Global| Sep 16 2009

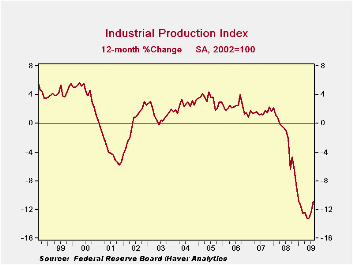

Global| Sep 16 2009IP Trend Turns Higher

Summary

Output and capacity: IP rose by 0.8% in August and manufacturing capacity rose for the second month in a row. For MFG, utilized capacity is just at 66.6% barely two thirds of the capacity put in place. However, even going back to the [...]

Output and capacity: IP rose by 0.8% in August and

manufacturing capacity rose for the second month in a row. For MFG,

utilized capacity is just at 66.6% barely two thirds of the capacity

put in place. However, even going back to the overheated sixties when

capacity use rates were higher, capacity utilization has never

triggered a reading above 91.6. Still, it’s a lot of capacity that is

left unused and the economy is not exactly scooping up the excess at a

rapid rate. Manufacturing capacity use rose from 65.1 in June to 66.1

in July and to 66.6 in August.

Manufacturing: Manufacturing output rose by 0.6% in August

lead by a 0.7% gain in nondurable goods. But durable good output rose

by 0.4% and that was on top of a gain of 1.4% the month before that,

implying a bit more momentum.

By sector: Consumer goods output rose, led by the output

automobiles and products. Business equipment output rose led by the key

transportation sector. Materials output rose led by output in the

energy sector, although nondurables goods ex-energy output also moved

up strongly in the month. Consumer goods business equipment and

materials output all are up for two months running.

Caution about the impact of this strong growth on GDP: In the

quarter to date, with two of three-month’s data in place, industrial

output is up at a 3.4% pace and MFG output is up at a strong 5.7% pace.

While these are strong numbers let me caution you that IP figures do

not easily translate into GDP growth. You have treat the IP report as

if it is an ‘indicator.’ We measure GDP in the United States from the

expenditure side not from the output side and so the IP report per se

does not feed into GDP. One clear issue is that the IP report uses

different seasonal factors and they are real different for the auto

sector. Still, taken and an indicator, the fact that IP is growing at a

3.4% annual rate and MFG at a 5.7% annual rate suggests that there is a

lot of life to GDP. We would expect to find this output either sold to

US consumers, bought by US businesses, sold overseas as exports or

sitting on shelves as inventories (…although inventory data are so weak

that the last option seems less likely and is more there for the sake

of completing the taxonomy of options). So while that accounting is

correct what GDP finds may be different from what IP implies.

What’s still weak? What is still weak in the third quarter is

consumer goods output excluding autos as that metric has output falling

at a 4.2% pace in Q3; the output of consumer energy goods also is

falling at a pace of 12.3% in Q3. In the business sector, the output of

computers and office equipment is falling in Q3 and in the materials

sector, the output of energy products is falling.

But by and large the strength in the industrial sector is

impressive and its momentum into Q3 appears to be quite solid.

| Industrial Production | |||||||

|---|---|---|---|---|---|---|---|

| Monthly Pct. Changes | At Annual Rates of Change | SAAR | |||||

| Month-to-month Pct. Change | 3-Month | 6-Month | Year/Year | 09-Q3 | |||

| Industrial Output | Aug-09 | Jun-09 | Jul-09 | %Change | %Change | %Change | Pct Change |

| All Production & Materials | 0.7% | 0.9% | -0.9% | 2.9% | -3.8% | -10.8% | 3.4% |

| All Products | 0.8% | 0.8% | -0.8% | 3.3% | -3.6% | -8.9% | 3.2% |

| Final Products | 1.1% | 0.9% | -0.9% | 4.4% | -3.3% | -7.3% | 3.7% |

| Manufacturing only | |||||||

| MFG | 0.6% | 1.4% | -1.4% | 2.5% | -2.9% | -12.2% | 5.7% |

| MFG-Durables | 0.4% | 3.2% | -3.1% | 1.7% | -4.7% | -17.7% | 11.0% |

| MFG-Nondurables | 0.7% | -0.1% | 0.1% | 2.9% | -0.2% | -6.2% | 1.4% |

| Consumer Goods | 1.3% | 0.7% | -0.7% | 5.4% | -0.6% | -4.2% | 4.1% |

| Durables | 2.0% | 7.8% | -7.3% | 8.1% | 10.8% | -13.0% | 38.4% |

| Automotive Products | 5.8% | 17.2% | -14.7% | 23.3% | 38.0% | -8.1% | 113.6% |

| Excl Automotive Products | -1.3% | 0.6% | -0.6% | -5.3% | -10.0% | -17.3% | -4.2% |

| Nondurables | 1.2% | -0.8% | 0.8% | 4.7% | -3.0% | -1.9% | -2.4% |

| Nonenergy | 1.2% | -0.4% | 0.4% | 4.7% | -1.0% | -2.8% | 0.8% |

| Consumer Energy | 0.9% | -2.0% | 2.0% | 3.4% | -9.5% | -0.4% | -12.3% |

| Business Equipment | 0.6% | 1.0% | -1.0% | 2.2% | -10.6% | -14.7% | 1.4% |

| Transportation | 2.4% | 4.4% | -4.2% | 9.4% | -5.7% | -15.4% | 20.7% |

| Computer & Office Equipment | -1.2% | -1.2% | 1.2% | -4.7% | -19.6% | -23.8% | -16.3% |

| Excl Technology Transport | 0.4% | 0.5% | -0.5% | 1.6% | -13.0% | -14.2% | -2.2% |

| Materials | 0.5% | 1.3% | -1.3% | 2.1% | -4.3% | -13.1% | 4.0% |

| Durables | 0.0% | 3.5% | -3.3% | 0.0% | -9.1% | -23.8% | 9.3% |

| Nondurables excl Energy | 0.8% | 0.2% | -0.2% | 3.0% | 3.7% | -8.7% | 5.6% |

| Energy | 1.1% | -0.2% | 0.2% | 4.5% | -6.3% | -4.8% | -3.0% |

| Actual Auto Production Levels | |||||||

| Month-to-month Pct. Change | 3-Month | 6-Month | Year/Year | 09-Q3 | |||

| Vehicle Production | Aug-09 | Jun-09 | Jul-09 | %Change | %Change | %Change | Pct Change |

| Autos | 55.9% | -7.0% | 7.5% | 223.6% | 111.1% | -31.4% | 164.0% |

| Trucks | 37.1% | 10.9% | -9.8% | 148.5% | 47.0% | -8.1% | 121.8% |

by Robert Brusca September 16, 2009

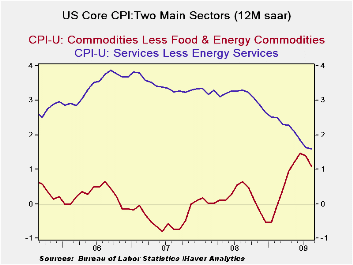

Headline rises 0.4% core rises 0.1% for second month in a row

The summary table shows that inflation remains contained for

the most part. Energy prices rose 8.5% in August slamming the headline

and lien items with energy in them. But core CPI trends remain

controlled. Inflation diffusion rose above 50 to 58.9 in August

implying that inflation rose m/m in more CPI categories than it fell.

But core diffusion was at 48.6 implying that inflation FELL m/m in more

CORE categories in which it rose and that was with the core pace at

+0.1%. That is pretty impressive.

Over three-months: Red figures in the table

above flag four top panel categories as having accelerating inflation

over three-months: Food and beverages where inflation has ‘risen’ to

-0.2% from -1.1% over six months; Housing where at -0.6% over three

months inflation compares to a pace of -0.8% over six months; Apparel

and upkeep where the inflation’s pace shot up to 4.8% over three-months

compared to 1.2% over six months; and, transportation where energy

prices are at work driving the price index up at a 30% pace over

three-months compared to 12.6% over six months. On balance these are

not worrisome developments Transportation is mostly energy prices,

housing costs are tame despite being hit by rising utilities and energy

costs, food and beverage prices are still falling despite

‘accelerating.’ Apparel prices we will see about; but the series is

very volatile and prices tend to run hot and cold without much trend;

indeed despite the high 3-month trend, apparel prices fell in the month

are up by only 0.6% Yr/yr.

These observations underscore several points: that energy

inflation is not always passed along and that it is hard to tell price

volatility from true inflation in the month-to-month reports. So we use

the diffusion results to help guide us and they are very good this

month.

Core Services: Core inflation for services

(excluding energy) appears to be mostly steady at the 1.5% level or so.

Twelve month six-month and three-month inflation trends all converge

around that 1.5% pace which is a very low pace for the service sector

where productivity is lower than for goods making input price pressures

harder to fight-off. Still, all that is going well.

Core Goods: Core goods inflation (excluding

food and energy) had spurted early in the year but it is settling down.

Three-month and Yr/Yr inflation rates are right at the 1% mark but over

six months core goods inflation is still a bit higher at 2.7%, and it

is still coming down from its cyclical peak rate. The trends are good.

| Consumer Prices: 2009 August Report | ||||||||

|---|---|---|---|---|---|---|---|---|

| Overview: Controlled after last month's spurting headline | ||||||||

| Quick Summary | Year-To-Date | One Mo. | Mo/Mo | |||||

| Yr/Yr | 6-Mo a.r. | 3-Mo a.r. | 2009 | 2008 | Diffusion | Aug.2009 | ||

| CPI | -1.4% | 2.3% | 4.9% | -- | 2.7% | 4.9% | 58.9 | NOT |

| Core CPI | 1.5% | 1.9% | 1.4% | -- | 1.9% | 2.4% | 48.6 | Annualized |

| Commodity Category | Mon a.r. | Annualized Inflation Rate For Last: | ||||||

| By Expenditure Category | Aug.2009 | % Weight | 3-Mos | 6-Mos | Year | Month | ||

| All Items | 5.5% | 100.00 | 4.9% | -- | 2.3% | -- | -1.4% | 0.4% |

| Food and Beverages | 1.1% | 16.20 | -0.2% | -- | -1.1% | -- | 0.6% | 0.1% |

| Housing | 0.6% | 39.98 | -0.6% | -- | -0.8% | -- | -0.6% | 0.1% |

| Apparel & Upkeep | -1.1% | 4.45 | 4.8% | -- | 1.2% | -- | 0.6% | -0.1% |

| Transportation | 31.5% | 17.57 | 30.1% | -- | 12.6% | -- | -10.7% | 2.3% |

| Medical care | 3.5% | 5.81 | 2.7% | -- | 3.1% | -- | 3.3% | 0.3% |

| Recreation | 1.3% | 5.91 | 2.4% | -- | 2.9% | -- | 3.7% | 0.5% |

| Educucation & Communication | 2.0% | 5.31 | 2.5% | -- | 3.2% | -- | 3.2% | 0.2% |

| Other Goods & Services | 1.1% | 4.77 | 4.6% | -- | 13.1% | -- | 7.4% | 0.1% |

| By Industry Group | ||||||||

| Nondurables (NSA) | 20.9% | 31.26 | 17.4% | 6.2% | -5.5% | 1.6% | ||

| Durables | -7.3% | 10.57 | -1.2% | 0.5% | -1.5% | -0.6% | ||

| Services | 2.4% | 58.17 | 1.1% | 0.5% | 0.7% | 0.2% | ||

| By Economic Group | ||||||||

| All: Excl Food & Energy | 0.8% | 77.10 | 1.4% | 1.9% | 1.5% | 0.1% | ||

| (Median Increase) | 1.2% | 100.00 | 0.9% | 0.9% | 0.8% | 0.1% | ||

| Excl. Energy | 0.9% | 92.32 | 1.1% | 1.4% | 1.3% | 0.1% | ||

| Commodities: Excl Food & Energy | -3.6% | 22.77 | 1.0% | (29% of core) | 2.7% | 1.1% | -0.3% | |

| Services: Excl Energy | 2.6% | 54.33 | 1.6% | (71% of core) | 1.6% | 1.6% | 0.2% | |

| Core CPI less Tobacco | 0.8% | 1.3% | 1.4% | 1.2% | 0.1% | |||

| Food & Energy | ||||||||

| Energy | 167.6% | 7.68 | 148.5% | 42.2% | -30.8% | 8.5% | ||

| Food | 1.0% | 15.22 | -0.5% | -1.4% | 0.4% | 0.1% | ||

by Robert Brusca September 16, 2009

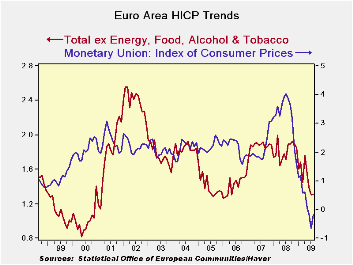

The EMU HICP finalized with August’s headline rate rising by

0.5% in and still dropping by 0.2% Yr/Yr. Core prices rose by 0.2% in

August and rose by 1.2% Yr/Yr – a moderate result and indicating that

inflation pressures are within the ECB’s HICP ceiling constraint. With

headline inflation DOWN Yr/Yr the headline constraint is not going to

be an issue for a while. Keeping inflation below 2% will be easy. But

the core rate will provide better guidance as to what true inflation

trends are doing when the energy sector is not bashing the headline

rate hither and thither each month like a tennis ball caught in a long

rally.

So far the picture is still a good one. Goods sector inflation

is down by 1.5% Yr/Yr while service sector inflation is at 1.8% Yr/Yr.

Goods inflation is off in the recent three-months but service sector

inflation has locked in an increasing trend with six month inflation at

3.1% and three-month services inflation at 4.7%. That trend is a more

than a bit uncomfortable.

At the country level core inflation (excluding food, energy

and alcohol) is well behaved over twelve months with Germany France

Italy and Spain each with 12-month rates below 1.5%. But over the

shorter horizons things get dicey. Only Italy shows a core rate that is

not accelerating. There the core HICP is up by 0.7% over three-months

when annualized. For Germany, France and Spain core inflation has

accelerated to a pace of 1.6%, 1.4% and 1.9% respectively. Those are

uncomfortable results.

Europe remains a troubled economic zone, even as it is engaged

in the recovery process. Recovery is not instantaneous; those who are

displaced have to live through the process until they are re-engaged in

economic activity. And the weaker than expected IFO survey for Germany

has economists thinking that the EMU recovery will be slower rather

than faster. Still at such an early stage of recovery and with the

upswing still nascent, the ECB’s ceiling for headline inflation at 2%

implies a lot of room for discretion but the core rates are doing

things that are troublesome and testing that flexibility. It will be

interesting to see how the ECB handles this delicate proposition. At

least it has a rising exchange rate to help fend of any imported

inflation. With the headline rate under wraps The ECB does have some

time, but when nettlesome inflation trends are present the ECB has not

been known for its patience. Yet the currency is so strong that the ECB

probably does not want to signal that it is closer to the upside of the

cycle for interest rates. The ECB has a dilemma in the making. Core

inflation trends yet could evaporate. But unless they do the ECB is on

a collision course with some hard and unpopular decisions.

| Trends in HICP | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % saar | ||||||

| Aug-09 | Jul-09 | Jun-09 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU | 0.5% | -0.3% | 0.3% | 2.0% | 0.6% | -0.2% | 3.8% |

| Core | 0.2% | 0.0% | 0.1% | 1.5% | 1.4% | 1.2% | 2.6% |

| Goods | 0.4% | -1.7% | 0.2% | -4.1% | 0.1% | -1.5% | 4.6% |

| Services | 0.2% | 0.8% | 0.1% | 4.7% | 3.1% | 1.8% | 2.7% |

| HICP | |||||||

| Germany | 0.7% | -0.5% | 0.5% | 2.6% | 0.6% | -0.1% | 3.3% |

| France | 0.5% | -0.1% | 0.2% | 2.4% | 0.6% | -0.2% | 3.5% |

| Italy | 0.5% | -0.6% | 0.3% | 0.7% | 0.9% | 0.1% | 4.2% |

| Spain | 0.7% | 0.1% | 0.4% | 4.9% | 1.3% | -0.7% | 5.0% |

| Core excl Food Energy & Alcohol | |||||||

| Germany | 0.4% | 0.1% | 0.2% | 2.7% | 1.7% | 1.2% | 1.9% |

| France | 0.3% | 0.1% | 0.1% | 1.6% | 1.4% | 1.4% | 2.3% |

| Italy | 0.5% | -0.4% | 0.1% | 0.7% | 1.3% | 1.2% | 3.2% |

| Spain | 0.1% | 0.2% | 0.2% | 1.9% | 1.1% | 0.5% | 3.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief