Global| Jul 10 2019

Global| Jul 10 2019IP Is Mixed Across EMU

Summary

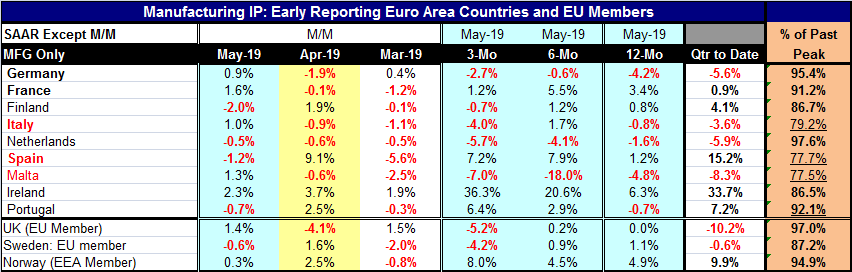

In May among reporting EMU members listed in the table, four show IP declines while five show increases month-to-month. In April there were five declines and in March the bottom fell out and seven declined. Output trends have [...]

In May among reporting EMU members listed in the table, four show IP declines while five show increases month-to-month. In April there were five declines and in March the bottom fell out and seven declined. Output trends have progressed better since March.

In May among reporting EMU members listed in the table, four show IP declines while five show increases month-to-month. In April there were five declines and in March the bottom fell out and seven declined. Output trends have progressed better since March.

Over sequential periods of three months, six months and 12 months, the number of countries with declining IP has been above half of the total number of countries over three months and 12 months, in each case with a count of five, barely more than half. Among the four largest EMU economies, there are declines in IP in two of them over three months, in one of them over six months and in two of them over 12 months. It seems no matter how you look at IP or divided it up, there are mixed conditions in the EMU. Growth in manufacturing has slowed and it is sipping in some places, but growth is fighting a stiff rear-guard action and not giving into decline across the board.

In addition, there are few countries with clear trends in play. The Netherlands shows clear deceleration and has declines on all three horizons. Sweden also shows clear ongoing deceleration. Spain is close to showing sequential acceleration. Ireland shows a very strong acceleration. Portugal shows acceleration and Norway (not an EMU member) is also close showing acceleration.

Two months into Q2, the quarter shows decline in output in four member states, one of them being the largest economy in the EMU and another the third largest economy. Spain, the fourth largest economy shows very strong output QTD.

We can also assess the state of manufacturing output across the regions. Among the nine reporting EMU countries in the table, six of them have manufacturing IP at 80% of more of their past peak. Four are in their 90th percentile range. Only Italy, Spain and Malta have IP in its 70th percentile range of its past peak. Clearly, there is industrial slack since industrial capacity will growth from its past peak. But a past peak comparison is an easy way to make the point and to demonstrate various national differences in slack. Italy and Spain show a lot of slack and Germany shows very little. Among the four largest EMU economies, Germany’s inflation has been relatively high in the last four years while in Italy and Spain inflation has been lower than in Germany.

The manufacturing sector has been under the most intense pressure. The Markit PMI reading is at 47.7, below 50 for four months in a row and points to declines in manufacturing output over those months. The Markit data are up to date though May and continue to show deceleration. The actual output data still seem to show a year-on-year decline for EMU manufacturing overall although the precise figure is not yet released. Looking at the details across EMU member nations, it is clear that whatever is happing on a pooled basis in the EMU, national conditions are varied. At this point, the European data do seem to be pointing to an overall loss in momentum. However, output declines come and go without leading to recessions. So far, Europe seems more like it has lost momentum. It does not look as yet as though there is a cumulative decline in the making. But manufacturing has weakened, has lost momentum and should continue to be monitored closely.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief