Global| Jan 14 2014

Global| Jan 14 2014IP Is Recovering

Summary

Manufacturing industrial production in the euro area spurted by 1.9% in November, offsetting two straight months of declines in October and September. Growth rates show acceleration from a 3.2% year-over-year rate to rates of 4.3% [...]

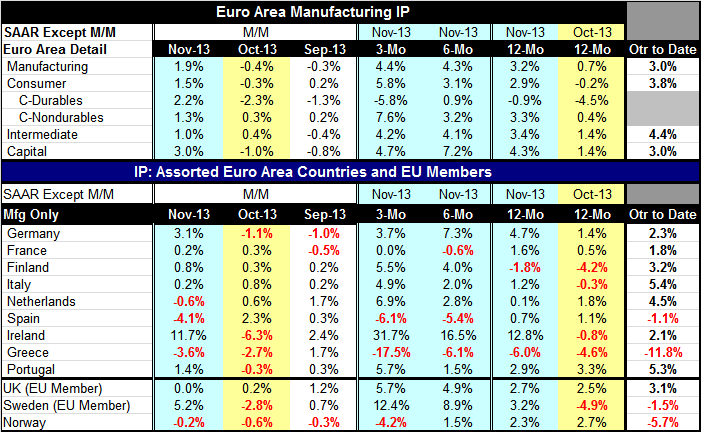

Manufacturing industrial production in the euro area spurted by 1.9% in November, offsetting two straight months of declines in October and September. Growth rates show acceleration from a 3.2% year-over-year rate to rates of 4.3% over six months and 4.4% over three months. All three main sectors consumer goods, intermediate goods and capital goods showed gains in November. Capital goods lead the pack with a 3% gain in November, followed by consumer goods output, up by 1.5% and intermediate goods output, up by 1.0%. The sequential growth rates show that growth right now is being boosted by the consumer sector where, over three months, output is increasing at a 5.8% annual rate, up from 3.1% over six months and 2.9% over three months. By comparison, capital goods output is up at a 4.7% annual rate over three months, down from a 7.2% pace over six months but ahead of its 4.3% gain over 12 months. Intermediate goods follow closely the pattern for headline output with a year-over-year growth rate of 3.4%, stepping up to 4.1% over six months and 4.2% over three months.

Manufacturing industrial production in the euro area spurted by 1.9% in November, offsetting two straight months of declines in October and September. Growth rates show acceleration from a 3.2% year-over-year rate to rates of 4.3% over six months and 4.4% over three months. All three main sectors consumer goods, intermediate goods and capital goods showed gains in November. Capital goods lead the pack with a 3% gain in November, followed by consumer goods output, up by 1.5% and intermediate goods output, up by 1.0%. The sequential growth rates show that growth right now is being boosted by the consumer sector where, over three months, output is increasing at a 5.8% annual rate, up from 3.1% over six months and 2.9% over three months. By comparison, capital goods output is up at a 4.7% annual rate over three months, down from a 7.2% pace over six months but ahead of its 4.3% gain over 12 months. Intermediate goods follow closely the pattern for headline output with a year-over-year growth rate of 3.4%, stepping up to 4.1% over six months and 4.2% over three months.

In the quarter to date, manufacturing output is rising at a 3% annual rate. Intermediate goods output is up at a 4.4% annual rate the quarter, followed by 3.8% pace for consumer goods and a 3% pace for capital goods.

Turning to a list of European Monetary Union members and others, we see that of the respondents in the table of which nine are monetary union members and three are not, output fell in November in only four countries. There was a relatively sharp drop of 4.1% in Spain and a 3.6% drop in Greece. As a lesser drop of 0.6% was posted in the Netherlands and a small decline of 0.2% in Norway- although for Norway this marks a string of three straight declines. Ireland's gain leads the pack at an 11.3% increase in November followed by Germany and Portugal. Portugal is getting ready to exit its bailout program.

There are four countries in the table that post declines in output in the quarter to date. Only two of them are monetary union countries. Among them Greece's 11.8% annual rate decline in the quarter to date leads the pack. Spain shows a 1.1% decline. Italy, Portugal and the Netherlands show the largest quarter to date increases in industrial production, at 5.5%, 5.3% and 4.5%, respectively. Germany, that has been a stalwart of the monetary union, has its output increasing at a 2.3% annual rate in the quarter to date.

As we have noted before, output is making a good showing for itself around the world in the industrial sector. The fly in the ointment has been the services sector which is the jobs sector in most countries. It is our hope that this improvement industrial production is going to carryover to help spur the rest of the economy. But we should make no mistake about it. The manufacturing sector is important, but it is not the only part of the economy that matters.

Banking sectors are still struggling with post financial crisis issues. In Denmark the authorities are thinking about taking more draconian steps to monitor bank lending that could wind up holding back growth. As the European Central Bank gets ready to implement stress test for banks around the union, it is a little bit worried about various national treatments across asset classes. While some look forward to the potential for ECB stress tests to give euro-banks a clean bill of health, and to provide an opportunity for them to raise capital, we don't share in this optimism. After each of the last two rounds of stress tests in the monetary union, banks that had passed the stress tests subsequently failed. The most recent example of this was Dexia.

The monetary union still has only one monetary policy to run for the whole of the union. And there is a program to help beleaguered banks as a unified effort. Fiscal policy continues to be patchwork and hodgepodge. Despite the fact that Mr. Draghi won the governor of the year award, the available tools to actually do things are limited. While he may have a firm conviction about what to do, the rest of the euro area is pretty much in disarray. If the recovery that is starting continues, the the euro zone will be fine. But if there is backsliding or a need for action, Europe still does not have targeted methods or programs to help out - or even a consensus on what to do. Make no mistake about it, the progress in manufacturing is very good news. But make no mistake about it... much more is needed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.