.2% | 1.4% | 4.4% | 4.1% | 4.6% | 9.6% |

| Consumer goods | 0.5% | -0.8% | 0.0% | -1.1% | -1.3% | 0.5% | 3.0% |

| Capital goods | -1.8% | -0.7% | 4.5% | 7.5% | 5.9% | 6.4% | 11.7% |

| Intermediate goods | 1.1% | 1.2% | -1.3% | 3.8% | 6.4% | 6.3% | 9.2% |

| Memo | |||||||

| Construction | -12.3% | 3.1% | 11.4% | 2.9% | 2.4% | -4.0% | 49.1% |

| MFG IP | -0.2% | 0.0% | 1.2% | 4.2% | 4.8% | 5.2% | 9.0% |

| MFG Orders | -0.6% | -0.6% | -0.7% | -7.2% | 6.0% | 5.1% | -5.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief