Global| Jun 12 2009

Global| Jun 12 2009IP Still Falling in Euro Area: but Evidence of Slowing

Summary

Industrial output fell again in April marking the 12th straight month of decline in Yr/Yr output; industrial output has gone 12-months without a month to month gain as well (m/m output was flat in August of 2008). Declines spread [...]

Industrial output fell again in April marking the 12th

straight month of decline in Yr/Yr output; industrial output has gone

12-months without a month to month gain as well (m/m output was flat in

August of 2008).

Declines spread across all major output categories in the

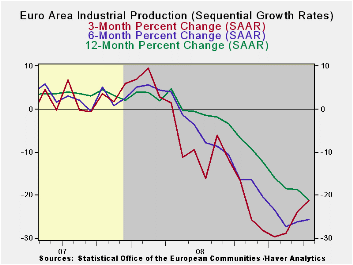

month. In terms of the sequential growth rates (3m compared to 6mo

compared to 12mo) there is improvement in train for intermediate and

capital goods but consumer goods output trends are getting

progressively worse. The overall trends show that after a worsening in

the growth rate at 6-months, the three-month growth rate has limited

its pace of decline to -18.9%.

Obviously the picture for EMU is still poor. Output is

declining on a broad front and still falling sharply on that broad

front. There are some signs that the output declines are abating. The

signs from the EMU index are the weakest. Strongest signs of a

turnaround come from the patterns in the large EMU economies.

| Euro Area MFG IP | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Apr 09 |

Mar 09 |

Apr 09 |

Mar 09 |

Apr 09 |

Mar 09 |

|||

| Euro Area Detail | Apr 09 |

Mar 09 |

Feb 09 |

3mo | 3mo | 6mo | 6mo | 12mo | 12mo | Q-to- Date |

| MFG | -1.5% | -1.2% | -2.5% | -18.9% | -25.4% | -26.5% | -27.6% | -21.5% | -20.2% | -17.3% |

| Consumer | -0.9% | -0.5% | -1.8% | -11.9% | -10.3% | -9.6% | -9.4% | -8.6% | -7.3% | -10.3% |

| Consumer Durables | -0.8% | -1.2% | -3.6% | -20.2% | -24.6% | -25.9% | -26.8% | -22.2% | -20.9% | -- |

| Consumer Nondurables | -0.7% | -0.3% | -1.5% | -9.9% | -7.8% | -6.7% | -6.6% | -6.2% | -5.1% | -- |

| Intermediate | -1.7% | -1.8% | -2.5% | -21.6% | -22.8% | -32.5% | -34.1% | -26.6% | -25.3% | -20.4% |

| Capital | -2.7% | 0.0% | -3.1% | -21.0% | -34.6% | -32.6% | -32.8% | -26.3% | -22.3% | -20.5% |

| Main Euro Area Countries and UK IP in MFG | ||||||||||

| Mo/Mo | Apr-09 | Mar 09 |

Apr 09 |

Mar 09 |

Apr 09 |

Mar 09 |

||||

| MFG Only | Apr 09 |

Mar 09 |

Feb 09 |

3mo | 3mo | 6mo | 6mo | 12mo | 12mo | Q-to- Date |

| Germany: | -2.9% | 0.8% | -3.5% | -20.5% | -35.2% | -36.8% | -35.8% | -24.2% | -22.1% | -19.4% |

| France: IP excl Construction | -1.4% | -1.7% | -0.9% | -15.0% | -24.4% | -22.5% | -26.1% | -18.8% | -16.4% | -15.8% |

| Italy | 0.7% | -4.7% | -5.0% | -30.9% | -36.7% | -30.6% | -34.8% | -25.2% | -25.6% | -22.7% |

| Spain | 5.8% | -5.0% | 1.2% | 7.1% | -39.1% | -24.7% | -36.1% | -28.6% | -13.7% | 16.7% |

| UK: EU member | 0.2% | 0.2% | -0.2% | 0.9% | -12.2% | -15.2% | -18.2% | -12.7% | -13.1% | 1.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief