Global| Oct 10 2007

Global| Oct 10 2007IP in Euro Area Still Growing Despite Slowing Signs

Summary

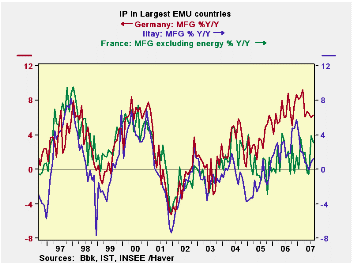

EMU growth is cropping to be strong in Q3, at least for industrial output. In France manufacturing output excluding energy is up at a 9% annualized Q/Q rate. In Germany output is up at a 7.9% rate. In Spain its up at an 8% rate. Even [...]

EMU growth is cropping to be strong in Q3, at least for industrial output. In France manufacturing output excluding energy is up at a 9% annualized Q/Q rate. In Germany output is up at a 7.9% rate. In Spain it’s up at an 8% rate. Even Italy shows a 4.4% rate of increase. The UK, an EU member, is showing slower IP growth in Q3 as output is up at just a 0.8% rate of increase. Sequential IP growth figures show us that growth has been accelerating in Germany, France and Italy. Spain shows sudden weakness in the most recent three months The UK shows some sporadic slowing as the recent rates of growth reveal a slow down over three months but over six months, a speed up.

On balance, despite weakening orders and slowdown assessment from Germany’s Chamber of Commerce (DIHK) and weaker surveys from the Reuters NTC survey as well as from various national surveys, actual production has been on an accelerating run. What we see is that this acceleration is counter to what surveys say they now expect. Some of the divergence reflects inter-temporal discord and mismatch. Since the financial market situation only began to turn abruptly in August before mid month, it is the reports of the next several months that should be most revealing as far as output is concerned. Up to now what we see is that, despite some weaker (and more topical) survey findings, actual output has remained firm through August for the main economies of EMU. Separately what survey data tell us is this: don’t get used to it.

| Main Euro Area Countries and UK IP in MFG | |||||||

|---|---|---|---|---|---|---|---|

| M/M | |||||||

| Aug-07 | Jul-07 | Jun-07 | 3-Month | 6-month | 12-month | Q2-Date | |

| Germany: Mfg IP | 1.8% | 0.2% | -0.3% | 7.2% | 5.6% | 6.2% | 7.9% |

| France: IP ex Construction | 0.3% | 1.7% | -0.5% | 6.3% | 3.3% | 2.6% | 9.0% |

| Italy: Mfg IP | 1.5% | 0.1% | -0.2% | 5.9% | 2.1% | 1.2% | 4.4% |

| Spain: Mfg IP | 1.3% | 1.7% | -4.2% | -5.3% | 3.9% | 0.5% | 8.0% |

| UK: Mfg IP | 0.4% | -0.2% | 0.1% | 1.2% | 3.4% | 0.6% | 0.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief